Advertisement

- Italy

- /

- Industrials

- /

- BIT:ITM

Earnings Tell The Story For Italmobiliare S.p.A. (BIT:ITM) As Its Stock Soars 26%

Italmobiliare S.p.A. (BIT:ITM) shareholders have had their patience rewarded with a 26% share price jump in the last month. Looking back a bit further, it's encouraging to see the stock is up 37% in the last year.

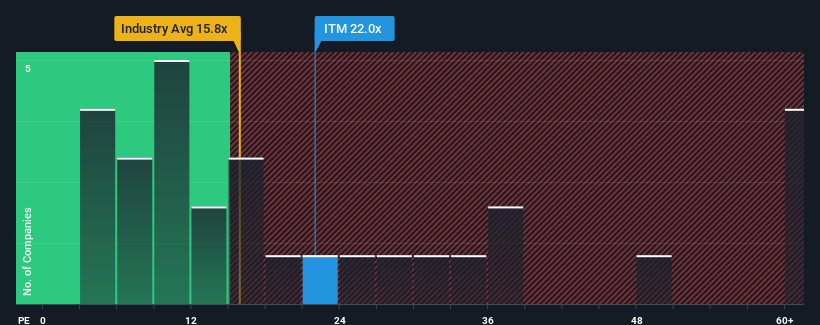

After such a large jump in price, Italmobiliare's price-to-earnings (or "P/E") ratio of 22x might make it look like a strong sell right now compared to the market in Italy, where around half of the companies have P/E ratios below 13x and even P/E's below 8x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Recent times have been advantageous for Italmobiliare as its earnings have been rising faster than most other companies. The P/E is probably high because investors think this strong earnings performance will continue. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Italmobiliare

Does Growth Match The High P/E?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Italmobiliare's to be considered reasonable.

If we review the last year of earnings growth, the company posted a terrific increase of 216%. The latest three year period has also seen a 5.2% overall rise in EPS, aided extensively by its short-term performance. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

Turning to the outlook, the next three years should generate growth of 22% per annum as estimated by the two analysts watching the company. That's shaping up to be materially higher than the 12% each year growth forecast for the broader market.

In light of this, it's understandable that Italmobiliare's P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From Italmobiliare's P/E?

The strong share price surge has got Italmobiliare's P/E rushing to great heights as well. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Italmobiliare maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. It's hard to see the share price falling strongly in the near future under these circumstances.

And what about other risks? Every company has them, and we've spotted 1 warning sign for Italmobiliare you should know about.

Of course, you might also be able to find a better stock than Italmobiliare. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:ITM

Italmobiliare

An investment holding company, owns and manages a portfolio of equity and other investments in the financial and industrial sectors in Italy and internationally.

Reasonable growth potential with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor