Advertisement

We Think NACL Industries Limited's (NSE:NACLIND) CEO Compensation Package Needs To Be Put Under A Microscope

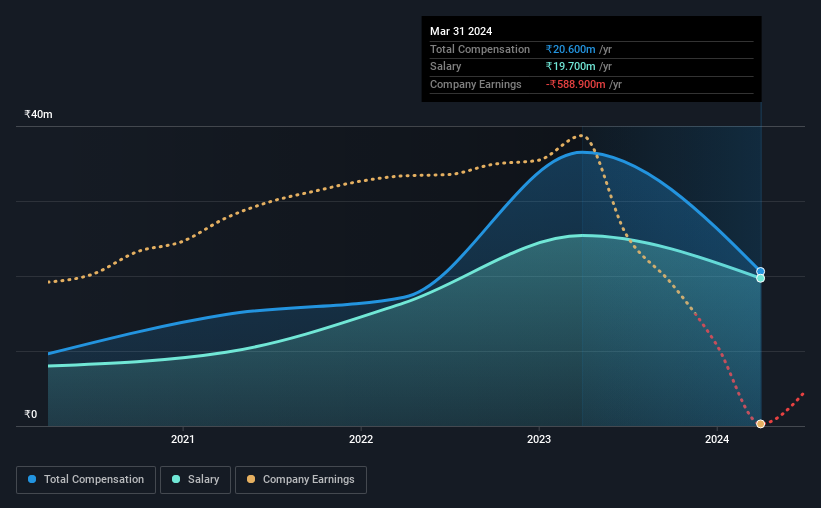

Key Insights

- NACL Industries' Annual General Meeting to take place on 25th of September

- CEO Pavan Munjuluri's total compensation includes salary of ₹19.7m

- The total compensation is 272% higher than the average for the industry

- NACL Industries' EPS declined by 67% over the past three years while total shareholder loss over the past three years was 25%

The results at NACL Industries Limited (NSE:NACLIND) have been quite disappointing recently and CEO Pavan Munjuluri bears some responsibility for this. Shareholders will be interested in what the board will have to say about turning performance around at the next AGM on 25th of September. This will be also be a chance where they can challenge the board on company direction and vote on resolutions such as executive remuneration. The data we present below explains why we think CEO compensation is not consistent with recent performance.

View our latest analysis for NACL Industries

Comparing NACL Industries Limited's CEO Compensation With The Industry

Our data indicates that NACL Industries Limited has a market capitalization of ₹11b, and total annual CEO compensation was reported as ₹21m for the year to March 2024. Notably, that's a decrease of 44% over the year before. Notably, the salary which is ₹19.7m, represents most of the total compensation being paid.

On comparing similar-sized companies in the Indian Chemicals industry with market capitalizations below ₹17b, we found that the median total CEO compensation was ₹5.5m. Hence, we can conclude that Pavan Munjuluri is remunerated higher than the industry median.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | ₹20m | ₹25m | 96% |

| Other | ₹900k | ₹11m | 4% |

| Total Compensation | ₹21m | ₹37m | 100% |

On an industry level, around 89% of total compensation represents salary and 11% is other remuneration. Investors will find it interesting that NACL Industries pays the bulk of its rewards through a traditional salary, instead of non-salary benefits. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

NACL Industries Limited's Growth

NACL Industries Limited has reduced its earnings per share by 67% a year over the last three years. In the last year, its revenue is down 14%.

Few shareholders would be pleased to read that EPS have declined. This is compounded by the fact revenue is actually down on last year. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has NACL Industries Limited Been A Good Investment?

With a three year total loss of 25% for the shareholders, NACL Industries Limited would certainly have some dissatisfied shareholders. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

Pavan receives almost all of their compensation through a salary. Not only have shareholders not seen a favorable return on their investment, but the business hasn't performed well either. Few shareholders would be willing to award the CEO with a pay raise. At the upcoming AGM, management will get a chance to explain how they plan to get the business back on track and address the concerns from investors.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We did our research and spotted 2 warning signs for NACL Industries that investors should look into moving forward.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Valuation is complex, but we're here to simplify it.

Discover if NACL Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:NACLIND

Low risk with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor