Advertisement

- India

- /

- Electronic Equipment and Components

- /

- NSEI:PGEL

Investors Appear Satisfied With PG Electroplast Limited's (NSE:PGEL) Prospects As Shares Rocket 36%

PG Electroplast Limited (NSE:PGEL) shares have continued their recent momentum with a 36% gain in the last month alone. The last 30 days bring the annual gain to a very sharp 71%.

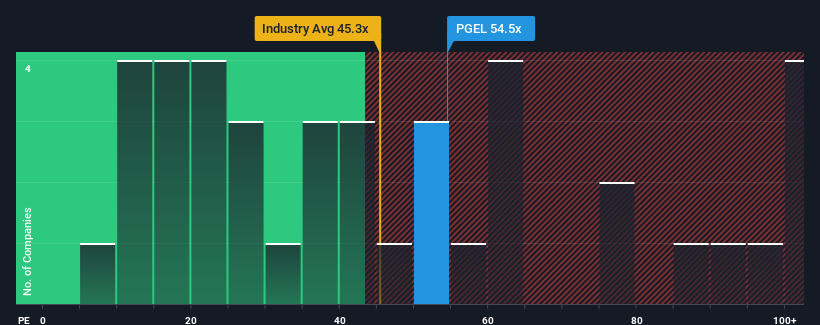

Since its price has surged higher, PG Electroplast's price-to-earnings (or "P/E") ratio of 54.5x might make it look like a strong sell right now compared to the market in India, where around half of the companies have P/E ratios below 30x and even P/E's below 17x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

With earnings growth that's superior to most other companies of late, PG Electroplast has been doing relatively well. The P/E is probably high because investors think this strong earnings performance will continue. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for PG Electroplast

Does Growth Match The High P/E?

The only time you'd be truly comfortable seeing a P/E as steep as PG Electroplast's is when the company's growth is on track to outshine the market decidedly.

Retrospectively, the last year delivered an exceptional 53% gain to the company's bottom line. The strong recent performance means it was also able to grow EPS by 769% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Turning to the outlook, the next year should generate growth of 47% as estimated by the three analysts watching the company. With the market only predicted to deliver 25%, the company is positioned for a stronger earnings result.

In light of this, it's understandable that PG Electroplast's P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

The strong share price surge has got PG Electroplast's P/E rushing to great heights as well. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that PG Electroplast maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

You always need to take note of risks, for example - PG Electroplast has 1 warning sign we think you should be aware of.

Of course, you might also be able to find a better stock than PG Electroplast. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:PGEL

PG Electroplast

Provides electronic manufacturing services for original equipment manufacturers in India and internationally.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor