Advertisement

- India

- /

- Metals and Mining

- /

- NSEI:POCL

Pondy Oxides And Chemicals (NSE:POCL) Has A Pretty Healthy Balance Sheet

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Pondy Oxides And Chemicals Limited (NSE:POCL) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

What Is Pondy Oxides And Chemicals's Debt?

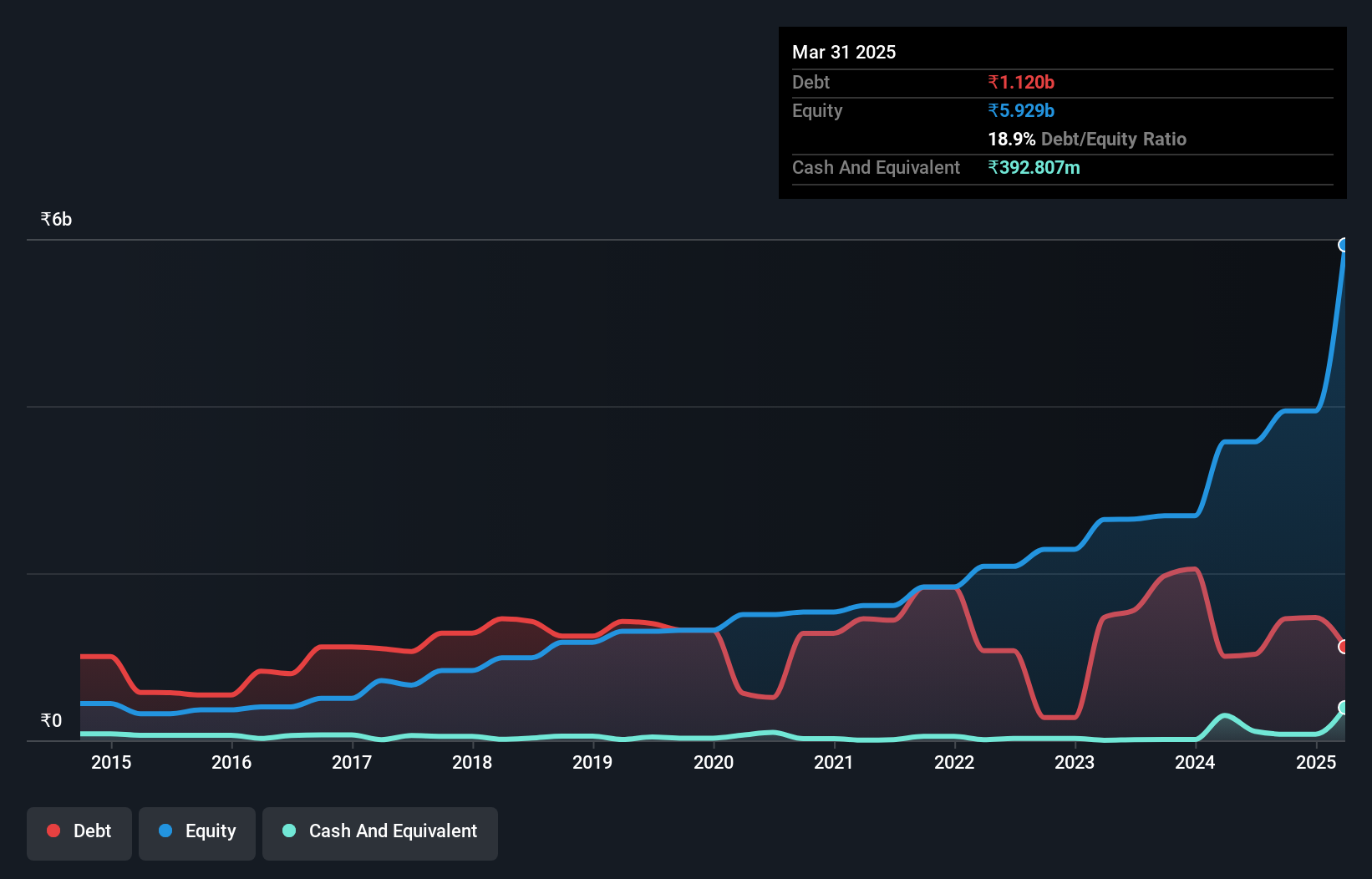

As you can see below, at the end of March 2025, Pondy Oxides And Chemicals had ₹1.12b of debt, up from ₹1.03b a year ago. Click the image for more detail. However, it also had ₹392.8m in cash, and so its net debt is ₹726.9m.

A Look At Pondy Oxides And Chemicals' Liabilities

According to the last reported balance sheet, Pondy Oxides And Chemicals had liabilities of ₹1.41b due within 12 months, and liabilities of ₹40.6m due beyond 12 months. Offsetting this, it had ₹392.8m in cash and ₹1.29b in receivables that were due within 12 months. So it can boast ₹241.4m more liquid assets than total liabilities.

This state of affairs indicates that Pondy Oxides And Chemicals' balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the ₹30.9b company is short on cash, but still worth keeping an eye on the balance sheet.

See our latest analysis for Pondy Oxides And Chemicals

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With net debt sitting at just 0.59 times EBITDA, Pondy Oxides And Chemicals is arguably pretty conservatively geared. And it boasts interest cover of 8.1 times, which is more than adequate. On top of that, Pondy Oxides And Chemicals grew its EBIT by 57% over the last twelve months, and that growth will make it easier to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is Pondy Oxides And Chemicals's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Pondy Oxides And Chemicals burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

The good news is that Pondy Oxides And Chemicals's demonstrated ability to grow its EBIT delights us like a fluffy puppy does a toddler. But we must concede we find its conversion of EBIT to free cash flow has the opposite effect. All these things considered, it appears that Pondy Oxides And Chemicals can comfortably handle its current debt levels. On the plus side, this leverage can boost shareholder returns, but the potential downside is more risk of loss, so it's worth monitoring the balance sheet. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 3 warning signs for Pondy Oxides And Chemicals you should be aware of, and 1 of them can't be ignored.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:POCL

Pondy Oxides And Chemicals

A secondary lead manufacturer company, produces and sells lead, lead alloys, and plastic additives in India.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$268.43|27.9% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|43.8% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|41.0% undervalued

AG

Community Contributor