Advertisement

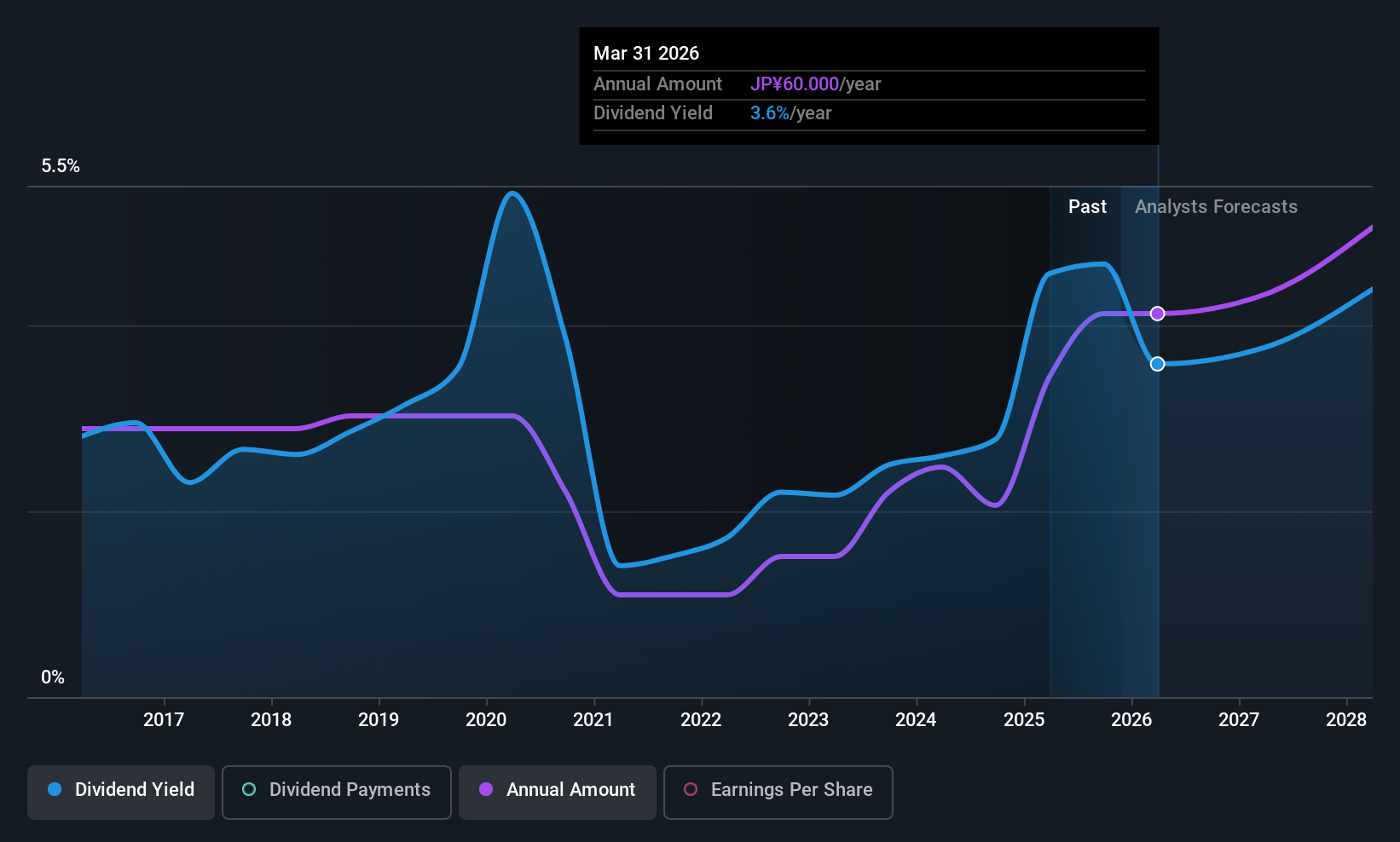

The board of JTEKT Corporation (TSE:6473) has announced that it will pay a dividend on the 25th of May, with investors receiving ¥30.00 per share. This will take the annual payment to 3.6% of the stock price, which is above what most companies in the industry pay.

JTEKT's Projected Earnings Seem Likely To Cover Future Distributions

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Prior to this announcement, JTEKT's dividend was making up a very large proportion of earnings and perhaps more concerning was that it was 100% of cash flows. This is certainly a risk factor, as reduced cash flows could force the company to pay a lower dividend.

Over the next year, EPS is forecast to expand by 39.9%. Assuming the dividend continues along the course it has been charting recently, our estimates show the payout ratio being 69% which brings it into quite a comfortable range.

View our latest analysis for JTEKT

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. The annual payment during the last 10 years was ¥28.00 in 2015, and the most recent fiscal year payment was ¥60.00. This means that it has been growing its distributions at 7.9% per annum over that time. We have seen cuts in the past, so while the growth looks promising we would be a little bit cautious about its track record.

JTEKT's Dividend Might Lack Growth

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. JTEKT has impressed us by growing EPS at 20% per year over the past five years. Fast growing earnings are great, but this can rarely be sustained without some reinvestment into the business, which JTEKT hasn't been doing.

The Dividend Could Prove To Be Unreliable

In summary, while it's always good to see the dividend being raised, we don't think JTEKT's payments are rock solid. In general, the distributions are a little bit higher than we would like, but we can't ignore the fact the quickly growing earnings gives this stock great potential in the future. This company is not in the top tier of income providing stocks.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Just as an example, we've come across 2 warning signs for JTEKT you should be aware of, and 1 of them is a bit unpleasant. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6473

JTEKT

Manufactures and sells steering systems, driveline components, bearings, machine tools, electronic control devices, and home accessory equipment.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

80 followersusers have followed this narrative

3 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

91 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative