- India

- /

- Basic Materials

- /

- NSEI:KCP

Shareholders Will Most Likely Find The KCP Limited's (NSE:KCP) CEO Compensation Acceptable

Key Insights

- KCP's Annual General Meeting to take place on 22nd of August

- Total pay for CEO Velagapudi Lakshmana Dutt includes ₹21.8m salary

- The total compensation is similar to the average for the industry

- KCP's total shareholder return over the past three years was 49% while its EPS was down 3.4% over the past three years

The KCP Limited (NSE:KCP) has exhibited strong share price growth in the past few years. However, its earnings growth has not kept up, suggesting that there may be something amiss. Some of these issues will occupy shareholders' minds as the AGM rolls around on 22nd of August. One way that shareholders can influence managerial decisions is through voting on CEO and executive remuneration packages, which studies show could impact company performance. From the data that we gathered, we think that shareholders should hold off on a raise on CEO compensation until performance starts to show some improvement.

See our latest analysis for KCP

How Does Total Compensation For Velagapudi Lakshmana Dutt Compare With Other Companies In The Industry?

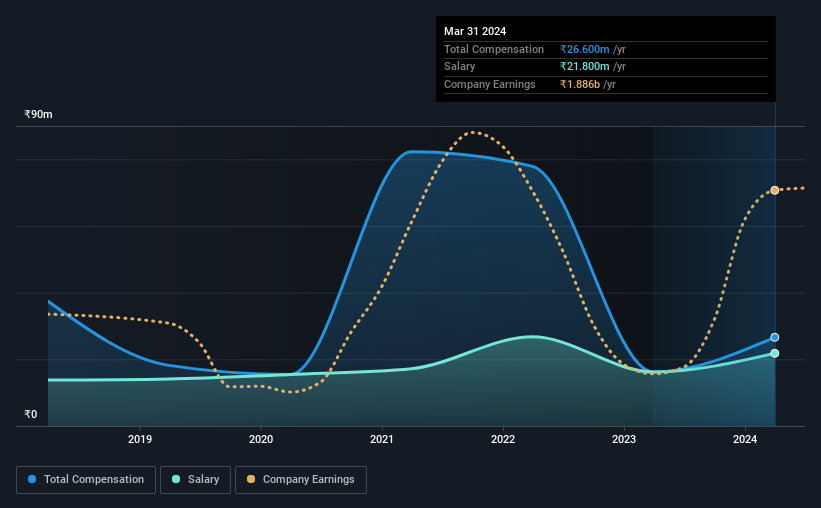

According to our data, The KCP Limited has a market capitalization of ₹27b, and paid its CEO total annual compensation worth ₹27m over the year to March 2024. Notably, that's an increase of 64% over the year before. We note that the salary portion, which stands at ₹21.8m constitutes the majority of total compensation received by the CEO.

For comparison, other companies in the Indian Basic Materials industry with market capitalizations ranging between ₹17b and ₹67b had a median total CEO compensation of ₹37m. So it looks like KCP compensates Velagapudi Lakshmana Dutt in line with the median for the industry. Moreover, Velagapudi Lakshmana Dutt also holds ₹2.5b worth of KCP stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | ₹22m | ₹16m | 82% |

| Other | ₹4.8m | - | 18% |

| Total Compensation | ₹27m | ₹16m | 100% |

Speaking on an industry level, nearly 83% of total compensation represents salary, while the remainder of 17% is other remuneration. There isn't a significant difference between KCP and the broader market, in terms of salary allocation in the overall compensation package. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

The KCP Limited's Growth

Over the last three years, The KCP Limited has shrunk its earnings per share by 3.4% per year. Its revenue is up 15% over the last year.

Few shareholders would be pleased to read that EPS have declined. And while it's good to see some good revenue growth recently, the growth isn't really fast enough for us to put aside my concerns around EPS. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has The KCP Limited Been A Good Investment?

Boasting a total shareholder return of 49% over three years, The KCP Limited has done well by shareholders. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

While the return to shareholders does look promising, it's hard to ignore the lack of earnings growth and this makes us question whether these strong returns will continue. The upcoming AGM will provide shareholders the opportunity to revisit the company’s remuneration policies and evaluate if the board’s judgement and decision-making is aligned with that of the company’s shareholders.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. That's why we did our research, and identified 3 warning signs for KCP (of which 1 makes us a bit uncomfortable!) that you should know about in order to have a holistic understanding of the stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if KCP might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:KCP

KCP

Engages in cement, heavy engineering, power generation, and hospitality businesses in India.

Excellent balance sheet and slightly overvalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Automotive Electronics Manufacturer Consistent and Stable

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion