Advertisement

Quicktouch Technologies Limited (NSE:QUICKTOUCH) Might Not Be As Mispriced As It Looks After Plunging 37%

Quicktouch Technologies Limited (NSE:QUICKTOUCH) shareholders that were waiting for something to happen have been dealt a blow with a 37% share price drop in the last month. The recent drop has obliterated the annual return, with the share price now down 6.4% over that longer period.

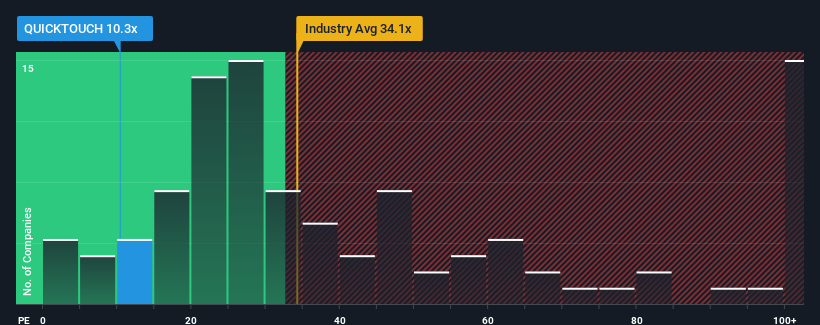

Since its price has dipped substantially, Quicktouch Technologies may be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 10.3x, since almost half of all companies in India have P/E ratios greater than 31x and even P/E's higher than 60x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

As an illustration, earnings have deteriorated at Quicktouch Technologies over the last year, which is not ideal at all. It might be that many expect the disappointing earnings performance to continue or accelerate, which has repressed the P/E. However, if this doesn't eventuate then existing shareholders may be feeling optimistic about the future direction of the share price.

See our latest analysis for Quicktouch Technologies

What Are Growth Metrics Telling Us About The Low P/E?

There's an inherent assumption that a company should far underperform the market for P/E ratios like Quicktouch Technologies' to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 31%. Still, the latest three year period has seen an excellent 738% overall rise in EPS, in spite of its unsatisfying short-term performance. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Comparing that to the market, which is only predicted to deliver 25% growth in the next 12 months, the company's momentum is stronger based on recent medium-term annualised earnings results.

In light of this, it's peculiar that Quicktouch Technologies' P/E sits below the majority of other companies. Apparently some shareholders believe the recent performance has exceeded its limits and have been accepting significantly lower selling prices.

The Bottom Line On Quicktouch Technologies' P/E

Quicktouch Technologies' P/E looks about as weak as its stock price lately. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our examination of Quicktouch Technologies revealed its three-year earnings trends aren't contributing to its P/E anywhere near as much as we would have predicted, given they look better than current market expectations. When we see strong earnings with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. It appears many are indeed anticipating earnings instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

There are also other vital risk factors to consider before investing and we've discovered 3 warning signs for Quicktouch Technologies that you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if Quicktouch Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:QUICKTOUCH

Quicktouch Technologies

Engages in the development and trading of computer software and related activities primarily in India.

Slight risk with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.563.6% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75032.0% undervalued

76 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.4% undervalued

66 followersusers have followed this narrative

4 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2779.9% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Abitibi Metals ·

Abitibi Metals’ High-Grade B26 Polymetallic Deposit Trading at a Fraction of Peers, 96% Undervalued?

Fair Value:CA$1.2950.4% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

EV

everyseed on Zylox-Tonbridge Medical Technology ·

Zylox-Tonbridge: Early Signs of an Emerging Global Vascular Intervention Platform

Fair Value:HK$30.8539.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

Anthony_Lee on Geohan Corporation Berhad ·

Geohan's Growth Outlook Brightens on Expanding Order Book and Easing Cost Pressures

Fair Value:RM 0.7460.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75032.0% undervalued

76 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.5% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.3% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative