- Italy

- /

- Consumer Durables

- /

- BIT:EM

The Emak S.p.A. (BIT:EM) Analyst Just Boosted Their Forecasts By A Substantial Amount

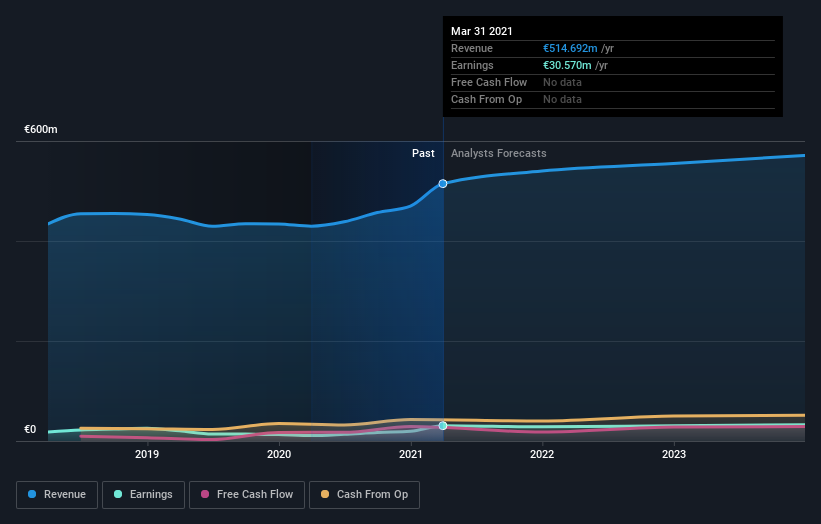

Emak S.p.A. (BIT:EM) shareholders will have a reason to smile today, with the covering analyst making substantial upgrades to this year's forecasts. The consensus statutory numbers for both revenue and earnings per share (EPS) increased, with their view clearly much more bullish on the company's business prospects. The stock price has risen 9.4% to €1.84 over the past week, suggesting investors are becoming more optimistic. It will be interesting to see if this latest upgrade is enough to kickstart further buying interest in the stock.

After this upgrade, Emak's sole analyst is now forecasting revenues of €540m in 2021. This would be an okay 4.9% improvement in sales compared to the last 12 months. Statutory earnings per share are anticipated to reduce 7.5% to €0.17 in the same period. Before this latest update, the analyst had been forecasting revenues of €489m and earnings per share (EPS) of €0.13 in 2021. There has definitely been an improvement in perception recently, with the analyst substantially increasing both their earnings and revenue estimates.

See our latest analysis for Emak

With these upgrades, we're not surprised to see that the analyst has lifted their price target 30% to €2.40 per share.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We can infer from the latest estimates that forecasts expect a continuation of Emak'shistorical trends, as the 4.9% annualised revenue growth to the end of 2021 is roughly in line with the 4.2% annual revenue growth over the past five years. Compare this with the broader industry, which analyst estimates (in aggregate) suggest will see revenues grow 4.8% annually. It's clear that while Emak's revenue growth is expected to continue on its current trajectory, it's only expected to grow in line with the industry itself.

The Bottom Line

The most important thing to take away from this upgrade is that the analyst upgraded their earnings per share estimates for this year, expecting improving business conditions. There was also an upgrade to revenue estimates, although as we saw earlier, forecast growth is only expected to be about the same as the wider market. With a serious upgrade to expectations and a rising price target, it might be time to take another look at Emak.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. We have analyst estimates for Emak going out as far as 2023, and you can see them free on our platform here.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

If you’re looking to trade Emak, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Emak might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About BIT:EM

Emak

Manufactures and distributes machines, components, and accessories for gardening, agriculture, forestry, and industries worldwide.

Good value with proven track record.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Clarivate Stock: When Data Becomes the Backbone of Innovation and Law

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion