Advertisement

- India

- /

- Semiconductors

- /

- NSEI:WEBELSOLAR

We Like These Underlying Return On Capital Trends At Websol Energy System (NSE:WEBELSOLAR)

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. So on that note, Websol Energy System (NSE:WEBELSOLAR) looks quite promising in regards to its trends of return on capital.

What is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for Websol Energy System:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.11 = ₹227m ÷ (₹2.8b - ₹722m) (Based on the trailing twelve months to March 2021).

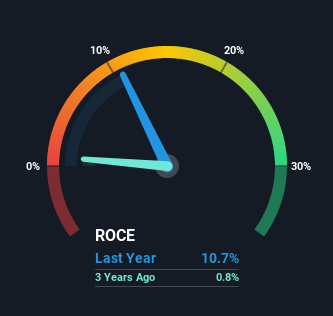

So, Websol Energy System has an ROCE of 11%. In absolute terms, that's a satisfactory return, but compared to the Semiconductor industry average of 7.3% it's much better.

See our latest analysis for Websol Energy System

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating Websol Energy System's past further, check out this free graph of past earnings, revenue and cash flow.

So How Is Websol Energy System's ROCE Trending?

Websol Energy System has recently broken into profitability so their prior investments seem to be paying off. Shareholders would no doubt be pleased with this because the business was loss-making five years ago but is is now generating 11% on its capital. And unsurprisingly, like most companies trying to break into the black, Websol Energy System is utilizing 219% more capital than it was five years ago. This can tell us that the company has plenty of reinvestment opportunities that are able to generate higher returns.

On a related note, the company's ratio of current liabilities to total assets has decreased to 25%, which basically reduces it's funding from the likes of short-term creditors or suppliers. This tells us that Websol Energy System has grown its returns without a reliance on increasing their current liabilities, which we're very happy with.

What We Can Learn From Websol Energy System's ROCE

Long story short, we're delighted to see that Websol Energy System's reinvestment activities have paid off and the company is now profitable. Investors may not be impressed by the favorable underlying trends yet because over the last five years the stock has only returned 12% to shareholders. Given that, we'd look further into this stock in case it has more traits that could make it multiply in the long term.

On a final note, we've found 2 warning signs for Websol Energy System that we think you should be aware of.

While Websol Energy System may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

When trading Websol Energy System or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Websol Energy System might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:WEBELSOLAR

Websol Energy System

Manufactures and sells solar photovoltaic (PV) cells and modules in India.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor