Advertisement

Subaru (TSE:7270): Assessing Valuation Following Dividend Hike and Updated Production Numbers

Simply Wall St

Reviewed by Simply Wall St

Subaru (TSE:7270) is on investors' radar after announcing its second-quarter dividend will climb to JPY 57.00 per share, up from JPY 48.00 a year ago. The company also updated its first-half production numbers, reporting 453,000 units built compared to 475,000 last year.

See our latest analysis for Subaru.

Subaru's latest dividend bump and production update come after a year marked by steady upward momentum. The stock’s share price has climbed 24.2% year-to-date, but what truly stands out for long-term investors is its total shareholder return of 45.5% over the past 12 months. This signals that market optimism around the brand is growing even as production eases off recent highs.

If Subaru’s recent performance has sparked your curiosity, now’s a perfect time to see what’s happening across the sector and discover See the full list for free.

But with the stock riding high and fundamentals improving at a modest pace, investors have to ask: Is Subaru undervalued at current levels, or are markets already pricing in the next wave of growth?

Price-to-Earnings of 9.3x: Is it justified?

Subaru’s shares are trading at a price-to-earnings (P/E) ratio of 9.3x, below both the Japanese market average and its industry peers, signaling the market may be undervaluing its current earnings profile.

The P/E ratio reflects how much investors are willing to pay per yen of earnings, offering a snapshot of market confidence in future profitability. For automakers like Subaru, investors often look to the P/E to judge whether the stock is pricing in enough growth or caution.

With Subaru’s P/E standing well under the Japanese auto sector average of 18.1x and even below the broader market’s 13.9x, it looks attractively priced on this metric. Notably, the fair P/E ratio is estimated at 14.1x, which suggests there could be potential for the share price to re-rate upwards if fundamentals support it.

Explore the SWS fair ratio for Subaru

Result: Price-to-Earnings of 9.3x (UNDERVALUED)

However, slowing production numbers and a share price now above analyst targets could limit further upside if Subaru's earnings momentum slows.

Find out about the key risks to this Subaru narrative.

Another View: What Does the SWS DCF Model Say?

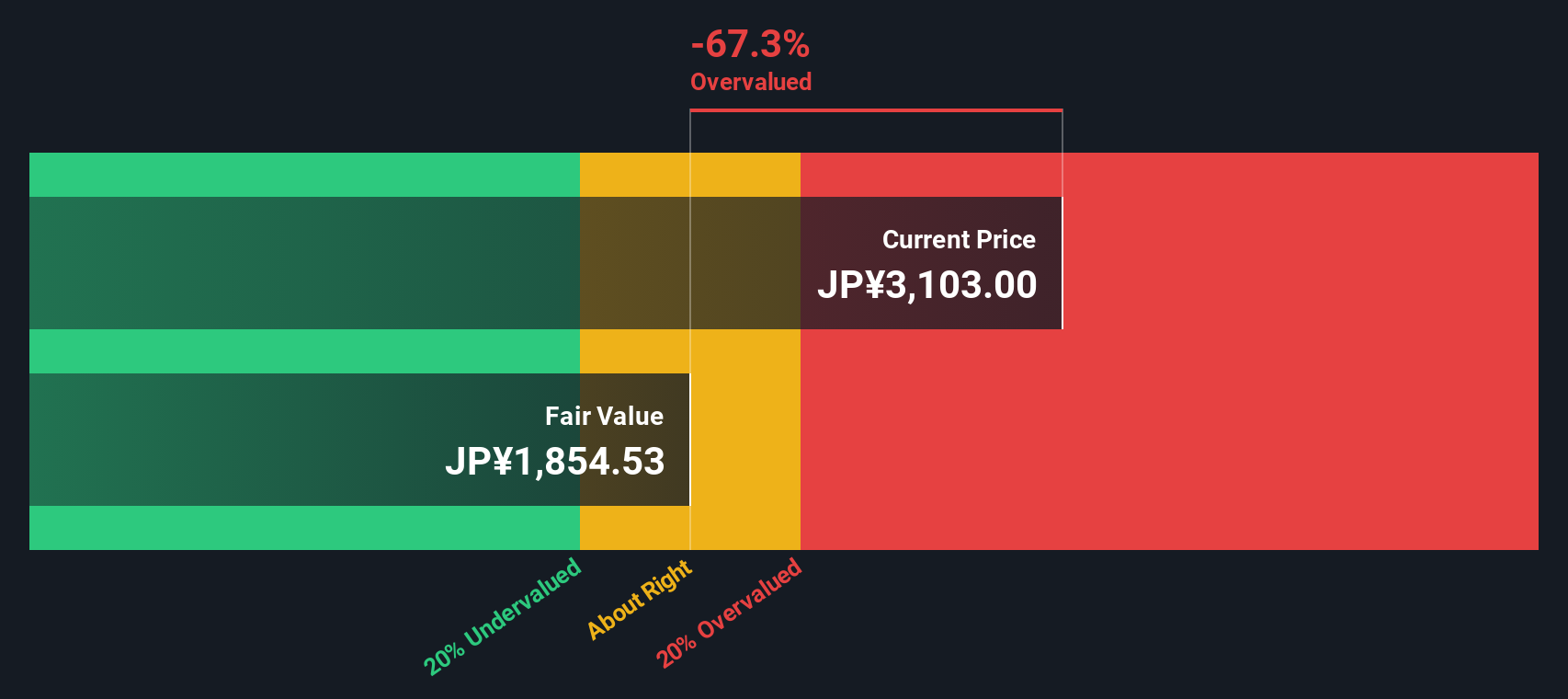

While Subaru’s low P/E ratio suggests a possible bargain, our DCF model takes a longer, cash flow-based approach and presents a different picture. It estimates Subaru’s fair value at ¥2,341.56 per share, meaning the current price may actually be overvalued by a significant margin. Could this caution investors against getting too swept up in recent momentum?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Subaru for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 923 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Subaru Narrative

If you see the numbers differently or want to dig deeper into Subaru’s outlook, you can craft your own take in just a few minutes with Do it your way.

A great starting point for your Subaru research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors know that broadening their watchlist can uncover hidden gems. Don’t miss your chance to target unique opportunities across a range of cutting-edge themes today.

- Tap into emerging trends by following these 26 AI penny stocks transforming industries with artificial intelligence-powered growth and innovation.

- Strengthen your portfolio with stability and yield. Review these 15 dividend stocks with yields > 3% offering consistently attractive payouts above 3%.

- Capture early-stage upside as you check out these 3594 penny stocks with strong financials breaking through with promising fundamentals and growth potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7270

Subaru

Manufactures and sells automobiles and aerospace products in Japan, Rest of Asia, North America, Europe, and Internationally.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor