Advertisement

- Italy

- /

- Other Utilities

- /

- BIT:IRE

Growth Investors: Industry Analysts Just Upgraded Their Iren SpA (BIT:IRE) Revenue Forecasts By 13%

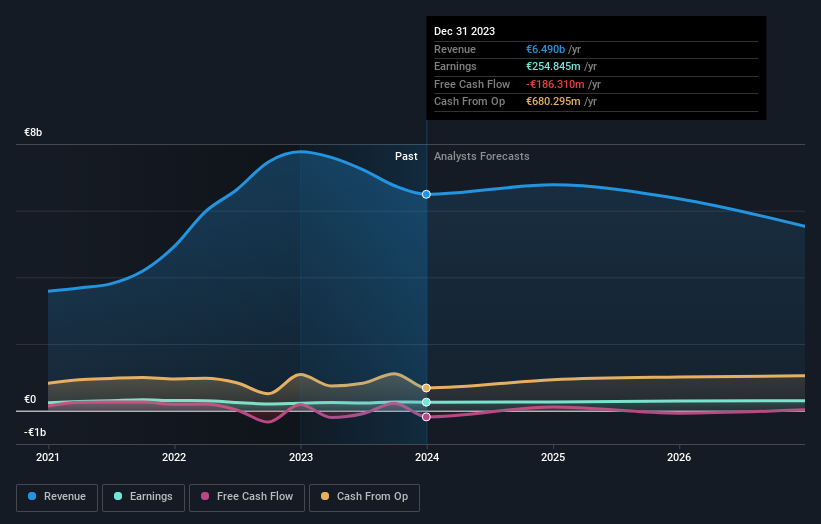

Celebrations may be in order for Iren SpA (BIT:IRE) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The revenue forecast for this year has experienced a facelift, with the analysts now much more optimistic on its sales pipeline.

Following the upgrade, the current consensus from Iren's three analysts is for revenues of €6.8b in 2024 which - if met - would reflect a satisfactory 4.4% increase on its sales over the past 12 months. Statutory earnings per share are expected to be €0.20, roughly flat on the last 12 months. Before this latest update, the analysts had been forecasting revenues of €6.0b and earnings per share (EPS) of €0.20 in 2024. The forecasts seem more optimistic now, with a substantial gain in revenue and a modest lift to earnings per share estimates.

Check out our latest analysis for Iren

Although the analysts have upgraded their earnings estimates, there was no change to the consensus price target of €2.28, suggesting that the forecast performance does not have a long term impact on the company's valuation.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Iren's past performance and to peers in the same industry. We would highlight that Iren's revenue growth is expected to slow, with the forecast 4.4% annualised growth rate until the end of 2024 being well below the historical 16% p.a. growth over the last five years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 1.7% per year. Even after the forecast slowdown in growth, it seems obvious that Iren is also expected to grow faster than the wider industry.

The Bottom Line

The biggest takeaway for us from these new estimates is that analysts upgraded their earnings per share estimates, with improved earnings power expected for this year. They also upgraded their revenue estimates for this year, and sales are expected to grow faster than the wider market. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at Iren.

Better yet, our automated discounted cash flow calculation (DCF) suggests Iren could be moderately undervalued. For more information, you can click through to our platform to learn more about our valuation approach.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:IRE

6 star dividend payer with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor