Advertisement

- India

- /

- Tech Hardware

- /

- NSEI:TVSELECT

TVS Electronics (NSE:TVSELECT) Has Announced That Its Dividend Will Be Reduced To ₹1.00

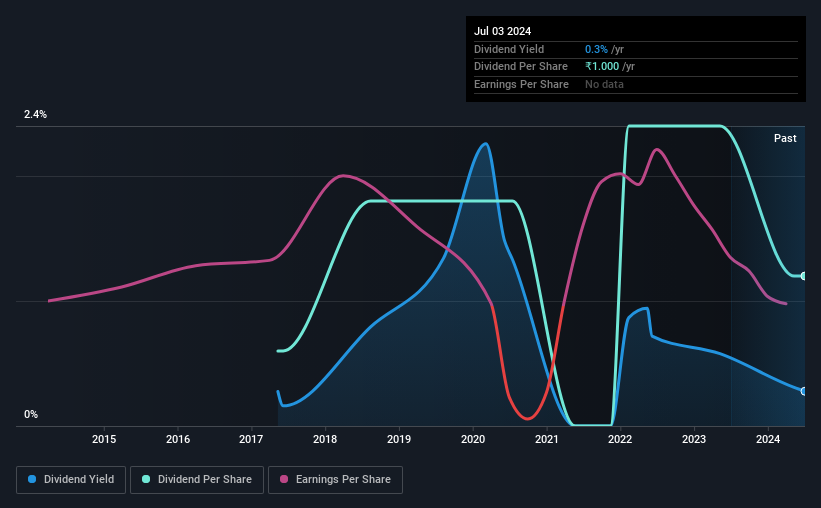

TVS Electronics Limited's (NSE:TVSELECT) dividend is being reduced from last year's payment covering the same period to ₹1.00 on the 9th of September. This means that the dividend yield is 0.3%, which is a bit low when comparing to other companies in the industry.

View our latest analysis for TVS Electronics

TVS Electronics Doesn't Earn Enough To Cover Its Payments

If it is predictable over a long period, even low dividend yields can be attractive. Prior to this announcement, the dividend made up 667% of earnings, and the company was generating negative free cash flows. This high of a dividend payment could start to put pressure on the balance sheet in the future.

Looking forward, EPS could fall by 51.3% if the company can't turn things around from the last few years. If the dividend continues along recent trends, we estimate the payout ratio could reach 1,439%, which could put the dividend in jeopardy if the company's earnings don't improve.

TVS Electronics' Dividend Has Lacked Consistency

Looking back, TVS Electronics' dividend hasn't been particularly consistent. This makes us cautious about the consistency of the dividend over a full economic cycle. The annual payment during the last 7 years was ₹0.50 in 2017, and the most recent fiscal year payment was ₹1.00. This means that it has been growing its distributions at 10% per annum over that time. Dividends have grown rapidly over this time, but with cuts in the past we are not certain that this stock will be a reliable source of income in the future.

The Dividend Has Limited Growth Potential

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. TVS Electronics' EPS has fallen by approximately 51% per year during the past five years. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future.

We're Not Big Fans Of TVS Electronics' Dividend

Overall, the dividend looks like it may have been a bit high, which explains why it has now been cut. The company seems to be stretching itself a bit to make such big payments, but it doesn't appear they can be consistent over time. The dividend doesn't inspire confidence that it will provide solid income in the future.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Just as an example, we've come across 3 warning signs for TVS Electronics you should be aware of, and 1 of them is a bit unpleasant. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if TVS Electronics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:TVSELECT

TVS Electronics

Through its subsidiaries, designs, manufactures, assembles, markets, sells, and services various products in India.

Mediocre balance sheet with very low risk.

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1941.1% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.6% undervalued

51 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4345.5% undervalued

16 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30154.5% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Silver One Resources ·

Silver One Resources, US$0.96/oz for 137Moz AgEq Past-Producing Silver Project, Eric Sprott Owns 15.61%

Fair Value:CA$2.584.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on Silver Storm Mining ·

A case for USD $26.00 (CAD 36.00) by 2030 with a MKT CAP of CAD$8.40 billion (USD$6.10) (10 bagger by Dec 2027)

Fair Value:CA$3698.8% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on First Mining Gold ·

First Mining Gold's competitive advantages in the mining sector.

Fair Value:CA$587.4% undervalued

23 followersusers have followed this narrative

4 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.6% undervalued

93 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5455.7% undervalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3455.9% undervalued

60 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

1

|0