Advertisement

- India

- /

- Basic Materials

- /

- NSEI:UDAICEMENT

Returns On Capital Signal Tricky Times Ahead For Udaipur Cement Works (NSE:UDAICEMENT)

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. However, after briefly looking over the numbers, we don't think Udaipur Cement Works (NSE:UDAICEMENT) has the makings of a multi-bagger going forward, but let's have a look at why that may be.

What Is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on Udaipur Cement Works is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

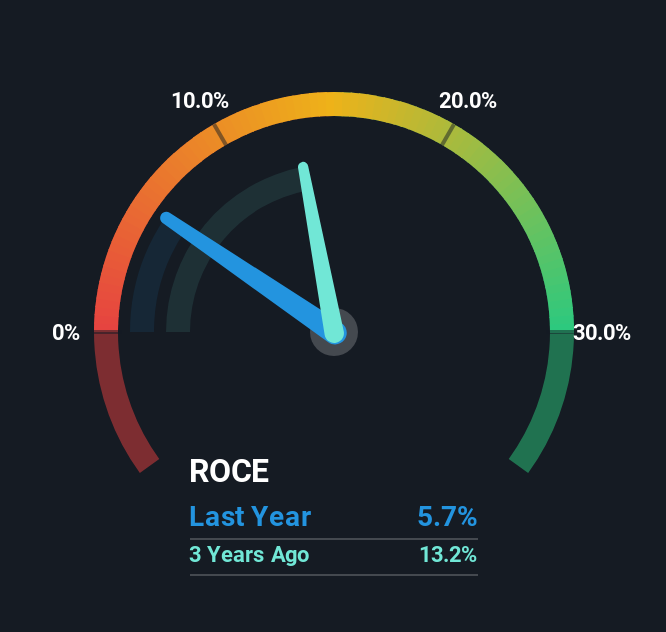

0.057 = ₹1.3b ÷ (₹27b - ₹3.7b) (Based on the trailing twelve months to March 2025).

Therefore, Udaipur Cement Works has an ROCE of 5.7%. On its own that's a low return on capital but it's in line with the industry's average returns of 5.5%.

Check out our latest analysis for Udaipur Cement Works

Historical performance is a great place to start when researching a stock so above you can see the gauge for Udaipur Cement Works' ROCE against it's prior returns. If you'd like to look at how Udaipur Cement Works has performed in the past in other metrics, you can view this free graph of Udaipur Cement Works' past earnings, revenue and cash flow.

What The Trend Of ROCE Can Tell Us

When we looked at the ROCE trend at Udaipur Cement Works, we didn't gain much confidence. Around five years ago the returns on capital were 17%, but since then they've fallen to 5.7%. However, given capital employed and revenue have both increased it appears that the business is currently pursuing growth, at the consequence of short term returns. If these investments prove successful, this can bode very well for long term stock performance.

On a side note, Udaipur Cement Works has done well to pay down its current liabilities to 14% of total assets. That could partly explain why the ROCE has dropped. Effectively this means their suppliers or short-term creditors are funding less of the business, which reduces some elements of risk. Since the business is basically funding more of its operations with it's own money, you could argue this has made the business less efficient at generating ROCE.

In Conclusion...

While returns have fallen for Udaipur Cement Works in recent times, we're encouraged to see that sales are growing and that the business is reinvesting in its operations. Furthermore the stock has climbed 54% over the last three years, it would appear that investors are upbeat about the future. So should these growth trends continue, we'd be optimistic on the stock going forward.

One more thing: We've identified 3 warning signs with Udaipur Cement Works (at least 2 which are a bit unpleasant) , and understanding these would certainly be useful.

While Udaipur Cement Works may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:UDAICEMENT

Udaipur Cement Works

Manufactures and supplies cement and cementitious products in India.

Slight risk and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.1% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.04% overvalued

LI

Community Contributor