Advertisement

Most Shareholders Will Probably Find That The CEO Compensation For Kansai Nerolac Paints Limited (NSE:KANSAINER) Is Reasonable

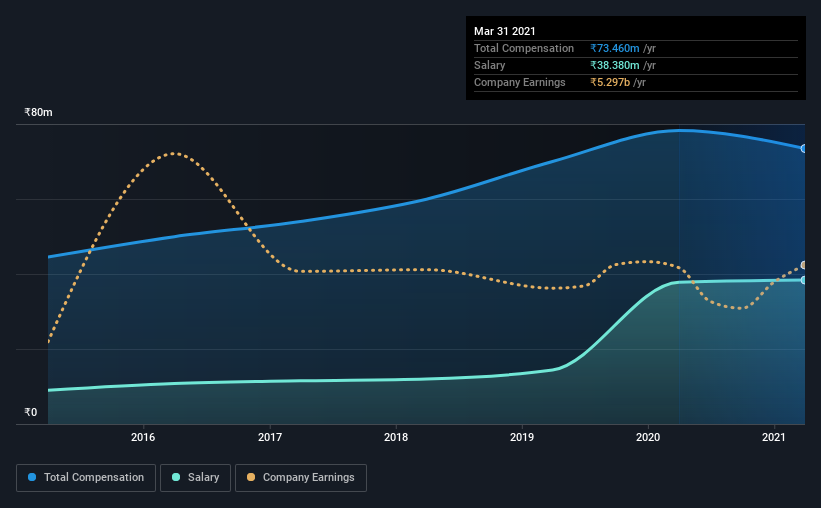

CEO Harishchandra Meghraj Bharuka has done a decent job of delivering relatively good performance at Kansai Nerolac Paints Limited (NSE:KANSAINER) recently. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 25 June 2021. Here is our take on why we think the CEO compensation looks appropriate.

See our latest analysis for Kansai Nerolac Paints

How Does Total Compensation For Harishchandra Meghraj Bharuka Compare With Other Companies In The Industry?

According to our data, Kansai Nerolac Paints Limited has a market capitalization of ₹311b, and paid its CEO total annual compensation worth ₹73m over the year to March 2021. We note that's a small decrease of 6.1% on last year. In particular, the salary of ₹38.4m, makes up a fairly large portion of the total compensation being paid to the CEO.

For comparison, other companies in the same industry with market capitalizations ranging between ₹147b and ₹470b had a median total CEO compensation of ₹65m. So it looks like Kansai Nerolac Paints compensates Harishchandra Meghraj Bharuka in line with the median for the industry.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | ₹38m | ₹38m | 52% |

| Other | ₹35m | ₹40m | 48% |

| Total Compensation | ₹73m | ₹78m | 100% |

On an industry level, around 89% of total compensation represents salary and 11% is other remuneration. It's interesting to note that Kansai Nerolac Paints allocates a smaller portion of compensation to salary in comparison to the broader industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Kansai Nerolac Paints Limited's Growth Numbers

Earnings per share at Kansai Nerolac Paints Limited are much the same as they were three years ago, albeit with slightly higher. Its revenue is down 3.9% over the previous year.

We would argue that the lack of revenue growth in the last year is less than ideal, but the modest EPS growth gives us some relief. It's hard to reach a conclusion about business performance right now. This may be one to watch. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Kansai Nerolac Paints Limited Been A Good Investment?

With a total shareholder return of 25% over three years, Kansai Nerolac Paints Limited shareholders would, in general, be reasonably content. But they would probably prefer not to see CEO compensation far in excess of the median.

In Summary...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. In saying that, any proposed increase to CEO compensation will still be assessed on how reasonable it is based on performance and industry benchmarks.

CEO compensation can have a massive impact on performance, but it's just one element. We did our research and spotted 1 warning sign for Kansai Nerolac Paints that investors should look into moving forward.

Important note: Kansai Nerolac Paints is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

If you’re looking to trade Kansai Nerolac Paints, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Kansai Nerolac Paints might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:KANSAINER

Kansai Nerolac Paints

Manufactures and supplies paints and varnishes, enamels, and lacquers in India.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|29.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.8% undervalued

AG

Community Contributor