Advertisement

Shaky Earnings May Not Tell The Whole Story For Infinium Pharmachem (NSE:INFINIUM)

Infinium Pharmachem Limited's (NSE:INFINIUM) lackluster earnings announcement last week disappointed investors. We think that they may have more to worry about than just soft profit numbers.

A Closer Look At Infinium Pharmachem's Earnings

In high finance, the key ratio used to measure how well a company converts reported profits into free cash flow (FCF) is the accrual ratio (from cashflow). In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

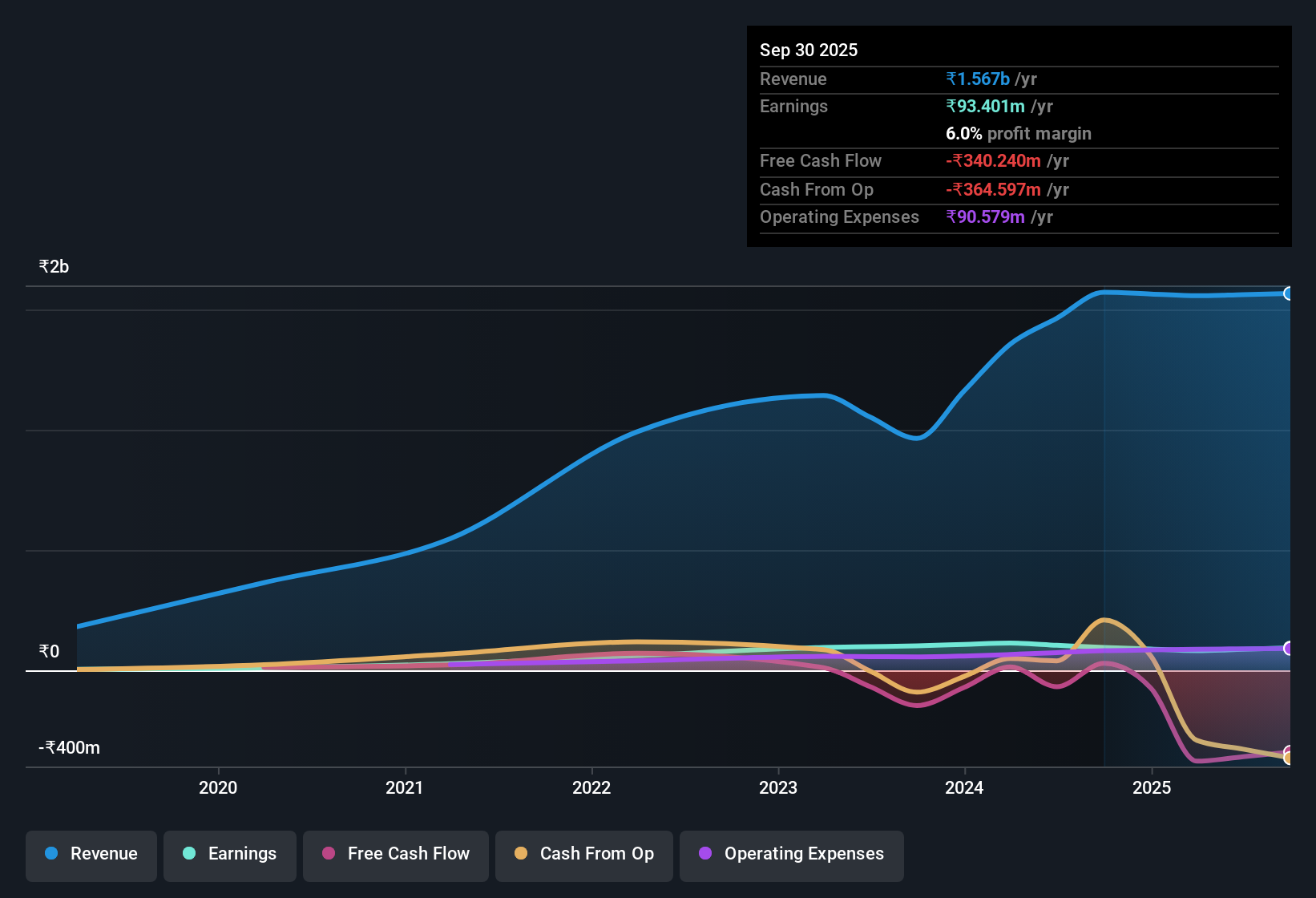

Infinium Pharmachem has an accrual ratio of 0.44 for the year to September 2025. Statistically speaking, that's a real negative for future earnings. To wit, the company did not generate one whit of free cashflow in that time. Over the last year it actually had negative free cash flow of ₹340m, in contrast to the aforementioned profit of ₹93.4m. We saw that FCF was ₹29m a year ago though, so Infinium Pharmachem has at least been able to generate positive FCF in the past. Notably, the company has issued new shares, thus diluting existing shareholders and reducing their share of future earnings.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Infinium Pharmachem.

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. Infinium Pharmachem expanded the number of shares on issue by 12% over the last year. That means its earnings are split among a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. You can see a chart of Infinium Pharmachem's EPS by clicking here.

A Look At The Impact Of Infinium Pharmachem's Dilution On Its Earnings Per Share (EPS)

Infinium Pharmachem has improved its profit over the last three years, with an annualized gain of 20% in that time. In contrast, earnings per share were actually down by 21% per year, in the exact same period. While we did see a very small decrease, net profit was basically flat over the last year. In contrast, earnings per share are actually down a full 11%, over the last twelve months. Therefore, the dilution is having a noteworthy influence on shareholder returns.

If Infinium Pharmachem's EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Our Take On Infinium Pharmachem's Profit Performance

As it turns out, Infinium Pharmachem couldn't match its profit with cashflow and its dilution means that shareholders own less of the company than the did before (unless they bought more shares). Considering all this we'd argue Infinium Pharmachem's profits probably give an overly generous impression of its sustainable level of profitability. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. For instance, we've identified 2 warning signs for Infinium Pharmachem (1 makes us a bit uncomfortable) you should be familiar with.

Our examination of Infinium Pharmachem has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:INFINIUM

Infinium Pharmachem

Engages in the manufacture and supply of iodine, iodine derivatives, and active pharmaceutical ingredients (APIs) in India and internationally.

Flawless balance sheet with very low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor