Advertisement

N R Agarwal Industries (NSE:NRAIL) Hasn't Managed To Accelerate Its Returns

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. That's why when we briefly looked at N R Agarwal Industries' (NSE:NRAIL) ROCE trend, we were pretty happy with what we saw.

Understanding Return On Capital Employed (ROCE)

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on N R Agarwal Industries is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

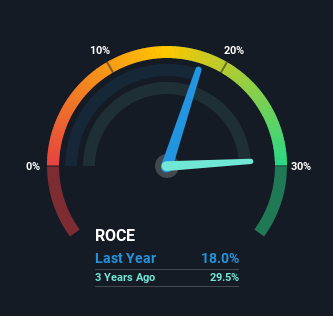

0.18 = ₹1.1b ÷ (₹9.3b - ₹3.0b) (Based on the trailing twelve months to June 2021).

Therefore, N R Agarwal Industries has an ROCE of 18%. On its own, that's a standard return, however it's much better than the 11% generated by the Packaging industry.

See our latest analysis for N R Agarwal Industries

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating N R Agarwal Industries' past further, check out this free graph of past earnings, revenue and cash flow.

So How Is N R Agarwal Industries' ROCE Trending?

While the current returns on capital are decent, they haven't changed much. The company has employed 46% more capital in the last five years, and the returns on that capital have remained stable at 18%. 18% is a pretty standard return, and it provides some comfort knowing that N R Agarwal Industries has consistently earned this amount. Stable returns in this ballpark can be unexciting, but if they can be maintained over the long run, they often provide nice rewards to shareholders.

The Bottom Line On N R Agarwal Industries' ROCE

In the end, N R Agarwal Industries has proven its ability to adequately reinvest capital at good rates of return. However, despite the favorable fundamentals, the stock has fallen 31% over the last three years, so there might be an opportunity here for astute investors. For that reason, savvy investors might want to look further into this company in case it's a prime investment.

If you'd like to know about the risks facing N R Agarwal Industries, we've discovered 3 warning signs that you should be aware of.

While N R Agarwal Industries may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

If you decide to trade N R Agarwal Industries, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if N R Agarwal Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:NRAIL

N R Agarwal Industries

Manufactures and sells finished paper products in India.

Medium-low risk second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor