Advertisement

Many Would Be Envious Of Happiest Minds Technologies' (NSE:HAPPSTMNDS) Excellent Returns On Capital

If you're looking for a multi-bagger, there's a few things to keep an eye out for. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. Ergo, when we looked at the ROCE trends at Happiest Minds Technologies (NSE:HAPPSTMNDS), we liked what we saw.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for Happiest Minds Technologies, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

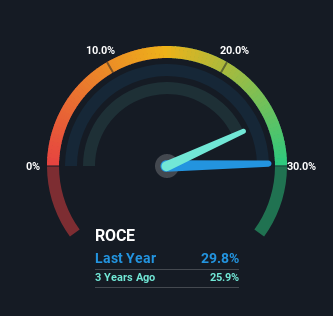

0.30 = ₹3.2b ÷ (₹16b - ₹5.8b) (Based on the trailing twelve months to March 2023).

So, Happiest Minds Technologies has an ROCE of 30%. That's a fantastic return and not only that, it outpaces the average of 15% earned by companies in a similar industry.

Check out our latest analysis for Happiest Minds Technologies

In the above chart we have measured Happiest Minds Technologies' prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Happiest Minds Technologies here for free.

SWOT Analysis for Happiest Minds Technologies

Strength

- Earnings growth over the past year exceeded the industry.

- Debt is not viewed as a risk.

Weakness

- Earnings growth over the past year is below its 5-year average.

- Dividend is low compared to the top 25% of dividend payers in the IT market.

- Expensive based on P/E ratio and estimated fair value.

Opportunity

- Annual earnings are forecast to grow faster than the Indian market.

Threat

- Dividends are not covered by cash flow.

- Revenue is forecast to grow slower than 20% per year.

The Trend Of ROCE

Happiest Minds Technologies deserves to be commended in regards to it's returns. The company has employed 259% more capital in the last three years, and the returns on that capital have remained stable at 30%. Returns like this are the envy of most businesses and given it has repeatedly reinvested at these rates, that's even better. If these trends can continue, it wouldn't surprise us if the company became a multi-bagger.

The Bottom Line

In summary, we're delighted to see that Happiest Minds Technologies has been compounding returns by reinvesting at consistently high rates of return, as these are common traits of a multi-bagger. Despite the good fundamentals, total returns from the stock have been virtually flat over the last year. That's why we think it'd be worthwhile to look further into this stock given the fundamentals are appealing.

Since virtually every company faces some risks, it's worth knowing what they are, and we've spotted 2 warning signs for Happiest Minds Technologies (of which 1 is significant!) that you should know about.

Happiest Minds Technologies is not the only stock earning high returns. If you'd like to see more, check out our free list of companies earning high returns on equity with solid fundamentals.

Valuation is complex, but we're here to simplify it.

Discover if Happiest Minds Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:HAPPSTMNDS

Happiest Minds Technologies

Provides information technology (IT) solutions and services in India, the Americas, Australia, Europe, Asia, the Middle East, and Africa.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor