Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Tata Metaliks Limited (NSE:TATAMETALI) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Tata Metaliks

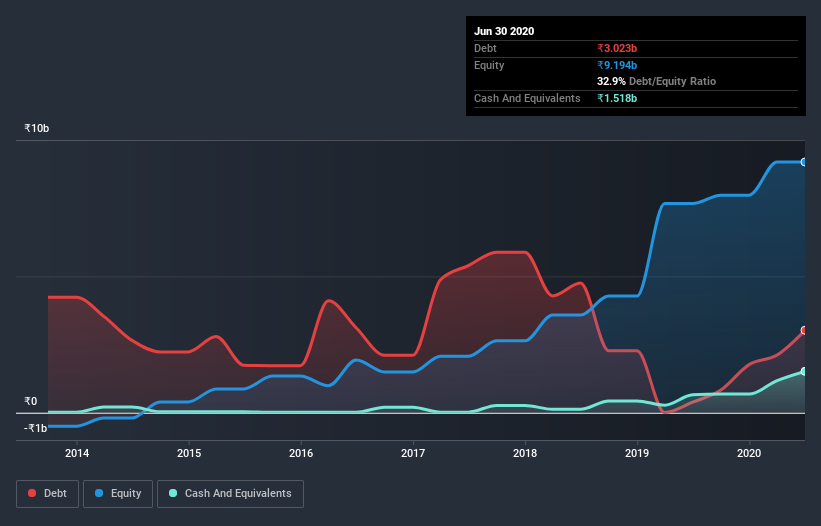

How Much Debt Does Tata Metaliks Carry?

As you can see below, at the end of March 2020, Tata Metaliks had ₹2.11b of debt, up from ₹385.3m a year ago. Click the image for more detail. On the flip side, it has ₹1.52b in cash leading to net debt of about ₹595.9m.

How Strong Is Tata Metaliks's Balance Sheet?

According to the last reported balance sheet, Tata Metaliks had liabilities of ₹6.71b due within 12 months, and liabilities of ₹1.04b due beyond 12 months. Offsetting these obligations, it had cash of ₹1.52b as well as receivables valued at ₹2.81b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₹3.4b.

Tata Metaliks has a market capitalization of ₹15.0b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While Tata Metaliks's low debt to EBITDA ratio of 0.23 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 5.7 times last year does give us pause. But the interest payments are certainly sufficient to have us thinking about how affordable its debt is. Unfortunately, Tata Metaliks's EBIT flopped 19% over the last four quarters. If earnings continue to decline at that rate then handling the debt will be more difficult than taking three children under 5 to a fancy pants restaurant. When analysing debt levels, the balance sheet is the obvious place to start. But it is Tata Metaliks's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. In the last three years, Tata Metaliks's free cash flow amounted to 36% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Our View

Tata Metaliks's struggle to grow its EBIT had us second guessing its balance sheet strength, but the other data-points we considered were relatively redeeming. In particular, its net debt to EBITDA was re-invigorating. We think that Tata Metaliks's debt does make it a bit risky, after considering the aforementioned data points together. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. Over time, share prices tend to follow earnings per share, so if you're interested in Tata Metaliks, you may well want to click here to check an interactive graph of its earnings per share history.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you’re looking to trade Tata Metaliks, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Tata Metaliks might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:TATAMETALI

Tata Metaliks

Tata Metaliks Limited engages in the manufacture and sale of pig iron and ductile iron pipes in India and internationally.

Flawless balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

FA

FAI on Arabian Internet and Communication Services ·

Solutions by stc: 34% Upside in Saudi's Digital Transformation Leader

Fair Value:ر.س342.2335.3% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

RO

RobertoAllende on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.9% undervalued

27 followersusers have followed this narrative

28 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Recently Updated Narratives

HA

Haha94 on Perdana Petroleum Berhad ·

Perdana Petroleum Berhad is a Zombie Business with a 27.34% Profit Margin and inflation adjusted revenue Business

Fair Value:RM 0.2128.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AB

Abc on Global X Etfs Icav - Global X Silver Miners Ucits ETF ·

Many trends acting at the same time

Fair Value:€10068.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NI

niteco on Texas Instruments ·

Engineered for Stability. Positioned for Growth.

Fair Value:US$314.4446.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

109 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.1% undervalued

941 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.4% undervalued

145 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative