Advertisement

Dev Information Technology Limited's (NSE:DEVIT) Stock Has Been Sliding But Fundamentals Look Strong: Is The Market Wrong?

It is hard to get excited after looking at Dev Information Technology's (NSE:DEVIT) recent performance, when its stock has declined 24% over the past month. However, stock prices are usually driven by a company’s financial performance over the long term, which in this case looks quite promising. Specifically, we decided to study Dev Information Technology's ROE in this article.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

View our latest analysis for Dev Information Technology

How Do You Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Dev Information Technology is:

20% = ₹88m ÷ ₹448m (Based on the trailing twelve months to December 2023).

The 'return' is the profit over the last twelve months. So, this means that for every ₹1 of its shareholder's investments, the company generates a profit of ₹0.20.

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Dev Information Technology's Earnings Growth And 20% ROE

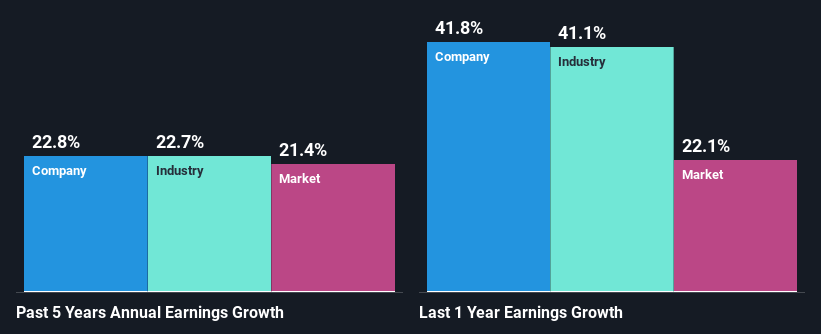

To start with, Dev Information Technology's ROE looks acceptable. Further, the company's ROE compares quite favorably to the industry average of 16%. This probably laid the ground for Dev Information Technology's significant 23% net income growth seen over the past five years. We believe that there might also be other aspects that are positively influencing the company's earnings growth. For example, it is possible that the company's management has made some good strategic decisions, or that the company has a low payout ratio.

We then performed a comparison between Dev Information Technology's net income growth with the industry, which revealed that the company's growth is similar to the average industry growth of 23% in the same 5-year period.

Earnings growth is an important metric to consider when valuing a stock. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is Dev Information Technology fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Dev Information Technology Efficiently Re-investing Its Profits?

Dev Information Technology has a really low three-year median payout ratio of 19%, meaning that it has the remaining 81% left over to reinvest into its business. So it seems like the management is reinvesting profits heavily to grow its business and this reflects in its earnings growth number.

Additionally, Dev Information Technology has paid dividends over a period of six years which means that the company is pretty serious about sharing its profits with shareholders.

Conclusion

Overall, we are quite pleased with Dev Information Technology's performance. In particular, it's great to see that the company is investing heavily into its business and along with a high rate of return, that has resulted in a sizeable growth in its earnings. If the company continues to grow its earnings the way it has, that could have a positive impact on its share price given how earnings per share influence long-term share prices. Not to forget, share price outcomes are also dependent on the potential risks a company may face. So it is important for investors to be aware of the risks involved in the business. You can see the 2 risks we have identified for Dev Information Technology by visiting our risks dashboard for free on our platform here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:DEVIT

Dev Information Technology

Provides information technology enabled services in India, Europe, and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.888.1% undervalued

48 followersusers have followed this narrative

3 commentsusers have commented on this narrative

21 likesusers have liked this narrative

TO

Tokyo on LVMH Moët Hennessy - Louis Vuitton Société Européenne ·

EU#4 - Turning Heritage into the World’s Strongest Luxury Empire

Fair Value:€750.0428.5% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

WE

WealthAP on Alphabet ·

The "Easy Money" Is Gone: Why Alphabet Is Now a "Show Me" Story

Fair Value:US$386.4316.5% undervalued

64 followersusers have followed this narrative

1 commentusers have commented on this narrative

19 likesusers have liked this narrative

Recently Updated Narratives

SE

SelectiveCapital on FactSet Research Systems ·

Future PE of 12.8x Shines Bright for FactSet Growth

Fair Value:US$313.9934.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Brookfield Infrastructure ·

BIPC: A strategic player in the energy crisis, a hybrid of Utility and Digital REIT.

Fair Value:US$57.1412.5% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

alex30free on Indutrade ·

Quintessential serial acquirer

Fair Value:SEK 256.868.9% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OO

OOO97 on Neo Performance Materials ·

Undervalued Key Player in Magnets/Rare Earth

Fair Value:CA$25.3322.3% undervalued

75 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.888.1% undervalued

48 followersusers have followed this narrative

3 commentsusers have commented on this narrative

21 likesusers have liked this narrative

WE

WealthAP on PayPal Holdings ·

The "Sleeping Giant" Stumbles, Then Wakes Up

Fair Value:US$8250.7% undervalued

88 followersusers have followed this narrative

6 commentsusers have commented on this narrative

35 likesusers have liked this narrative

Trending Discussion

KA

Kalibrator on Ubisoft Entertainment ·

As a gamer, I would not touch this company now. They are hated by the community and have been releasing major flops on their AAA games during the last 5 years (for good reasons). It is true that the valuation is ridiculously low compared to what the licenses are worth, but if the trend continues the value of those will also decline. Management needs to almost make a 180° turnaround to get things right. I agree that a take-private deal before it is too late might be the best option for an investor entering today. We might also see a split sales of the different studios. It is a very risky play, but potentially with high reward.

1

|0

CG

CGHHDEEU2026 on LANXESS ·

It is very interesting to overlook the how strongly the fair values assessed by various analysists divergent (based on HANDELSBLATT today): Barclays 14€, GoldmanIt Sachs 10€, UBS 14€, Jeffries 17€, Berenberg 18€, Warburg € 21, Deutsche Bank 27€. So, Anglo-Saxon analysts are much less optimistic than their continental European colleagues. Yesterday the Lanxess share price jumped by 11 percent. Hopefully it won't be a one-off event...

0

|0