Advertisement

Medico Remedies Limited (NSE:MEDICO) Shares Slammed 33% But Getting In Cheap Might Be Difficult Regardless

Medico Remedies Limited (NSE:MEDICO) shareholders that were waiting for something to happen have been dealt a blow with a 33% share price drop in the last month. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 28% in that time.

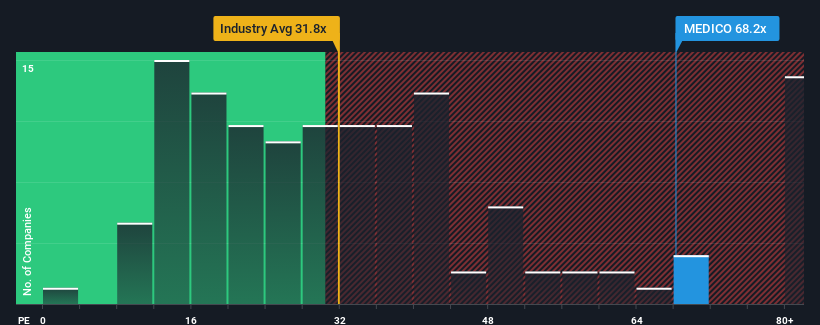

Although its price has dipped substantially, given close to half the companies in India have price-to-earnings ratios (or "P/E's") below 28x, you may still consider Medico Remedies as a stock to avoid entirely with its 68.2x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

For example, consider that Medico Remedies' financial performance has been poor lately as its earnings have been in decline. One possibility is that the P/E is high because investors think the company will still do enough to outperform the broader market in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Medico Remedies

Does Growth Match The High P/E?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Medico Remedies' to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 6.9%. Still, the latest three year period has seen an excellent 175% overall rise in EPS, in spite of its unsatisfying short-term performance. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 24% shows it's noticeably more attractive on an annualised basis.

With this information, we can see why Medico Remedies is trading at such a high P/E compared to the market. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

The Key Takeaway

Even after such a strong price drop, Medico Remedies' P/E still exceeds the rest of the market significantly. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Medico Remedies maintains its high P/E on the strength of its recent three-year growth being higher than the wider market forecast, as expected. Right now shareholders are comfortable with the P/E as they are quite confident earnings aren't under threat. Unless the recent medium-term conditions change, they will continue to provide strong support to the share price.

We don't want to rain on the parade too much, but we did also find 1 warning sign for Medico Remedies that you need to be mindful of.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:MEDICO

Medico Remedies

Develops, manufactures, and sells pharmaceutical and nutraceutical products in India.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|31.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|44.7% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|40.9% undervalued

AG

Community Contributor