Advertisement

- India

- /

- Electronic Equipment and Components

- /

- NSEI:PGEL

PG Electroplast (NSE:PGEL) Shareholders Will Want The ROCE Trajectory To Continue

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. With that in mind, we've noticed some promising trends at PG Electroplast (NSE:PGEL) so let's look a bit deeper.

What Is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for PG Electroplast:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

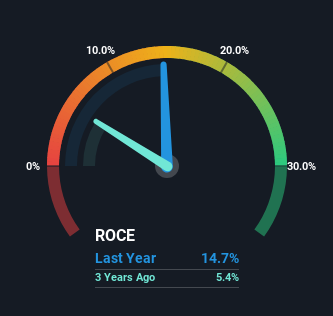

0.15 = ₹1.8b ÷ (₹16b - ₹4.2b) (Based on the trailing twelve months to September 2023).

Therefore, PG Electroplast has an ROCE of 15%. In absolute terms, that's a satisfactory return, but compared to the Electronic industry average of 12% it's much better.

Check out our latest analysis for PG Electroplast

In the above chart we have measured PG Electroplast's prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering PG Electroplast here for free.

What Can We Tell From PG Electroplast's ROCE Trend?

PG Electroplast is displaying some positive trends. The data shows that returns on capital have increased substantially over the last five years to 15%. The company is effectively making more money per dollar of capital used, and it's worth noting that the amount of capital has increased too, by 465%. So we're very much inspired by what we're seeing at PG Electroplast thanks to its ability to profitably reinvest capital.

In another part of our analysis, we noticed that the company's ratio of current liabilities to total assets decreased to 25%, which broadly means the business is relying less on its suppliers or short-term creditors to fund its operations. This tells us that PG Electroplast has grown its returns without a reliance on increasing their current liabilities, which we're very happy with.

Our Take On PG Electroplast's ROCE

A company that is growing its returns on capital and can consistently reinvest in itself is a highly sought after trait, and that's what PG Electroplast has. Since the stock has returned a staggering 2,016% to shareholders over the last five years, it looks like investors are recognizing these changes. So given the stock has proven it has promising trends, it's worth researching the company further to see if these trends are likely to persist.

One more thing to note, we've identified 1 warning sign with PG Electroplast and understanding this should be part of your investment process.

While PG Electroplast may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:PGEL

PG Electroplast

Provides electronic manufacturing services for original equipment manufacturers in India and internationally.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|8.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.6% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor