Advertisement

- Italy

- /

- Consumer Finance

- /

- BIT:MOL

Gruppo MutuiOnline S.p.A Just Recorded A 16% Revenue Beat: Here's What Analysts Think

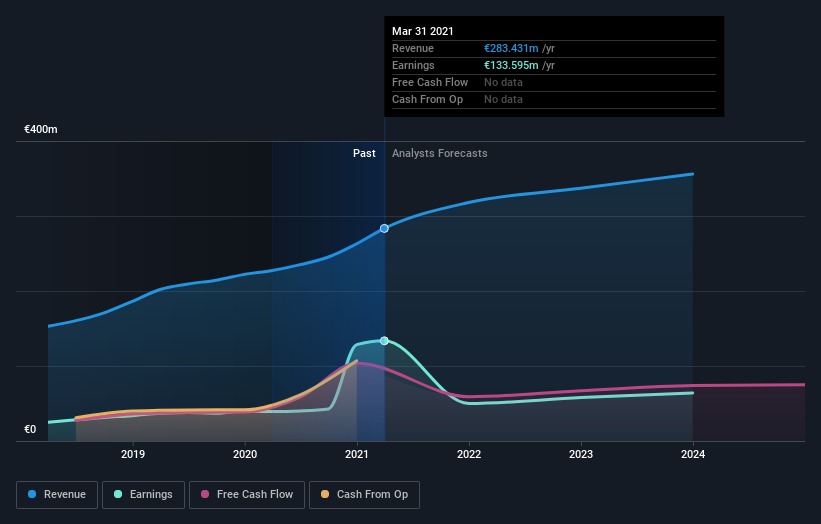

Gruppo MutuiOnline S.p.A (BIT:MOL) shareholders are probably feeling a little disappointed, since its shares fell 7.8% to €40.40 in the week after its latest first-quarter results. Gruppo MutuiOnline beat revenue forecasts by a solid 16% to hit €78m. Statutory earnings per share came in at €3.28, in line with expectations. Following the result, the analyst has updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. With this in mind, we've gathered the latest statutory forecasts to see what the analyst is expecting for next year.

See our latest analysis for Gruppo MutuiOnline

After the latest results, the sole analyst covering Gruppo MutuiOnline are now predicting revenues of €318.0m in 2021. If met, this would reflect a notable 12% improvement in sales compared to the last 12 months. Statutory earnings per share are expected to dive 62% to €1.34 in the same period. Yet prior to the latest earnings, the analyst had been anticipated revenues of €308.0m and earnings per share (EPS) of €1.33 in 2021. There doesn't appear to have been a major change in sentiment following the results, other than the modest lift to revenue estimates.

The analyst increased their price target 15% to €50.00, perhaps signalling that higher revenues are a strong leading indicator for Gruppo MutuiOnline's valuation.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. The period to the end of 2021 brings more of the same, according to the analyst, with revenue forecast to display 17% growth on an annualised basis. That is in line with its 16% annual growth over the past five years. Compare this with the broader industry, which analyst estimates (in aggregate) suggest will see revenues grow 18% annually. It's clear that while Gruppo MutuiOnline's revenue growth is expected to continue on its current trajectory, it's only expected to grow in line with the industry itself.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analyst reconfirming that the business is performing in line with their previous earnings per share estimates. They also upgraded their revenue forecasts, although the latest estimates suggest that Gruppo MutuiOnline will grow in line with the overall industry. We note an upgrade to the price target, suggesting that the analyst believes the intrinsic value of the business is likely to improve over time.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At least one analyst has provided forecasts out to 2023, which can be seen for free on our platform here.

And what about risks? Every company has them, and we've spotted 2 warning signs for Gruppo MutuiOnline (of which 1 shouldn't be ignored!) you should know about.

If you decide to trade Gruppo MutuiOnline, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About BIT:MOL

Moltiply Group

A holding company that operates in the financial services industry.

High growth potential with proven track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

932 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative