Advertisement

- India

- /

- Electronic Equipment and Components

- /

- NSEI:KAYNES

Kaynes Technology India Limited (NSE:KAYNES) Not Flying Under The Radar

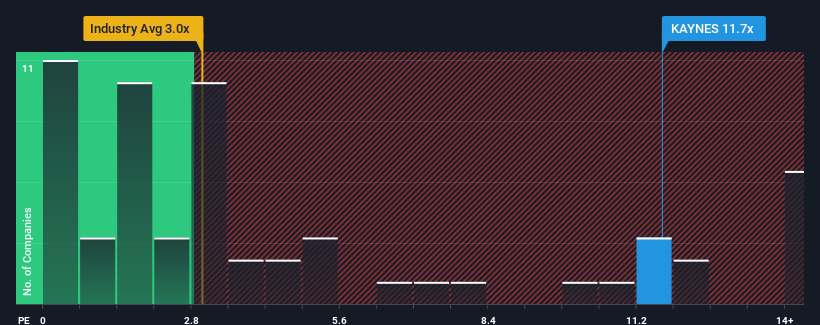

When close to half the companies in the Electronic industry in India have price-to-sales ratios (or "P/S") below 3x, you may consider Kaynes Technology India Limited (NSE:KAYNES) as a stock to avoid entirely with its 11.7x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

See our latest analysis for Kaynes Technology India

What Does Kaynes Technology India's P/S Mean For Shareholders?

With revenue growth that's superior to most other companies of late, Kaynes Technology India has been doing relatively well. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. However, if this isn't the case, investors might get caught out paying too much for the stock.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Kaynes Technology India.Is There Enough Revenue Growth Forecasted For Kaynes Technology India?

The only time you'd be truly comfortable seeing a P/S as steep as Kaynes Technology India's is when the company's growth is on track to outshine the industry decidedly.

Retrospectively, the last year delivered an exceptional 53% gain to the company's top line. The strong recent performance means it was also able to grow revenue by 263% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenue over that time.

Looking ahead now, revenue is anticipated to climb by 47% per annum during the coming three years according to the analysts following the company. That's shaping up to be materially higher than the 13% each year growth forecast for the broader industry.

With this in mind, it's not hard to understand why Kaynes Technology India's P/S is high relative to its industry peers. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Final Word

While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've established that Kaynes Technology India maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Electronic industry, as expected. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. Unless these conditions change, they will continue to provide strong support to the share price.

Before you take the next step, you should know about the 1 warning sign for Kaynes Technology India that we have uncovered.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Kaynes Technology India might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:KAYNES

Kaynes Technology India

Operates as an end-to-end and IoT solutions-enabled integrated electronics manufacturer in India and internationally.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|8.7% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.3% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor