Advertisement

We're Not So Sure You Should Rely on Ind-Swift Laboratories's (NSE:INDSWFTLAB) Statutory Earnings

Broadly speaking, profitable businesses are less risky than unprofitable ones. That said, the current statutory profit is not always a good guide to a company's underlying profitability. Today we'll focus on whether this year's statutory profits are a good guide to understanding Ind-Swift Laboratories (NSE:INDSWFTLAB).

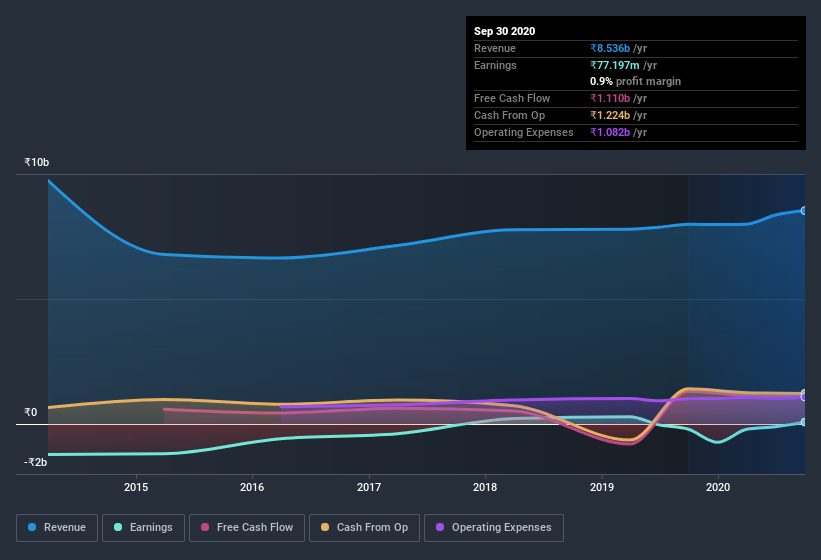

It's good to see that over the last twelve months Ind-Swift Laboratories made a profit of ₹77.2m on revenue of ₹8.54b. The good news is that the company managed to grow its revenue over the last three years, and also move from loss-making to profitable.

Check out our latest analysis for Ind-Swift Laboratories

Importantly, statutory profits are not always the best tool for understanding a company's true earnings power, so it's well worth examining profits in a little more detail. In this article we will consider how Ind-Swift Laboratories' decision to issue new shares in the company has impacted returns to shareholders. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Ind-Swift Laboratories.

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. Ind-Swift Laboratories expanded the number of shares on issue by 24% over the last year. As a result, its net income is now split between a greater number of shares. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. Check out Ind-Swift Laboratories' historical EPS growth by clicking on this link.

How Is Dilution Impacting Ind-Swift Laboratories' Earnings Per Share? (EPS)

Three years ago, Ind-Swift Laboratories lost money. Zooming in to the last year, we still can't talk about growth rates coherently, since it made a loss last year. But mathematics aside, it is always good to see when a formerly unprofitable business come good (though we accept profit would have been higher if dilution had not been required). Therefore, one can observe that the dilution is having a fairly profound effect on shareholder returns.

If Ind-Swift Laboratories' EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Our Take On Ind-Swift Laboratories' Profit Performance

Ind-Swift Laboratories issued shares during the year, and that means its EPS performance lags its net income growth. Because of this, we think that it may be that Ind-Swift Laboratories' statutory profits are better than its underlying earnings power. On the bright side, the company showed enough improvement to book a profit this year, after losing money last year. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. Keep in mind, when it comes to analysing a stock it's worth noting the risks involved. To that end, you should learn about the 5 warning signs we've spotted with Ind-Swift Laboratories (including 1 which can't be ignored).

This note has only looked at a single factor that sheds light on the nature of Ind-Swift Laboratories' profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you decide to trade Ind-Swift Laboratories, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:INDSWFTLAB

Ind-Swift Laboratories

Develops, manufactures, and sells active pharmaceutical ingredients (APIs), intermediates, and formulations in India and internationally.

Adequate balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor