Advertisement

- India

- /

- Metals and Mining

- /

- NSEI:SBCL

Shivalik Bimetal Controls' (NSE:SBCL) Shareholders Will Receive A Bigger Dividend Than Last Year

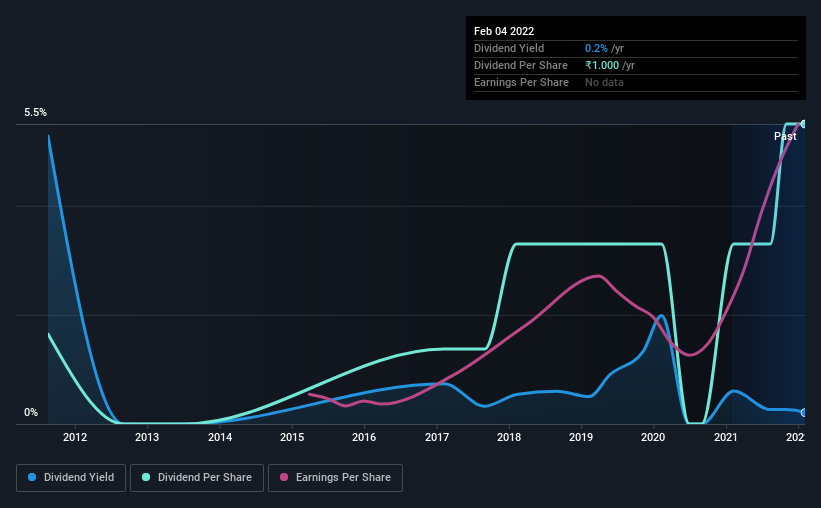

Shivalik Bimetal Controls Limited (NSE:SBCL) has announced that it will be increasing its dividend on the 3rd of March to ₹0.50. Even though the dividend went up, the yield is still quite low at only 0.2%.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that Shivalik Bimetal Controls' stock price has increased by 49% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

See our latest analysis for Shivalik Bimetal Controls

Shivalik Bimetal Controls' Dividend Is Well Covered By Earnings

Even a low dividend yield can be attractive if it is sustained for years on end. Shivalik Bimetal Controls is quite easily earning enough to cover the dividend, however it is being let down by weak cash flows. With the company not bringing in any cash, paying out to shareholders is bound to become difficult at some point.

Over the next year, EPS could expand by 43.5% if recent trends continue. Assuming the dividend continues along recent trends, we think the payout ratio could be 4.8% by next year, which is in a pretty sustainable range.

Dividend Volatility

The company's dividend history has been marked by instability, with at least 1 cut in the last 10 years. Since 2012, the dividend has gone from ₹0.30 to ₹1.00. This implies that the company grew its distributions at a yearly rate of about 13% over that duration. Shivalik Bimetal Controls has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

The Dividend Looks Likely To Grow

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Shivalik Bimetal Controls has impressed us by growing EPS at 43% per year over the past five years. Rapid earnings growth and a low payout ratio suggest this company has been effectively reinvesting in its business. Should that continue, this company could have a bright future.

In Summary

Overall, we always like to see the dividend being raised, but we don't think Shivalik Bimetal Controls will make a great income stock. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. We would be a touch cautious of relying on this stock primarily for the dividend income.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. However, there are other things to consider for investors when analysing stock performance. For instance, we've picked out 1 warning sign for Shivalik Bimetal Controls that investors should take into consideration. Looking for more high-yielding dividend ideas? Try our curated list of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SBCL

Shivalik Bimetal Controls

Operates as a process and product engineering company in India, the United States, Europe, and internationally.

Flawless balance sheet with high growth potential.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|12.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|21.7% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.1% undervalued

EA

Community Contributor