Stock Analysis

These 4 Measures Indicate That Themis Medicare (NSE:THEMISMED) Is Using Debt Reasonably Well

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Themis Medicare Limited (NSE:THEMISMED) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Themis Medicare

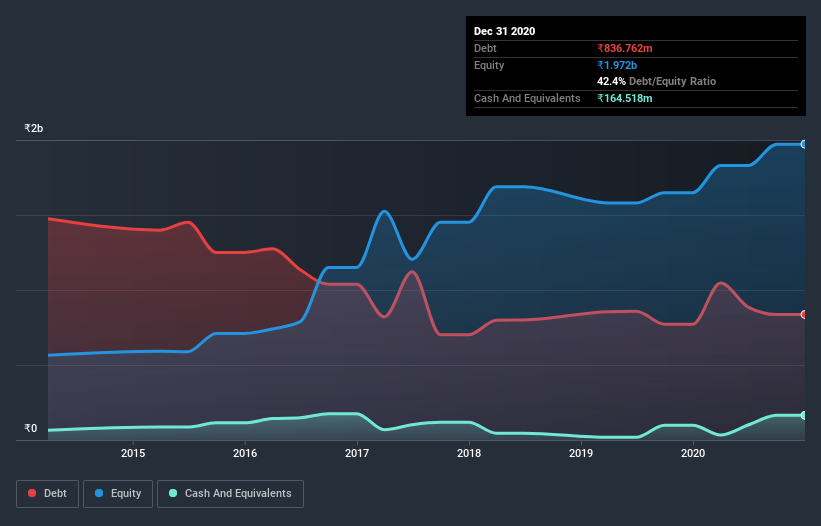

What Is Themis Medicare's Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of September 2020 Themis Medicare had ₹832.2m of debt, an increase on ₹771.7m, over one year. However, it also had ₹164.5m in cash, and so its net debt is ₹667.7m.

A Look At Themis Medicare's Liabilities

Zooming in on the latest balance sheet data, we can see that Themis Medicare had liabilities of ₹1.38b due within 12 months and liabilities of ₹212.4m due beyond that. On the other hand, it had cash of ₹164.5m and ₹922.2m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₹502.7m.

Of course, Themis Medicare has a market capitalization of ₹2.83b, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Looking at its net debt to EBITDA of 1.3 and interest cover of 3.9 times, it seems to us that Themis Medicare is probably using debt in a pretty reasonable way. So we'd recommend keeping a close eye on the impact financing costs are having on the business. Notably, Themis Medicare's EBIT launched higher than Elon Musk, gaining a whopping 428% on last year. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Themis Medicare will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. In the last three years, Themis Medicare's free cash flow amounted to 31% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

The good news is that Themis Medicare's demonstrated ability to grow its EBIT delights us like a fluffy puppy does a toddler. But truth be told we feel its interest cover does undermine this impression a bit. All these things considered, it appears that Themis Medicare can comfortably handle its current debt levels. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it's worth keeping an eye on this one. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 4 warning signs for Themis Medicare you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you decide to trade Themis Medicare, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're helping make it simple.

Find out whether Themis Medicare is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:THEMISMED

Themis Medicare

Manufactures and sells pharmaceutical products in India and internationally.

Flawless balance sheet with questionable track record.