Advertisement

Exploring Three Indian Exchange Stocks With Intrinsic Value Discounts Ranging From 18.4% To 42.7%

Simply Wall St

Reviewed by Simply Wall St

The Indian stock market has experienced a slight dip of 1.3% over the past week, yet it maintains a robust annual growth of 43%, with earnings expected to grow by 16% annually. In this context, identifying stocks that are undervalued relative to their intrinsic value can be particularly compelling for investors looking for potential opportunities in a growing market.

Top 10 Undervalued Stocks Based On Cash Flows In India

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| HEG (NSEI:HEG) | ₹2045.25 | ₹3292.68 | 37.9% |

| IOL Chemicals and Pharmaceuticals (BSE:524164) | ₹403.15 | ₹636.71 | 36.7% |

| Updater Services (NSEI:UDS) | ₹309.35 | ₹538.16 | 42.5% |

| Vedanta (NSEI:VEDL) | ₹439.80 | ₹717.96 | 38.7% |

| Rajesh Exports (NSEI:RAJESHEXPO) | ₹300.90 | ₹506.76 | 40.6% |

| Mahindra Logistics (NSEI:MAHLOG) | ₹512.70 | ₹901.81 | 43.1% |

| Strides Pharma Science (NSEI:STAR) | ₹952.70 | ₹1664.05 | 42.7% |

| Delhivery (NSEI:DELHIVERY) | ₹374.30 | ₹740.20 | 49.4% |

| Godrej Properties (NSEI:GODREJPROP) | ₹3245.75 | ₹5592.14 | 42% |

| PVR INOX (NSEI:PVRINOX) | ₹1402.50 | ₹2538.40 | 44.7% |

Let's dive into some prime choices out of from the screener.

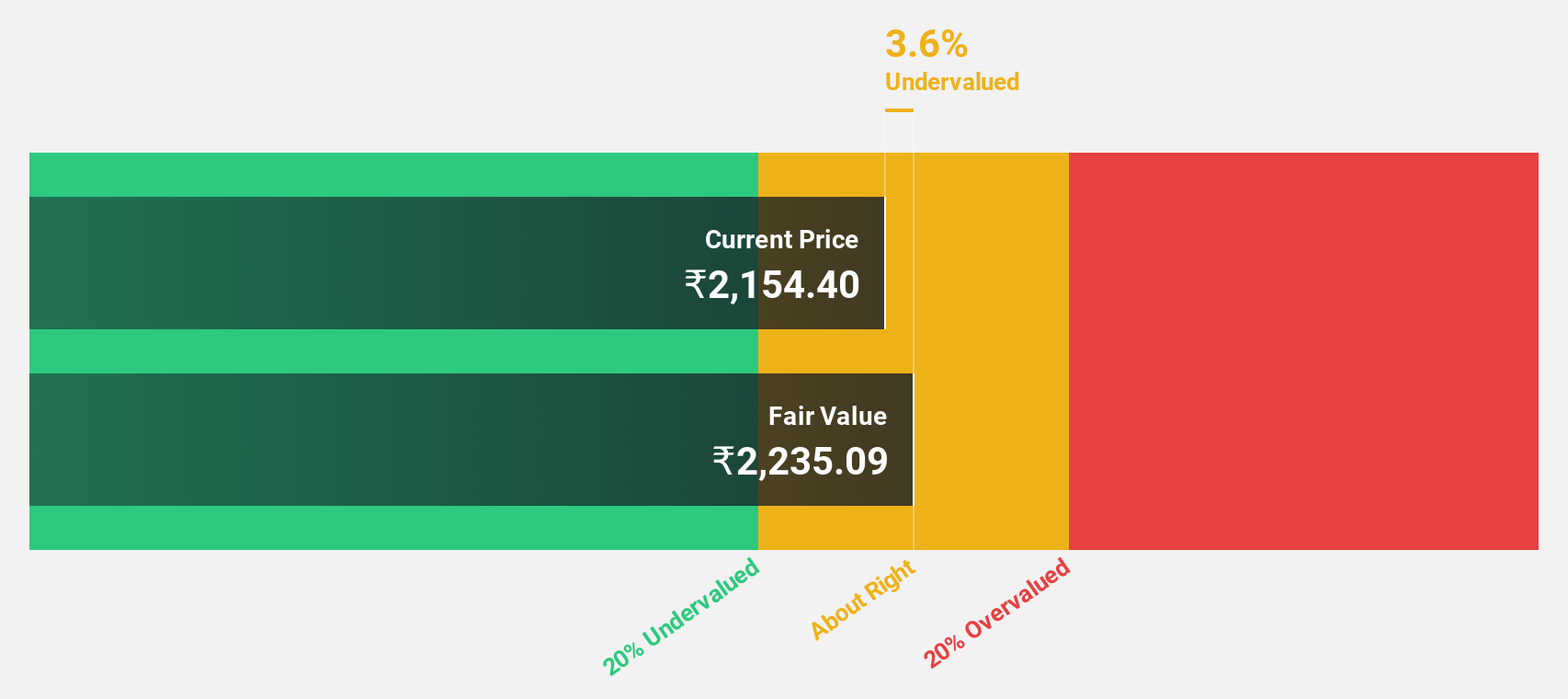

Dalmia Bharat (NSEI:DALBHARAT)

Overview: Dalmia Bharat Limited, along with its subsidiaries, specializes in producing and marketing clinker and cement products mainly in India, boasting a market capitalization of approximately ₹341.09 billion.

Operations: The company primarily generates revenue from the production and sale of clinker and cement products in India.

Estimated Discount To Fair Value: 18.4%

Dalmia Bharat, trading at ₹1818.7, is perceived as undervalued against a fair value estimate of ₹2230.13, marking an 18.4% discrepancy. Despite slower revenue growth projections at 10.8% annually compared to the broader market's 9.6%, its earnings are expected to surge by approximately 21.33% per year over the next three years, outpacing the Indian market forecast of 15.9%. However, its dividend yield of 0.49% raises concerns over sustainability due to inadequate coverage by free cash flows and a modest forecasted Return on Equity (ROE) of only around 7%.

- The analysis detailed in our Dalmia Bharat growth report hints at robust future financial performance.

- Delve into the full analysis health report here for a deeper understanding of Dalmia Bharat.

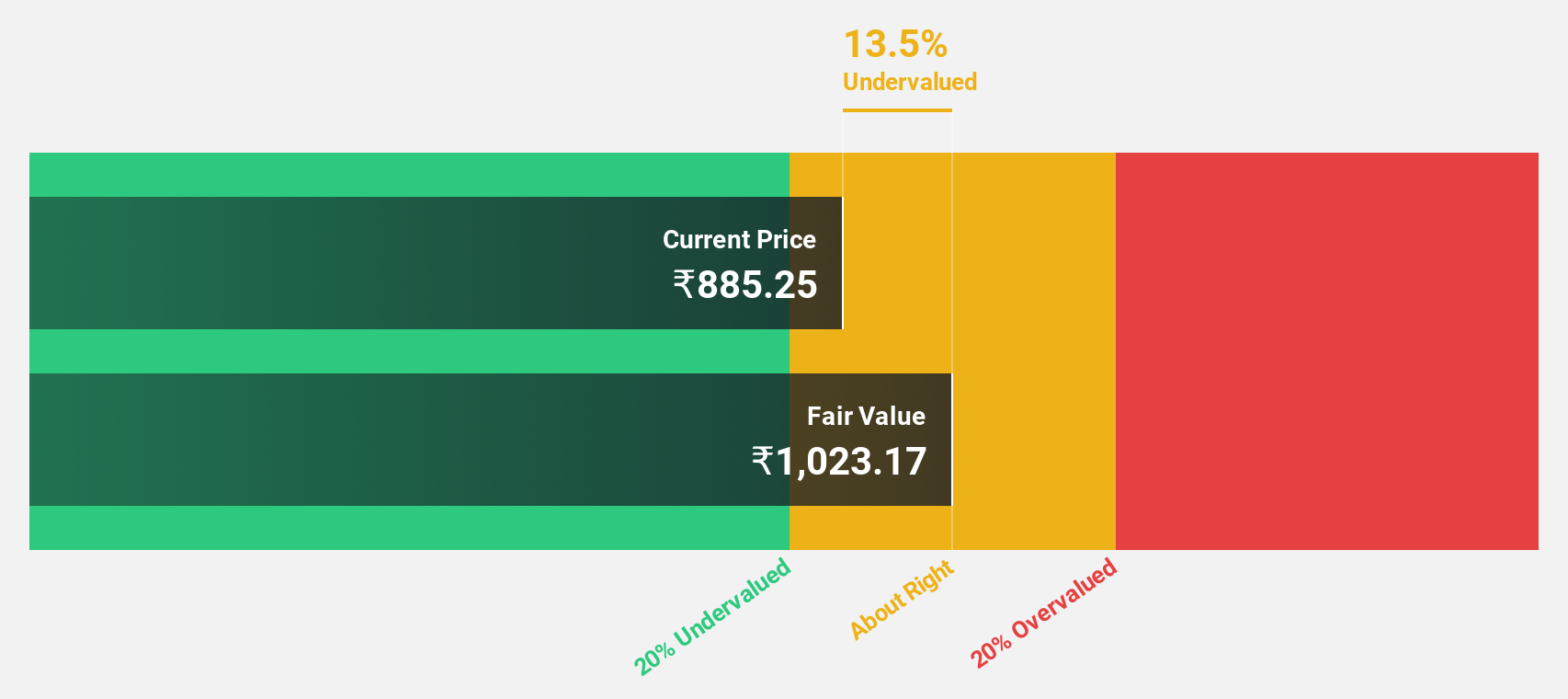

Strides Pharma Science (NSEI:STAR)

Overview: Strides Pharma Science Limited is a pharmaceutical company that develops, manufactures, and sells products across multiple continents including Africa, Australia, North America, Europe, and Asia with a market capitalization of approximately ₹87.57 billion.

Operations: The company generates ₹40.51 billion from its pharmaceutical business, excluding the bio-pharmaceutical segment.

Estimated Discount To Fair Value: 42.7%

Strides Pharma Science, with a current market price of ₹952.7, is assessed to be trading at 42.7% below its calculated fair value of ₹1664.05, indicating a significant undervaluation based on discounted cash flow analysis. Despite this potential for value, the company's expected revenue growth rate at 11.2% annually falls short of the high-growth benchmark of 20%, though it surpasses India's market average growth forecast of 9.6%. Additionally, Strides is projected to transition into profitability within the next three years with an anticipated profit increase substantially above average market expectations.

- Our growth report here indicates Strides Pharma Science may be poised for an improving outlook.

- Dive into the specifics of Strides Pharma Science here with our thorough financial health report.

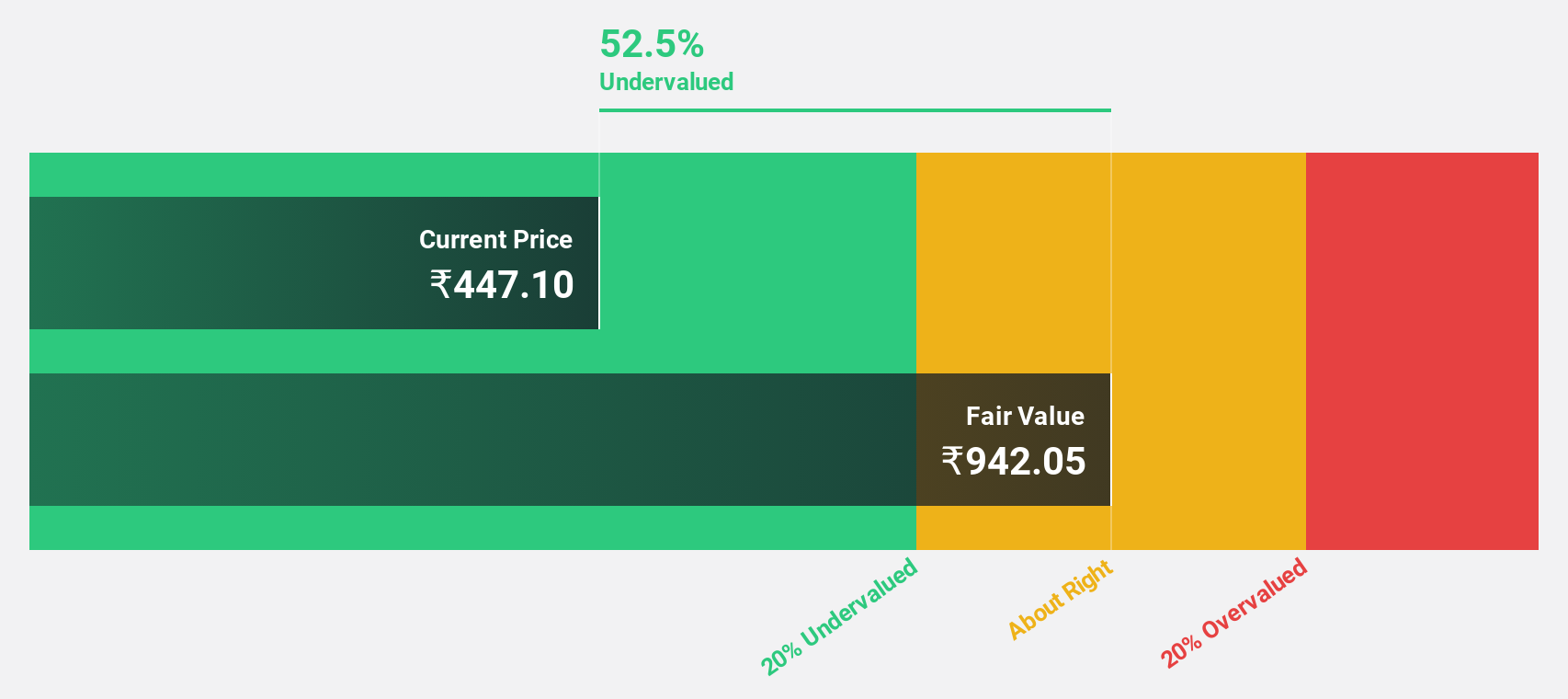

Vedanta (NSEI:VEDL)

Overview: Vedanta Limited is a diversified natural resources company that operates in the exploration, extraction, and processing of minerals and oil and gas across India, Europe, China, the United States, Mexico, and other international markets, with a market cap of approximately ₹1.72 trillion.

Operations: The company's revenue is primarily derived from its Aluminium, Zinc - India, Copper, Oil and Gas, Iron Ore, and Power segments which collectively contribute ₹1.17 billion.

Estimated Discount To Fair Value: 38.7%

Vedanta Limited, priced at INR 439.8, appears undervalued by 38.7% against a fair value estimate of INR 717.96 based on discounted cash flow analysis, suggesting potential for appreciation. Recent strategic moves include a substantial private placement aimed at raising up to INR 80 billion if oversubscribed, indicating robust financing activities and future capital deployment strategies. Despite this, Vedanta's dividend sustainability is questionable as its current yield is poorly covered by earnings, reflecting a payout that may not be maintainable without adjustments in operational efficiency or profit margins. Additionally, while the company's earnings are expected to grow significantly at an annual rate of 43.25%, this contrasts with more modest revenue growth forecasts and a high debt level that could constrain financial flexibility.

- Upon reviewing our latest growth report, Vedanta's projected financial performance appears quite optimistic.

- Unlock comprehensive insights into our analysis of Vedanta stock in this financial health report.

Where To Now?

- Click here to access our complete index of 20 Undervalued Indian Stocks Based On Cash Flows.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:STAR

Strides Pharma Science

Develops, manufactures, and sells pharmaceutical products in Africa, Australia, North America, Europe, Asia, and internationally.

Undervalued with high growth potential and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor