Stock Analysis

Quess And Two More Stocks Estimated To Be Undervalued On The Indian Exchange

Reviewed by Simply Wall St

The Indian stock market has shown robust performance, with a 1.1% increase over the last week and an impressive 44% growth over the past 12 months. In this environment of strong earnings growth, projected at 16% per annum, identifying undervalued stocks like Quess can offer potential opportunities for investors looking for value in a thriving market.

Top 10 Undervalued Stocks Based On Cash Flows In India

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Updater Services (NSEI:UDS) | ₹298.25 | ₹539.77 | 44.7% |

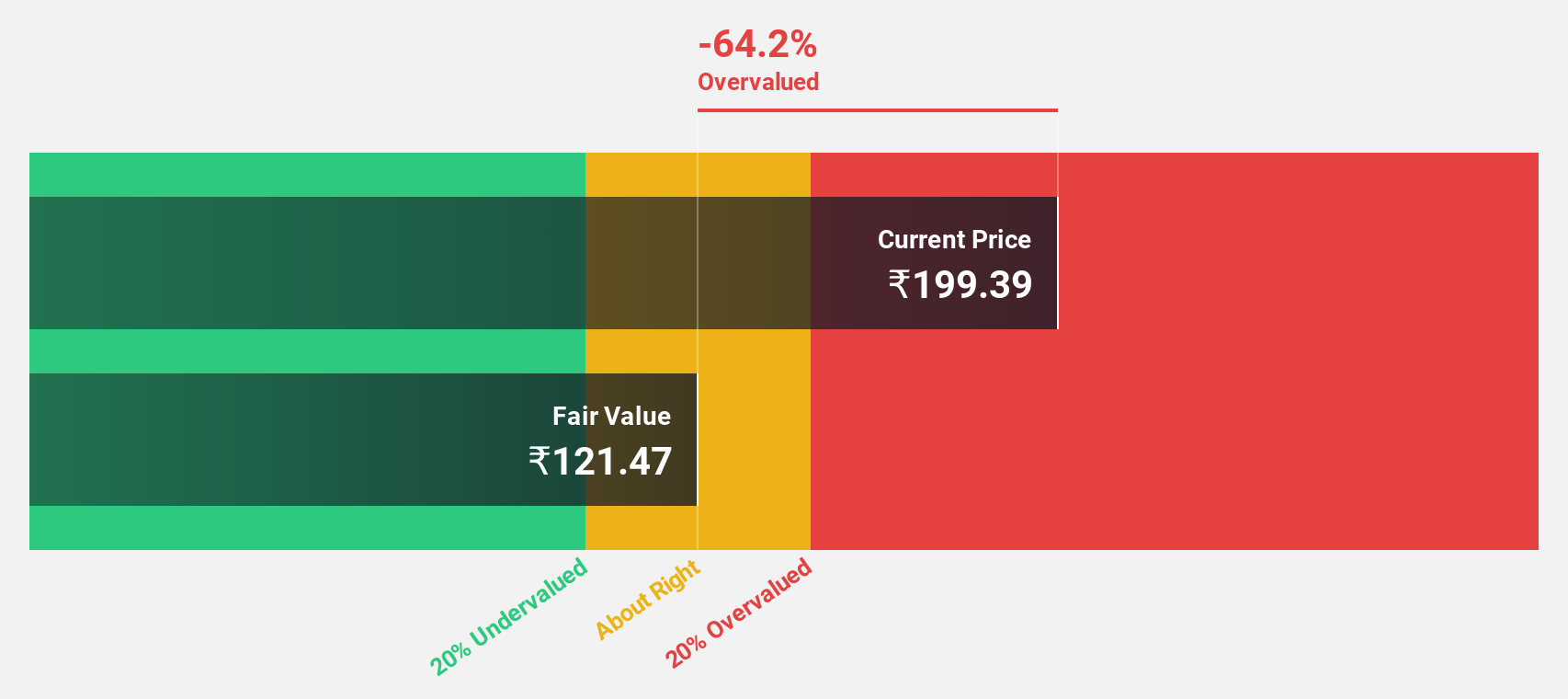

| IOL Chemicals and Pharmaceuticals (BSE:524164) | ₹409.30 | ₹636.71 | 35.7% |

| Rajesh Exports (NSEI:RAJESHEXPO) | ₹285.75 | ₹496.05 | 42.4% |

| Vedanta (NSEI:VEDL) | ₹465.00 | ₹735.75 | 36.8% |

| Strides Pharma Science (NSEI:STAR) | ₹943.80 | ₹1664.05 | 43.3% |

| Mahindra Logistics (NSEI:MAHLOG) | ₹537.90 | ₹904.58 | 40.5% |

| Delhivery (NSEI:DELHIVERY) | ₹399.85 | ₹740.91 | 46% |

| PVR INOX (NSEI:PVRINOX) | ₹1497.80 | ₹2565.55 | 41.6% |

| TV18 Broadcast (NSEI:TV18BRDCST) | ₹41.53 | ₹69.60 | 40.3% |

| Godrej Properties (NSEI:GODREJPROP) | ₹3161.65 | ₹5682.11 | 44.4% |

Below we spotlight a couple of our favorites from our exclusive screener

Quess (NSEI:QUESS)

Overview: Quess Corp Limited is a business services provider operating in India, South East Asia, the Middle East, and North America with a market capitalization of approximately ₹94.28 billion.

Operations: The revenue segments of the company are categorized into Workforce Management (₹134.42 billion), Operating Asset Management (₹28.01 billion), Global Technology Solutions excluding Product Led Business (₹23.40 billion), and Product Led Business (₹5.17 billion).

Estimated Discount To Fair Value: 14.4%

Quess Corp, priced at ₹634.85, trades below its estimated fair value of ₹742.06, reflecting a modest undervaluation based on cash flows. Despite this, the company's earnings have shown robust growth of 23.8% over the past year with expectations to outpace the Indian market significantly in coming years. However, concerns include an unstable dividend track record and significant insider selling recently. Recent financials confirm strong performance with substantial year-over-year increases in net income and revenue for Q4 2024 and full-year results.

- In light of our recent growth report, it seems possible that Quess' financial performance will exceed current levels.

- Click here and access our complete balance sheet health report to understand the dynamics of Quess.

Rajesh Exports (NSEI:RAJESHEXPO)

Overview: Rajesh Exports Limited operates in India as a gold refiner and engages in the manufacturing, wholesaling, and retailing of gold and diamond jewelry, along with various other gold products, boasting a market capitalization of approximately ₹84.37 billion.

Operations: The company's revenue from gold products totals approximately ₹280.92 billion.

Estimated Discount To Fair Value: 42.4%

Rajesh Exports, valued at ₹285.75, is perceived as undervalued with its price standing 42.4% below the estimated fair value of ₹496.05. The company's earnings are poised to grow by 31.68% annually, outstripping the Indian market's growth rate significantly. Despite this promising growth trajectory and favorable comparison to peers, its profit margins have dipped slightly from last year, and its return on equity in three years is expected to remain low at 8.2%. Upcoming board meetings will discuss financial results and dividend proposals for FY 2023-24.

- Insights from our recent growth report point to a promising forecast for Rajesh Exports' business outlook.

- Delve into the full analysis health report here for a deeper understanding of Rajesh Exports.

Shyam Metalics and Energy (NSEI:SHYAMMETL)

Overview: Shyam Metalics and Energy Limited is an integrated metal company based in India, specializing in the production and sale of long steel products and ferro alloys, with a market capitalization of approximately ₹199.08 billion.

Operations: The company generates ₹131.95 billion primarily from its iron and steel segment.

Estimated Discount To Fair Value: 29.2%

Shyam Metalics and Energy, priced at ₹715.1, trades 29.2% below its fair value of ₹1009.7, indicating significant undervaluation based on discounted cash flows. The company's earnings and revenue are expected to grow by 28.66% and 25.5% per year respectively, outpacing the Indian market projections significantly. Despite these growth prospects, shareholder dilution has occurred over the past year, and a low dividend coverage by cash flows suggests potential concerns about sustainable payouts. Recent expansions in rail infrastructure highlight operational enhancements supporting long-term growth.

- Our expertly prepared growth report on Shyam Metalics and Energy implies its future financial outlook may be stronger than recent results.

- Click to explore a detailed breakdown of our findings in Shyam Metalics and Energy's balance sheet health report.

Taking Advantage

- Dive into all 16 of the Undervalued Indian Stocks Based On Cash Flows we have identified here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're helping make it simple.

Find out whether Rajesh Exports is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:RAJESHEXPO

Rajesh Exports

A gold refiner, manufactures, wholesales, and retails gold and diamond jewelry, and various gold products in India.

Flawless balance sheet and undervalued.