Advertisement

- India

- /

- Metals and Mining

- /

- NSEI:NSLNISP

NMDC Steel (NSE:NSLNISP) Has Debt But No Earnings; Should You Worry?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that NMDC Steel Limited (NSE:NSLNISP) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

What Is NMDC Steel's Debt?

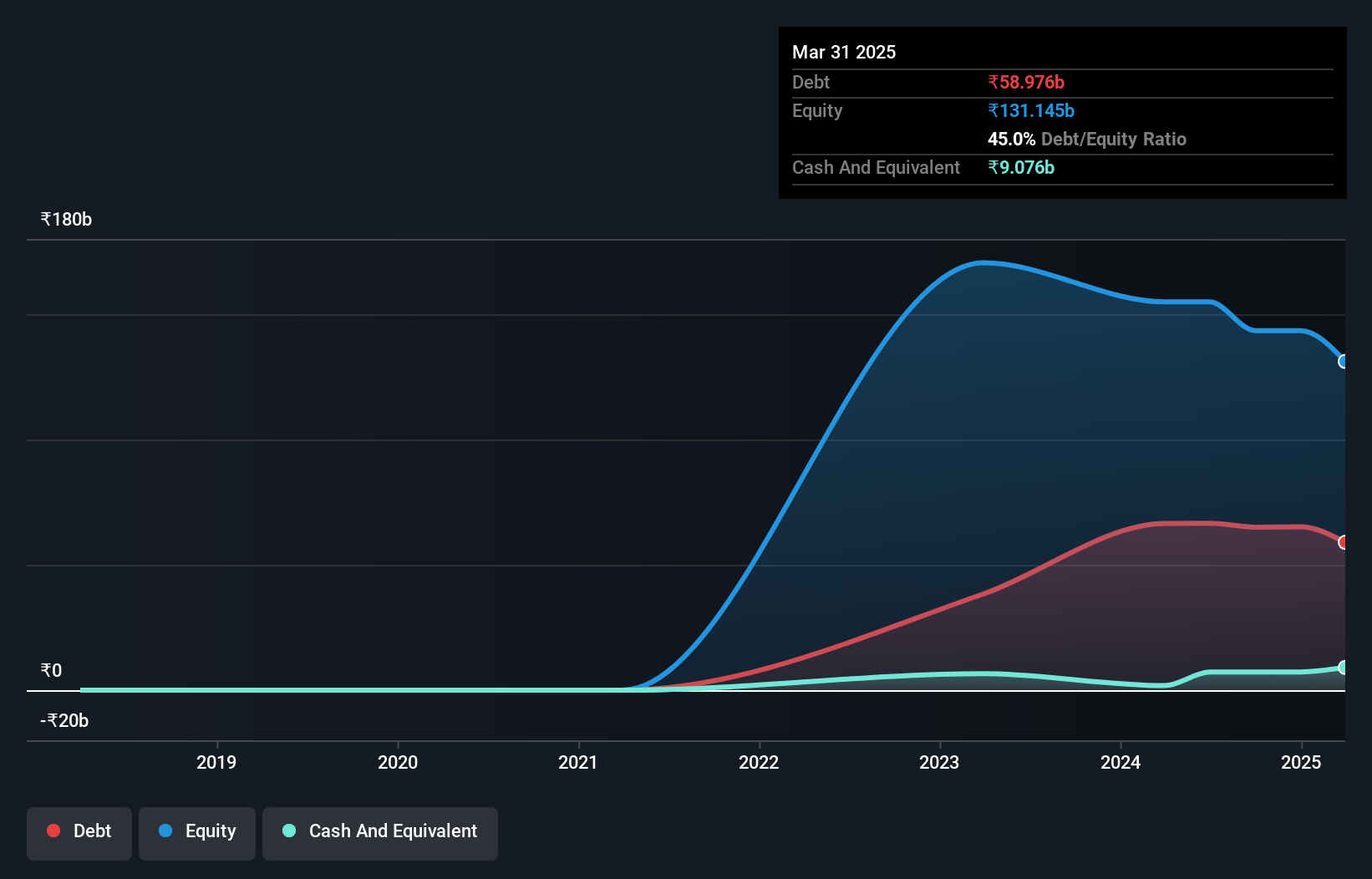

You can click the graphic below for the historical numbers, but it shows that NMDC Steel had ₹59.0b of debt in March 2025, down from ₹66.5b, one year before. However, it also had ₹9.08b in cash, and so its net debt is ₹49.9b.

How Healthy Is NMDC Steel's Balance Sheet?

According to the last reported balance sheet, NMDC Steel had liabilities of ₹99.0b due within 12 months, and liabilities of ₹54.5b due beyond 12 months. Offsetting these obligations, it had cash of ₹9.08b as well as receivables valued at ₹1.97b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₹142.5b.

Given this deficit is actually higher than the company's market capitalization of ₹110.4b, we think shareholders really should watch NMDC Steel's debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since NMDC Steel will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Check out our latest analysis for NMDC Steel

In the last year NMDC Steel wasn't profitable at an EBIT level, but managed to grow its revenue by 179%, to ₹85b. So its pretty obvious shareholders are hoping for more growth!

Caveat Emptor

While we can certainly appreciate NMDC Steel's revenue growth, its earnings before interest and tax (EBIT) loss is not ideal. Indeed, it lost a very considerable ₹27b at the EBIT level. Considering that alongside the liabilities mentioned above make us nervous about the company. It would need to improve its operations quickly for us to be interested in it. It's fair to say the loss of ₹24b didn't encourage us either; we'd like to see a profit. And until that time we think this is a risky stock. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example - NMDC Steel has 1 warning sign we think you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if NMDC Steel might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:NSLNISP

Good value with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor