Advertisement

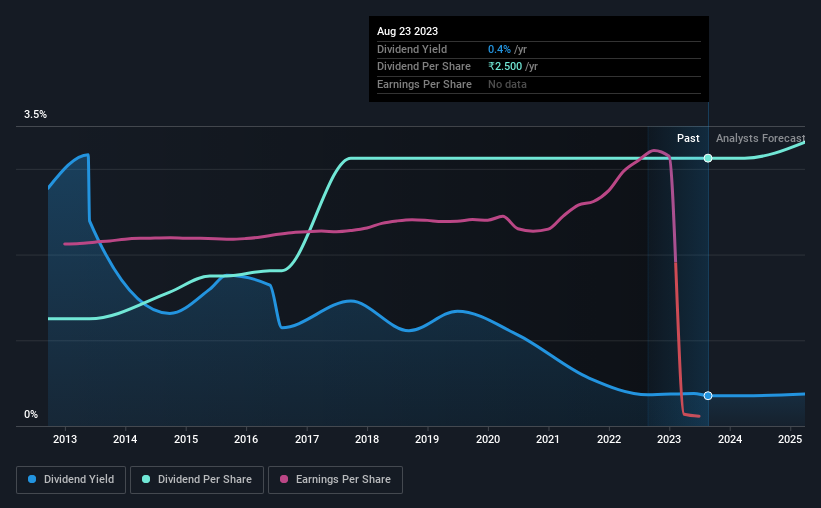

RHI Magnesita India Limited's (NSE:RHIM) investors are due to receive a payment of ₹2.50 per share on 28th of October. This payment means the dividend yield will be 0.4%, which is below the average for the industry.

See our latest analysis for RHI Magnesita India

RHI Magnesita India's Payment Has Solid Earnings Coverage

It would be nice for the yield to be higher, but we should also check if higher levels of dividend payment would be sustainable. RHI Magnesita India is not generating a profit, but its free cash flows easily cover the dividend, leaving plenty for reinvestment in the business. This gives us some comfort about the level of the dividend payments.

The next year is set to see EPS grow by 124.5%. Assuming the dividend continues along recent trends, we think the payout ratio could be 46% by next year, which is in a pretty sustainable range.

RHI Magnesita India Has A Solid Track Record

The company has an extended history of paying stable dividends. Since 2013, the annual payment back then was ₹1.00, compared to the most recent full-year payment of ₹2.50. This implies that the company grew its distributions at a yearly rate of about 9.6% over that duration. The growth of the dividend has been pretty reliable, so we think this can offer investors some nice additional income in their portfolio.

The Dividend Has Limited Growth Potential

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. However, things aren't all that rosy. Over the past five years, it looks as though RHI Magnesita India's EPS has declined at around 15% a year. Dividend payments are likely to come under some pressure unless EPS can pull out of the nosedive it is in. However, the next year is actually looking up, with earnings set to rise. We would just wait until it becomes a pattern before getting too excited.

An additional note is that the company has been raising capital by issuing stock equal to 28% of shares outstanding in the last 12 months. Regularly doing this can be detrimental - it's hard to grow dividends per share when new shares are regularly being created.

In Summary

Overall, it's nice to see a consistent dividend payment, but we think that longer term, the current level of payment might be unsustainable. The company has been bring in plenty of cash to cover the dividend, but we don't necessarily think that makes it a great dividend stock. We don't think RHI Magnesita India is a great stock to add to your portfolio if income is your focus.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Case in point: We've spotted 3 warning signs for RHI Magnesita India (of which 1 is potentially serious!) you should know about. Is RHI Magnesita India not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:RHIM

RHI Magnesita India

Engages in the manufacture and trading of refractories, monolithics, bricks, and ceramic paper in India and internationally.

Excellent balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.1% undervalued

TI

Community Contributor