Advertisement

- India

- /

- Renewable Energy

- /

- NSEI:ACMESOLAR

ACME Solar Holdings Limited (NSE:ACMESOLAR) Stocks Shoot Up 26% But Its P/E Still Looks Reasonable

ACME Solar Holdings Limited (NSE:ACMESOLAR) shares have continued their recent momentum with a 26% gain in the last month alone. While recent buyers may be laughing, long-term holders might not be as pleased since the recent gain only brings the stock back to where it started a year ago.

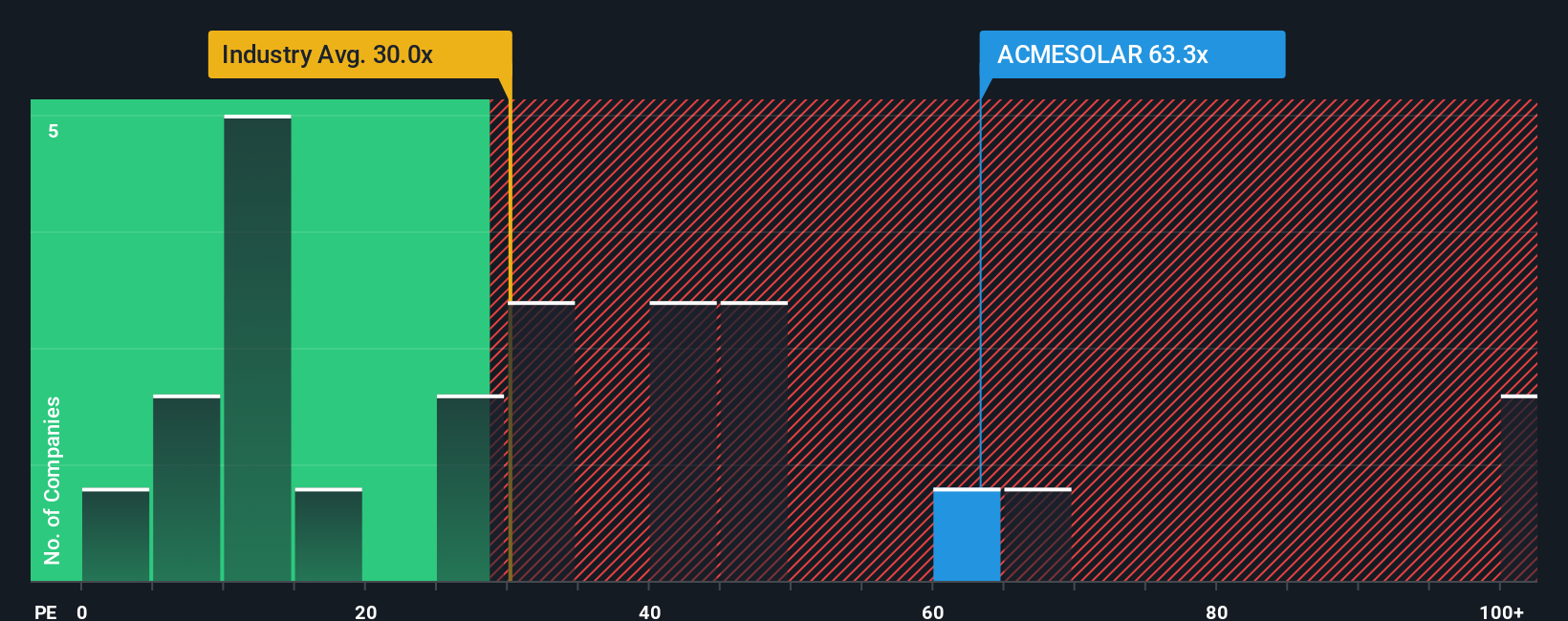

Since its price has surged higher, ACME Solar Holdings' price-to-earnings (or "P/E") ratio of 63.3x might make it look like a strong sell right now compared to the market in India, where around half of the companies have P/E ratios below 28x and even P/E's below 16x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

ACME Solar Holdings could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. It might be that many expect the dour earnings performance to recover substantially, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for ACME Solar Holdings

Is There Enough Growth For ACME Solar Holdings?

ACME Solar Holdings' P/E ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 64%. However, a few very strong years before that means that it was still able to grow EPS by an impressive 274% in total over the last three years. So we can start by confirming that the company has generally done a very good job of growing earnings over that time, even though it had some hiccups along the way.

Looking ahead now, EPS is anticipated to climb by 75% per year during the coming three years according to the six analysts following the company. Meanwhile, the rest of the market is forecast to only expand by 21% per year, which is noticeably less attractive.

In light of this, it's understandable that ACME Solar Holdings' P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

Shares in ACME Solar Holdings have built up some good momentum lately, which has really inflated its P/E. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of ACME Solar Holdings' analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

And what about other risks? Every company has them, and we've spotted 2 warning signs for ACME Solar Holdings (of which 1 doesn't sit too well with us!) you should know about.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ACMESOLAR

ACME Solar Holdings

A solar independent power producing company, engages in developing, building, owning, operating, and maintaining utility scale renewable energy projects in India.

Exceptional growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|49.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|7.0% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|20.3% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|54.2% overvalued

RO

Community Contributor