Stock Analysis

- Italy

- /

- Specialty Stores

- /

- BIT:BELL

Has Bellini Nautica S.p.A.'s (BIT:BELL) Impressive Stock Performance Got Anything to Do With Its Fundamentals?

Bellini Nautica's (BIT:BELL) stock is up by a considerable 28% over the past three months. As most would know, fundamentals are what usually guide market price movements over the long-term, so we decided to look at the company's key financial indicators today to determine if they have any role to play in the recent price movement. Specifically, we decided to study Bellini Nautica's ROE in this article.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

View our latest analysis for Bellini Nautica

How Is ROE Calculated?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Bellini Nautica is:

3.2% = €241k ÷ €7.5m (Based on the trailing twelve months to December 2023).

The 'return' refers to a company's earnings over the last year. One way to conceptualize this is that for each €1 of shareholders' capital it has, the company made €0.03 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Bellini Nautica's Earnings Growth And 3.2% ROE

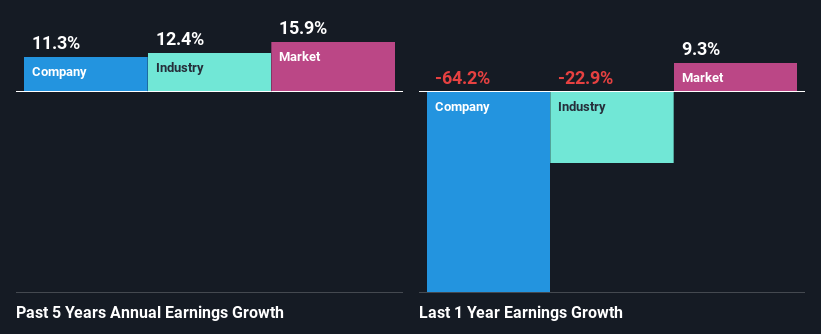

As you can see, Bellini Nautica's ROE looks pretty weak. Even compared to the average industry ROE of 14%, the company's ROE is quite dismal. Bellini Nautica was still able to see a decent net income growth of 11% over the past five years. We believe that there might be other aspects that are positively influencing the company's earnings growth. For instance, the company has a low payout ratio or is being managed efficiently.

As a next step, we compared Bellini Nautica's net income growth with the industry and found that the company has a similar growth figure when compared with the industry average growth rate of 12% in the same period.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. Doing so will help them establish if the stock's future looks promising or ominous. If you're wondering about Bellini Nautica's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Bellini Nautica Efficiently Re-investing Its Profits?

Bellini Nautica doesn't pay any regular dividends, meaning that all of its profits are being reinvested in the business, which explains the fair bit of earnings growth the company has seen.

Conclusion

Overall, we feel that Bellini Nautica certainly does have some positive factors to consider. Even in spite of the low rate of return, the company has posted impressive earnings growth as a result of reinvesting heavily into its business. That being so, the latest analyst forecasts show that the company will continue to see an expansion in its earnings. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

Valuation is complex, but we're helping make it simple.

Find out whether Bellini Nautica is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:BELL

Bellini Nautica

Engages in the sale of new Cranchi yachts and used Riva motorboats, dinghies, and motorboats.

Mediocre balance sheet with concerning outlook.