Advertisement

Jocil (NSE:JOCIL) Will Pay A Smaller Dividend Than Last Year

Jocil Limited (NSE:JOCIL) has announced it will be reducing its dividend payable on the 24th of October to ₹0.50, which is 67% lower than what investors received last year for the same period. This means that the annual payment will be 0.9% of the current stock price, which is in line with the average for the industry.

Jocil's Payment Could Potentially Have Solid Earnings Coverage

Unless the payments are sustainable, the dividend yield doesn't mean too much. The last dividend made up quite a large portion of free cash flows, and this was made worse by the lack of free cash flows. Generally, we think that this would be a risky long term practice.

Looking forward, EPS could fall by 29.0% if the company can't turn things around from the last few years. If the dividend continues along recent trends, we estimate the payout ratio could be 9.2%, which we consider to be quite comfortable, even though the current levels are slightly more elevated.

See our latest analysis for Jocil

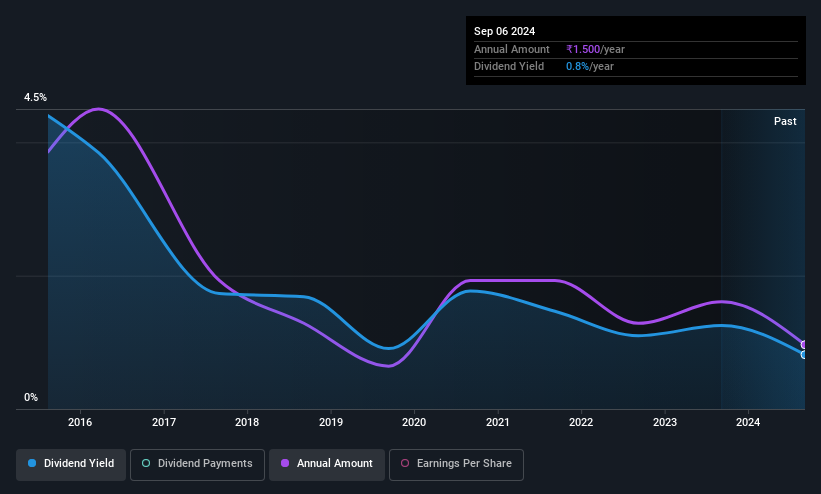

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. The dividend has gone from an annual total of ₹5.00 in 2015 to the most recent total annual payment of ₹1.50. Dividend payments have fallen sharply, down 70% over that time. Declining dividends isn't generally what we look for as they can indicate that the company is running into some challenges.

The Dividend Has Limited Growth Potential

With a relatively unstable dividend, and a poor history of shrinking dividends, it's even more important to see if EPS is growing. Over the past five years, it looks as though Jocil's EPS has declined at around 29% a year. Dividend payments are likely to come under some pressure unless EPS can pull out of the nosedive it is in.

The Dividend Could Prove To Be Unreliable

Overall, the dividend looks like it may have been a bit high, which explains why it has now been cut. The payments are bit high to be considered sustainable, and the track record isn't the best. Overall, we don't think this company has the makings of a good income stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. For example, we've identified 4 warning signs for Jocil (1 is significant!) that you should be aware of before investing. Is Jocil not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:JOCIL

Jocil

Manufactures and sells stearic acids, fatty acids, soap noodles, toilet soaps, glycerine, and industrial oxygen in India.

Excellent balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor