Advertisement

- India

- /

- Basic Materials

- /

- NSEI:JKCEMENT

J.K. Cement Limited (NSE:JKCEMENT) First-Quarter Results Just Came Out: Here's What Analysts Are Forecasting For This Year

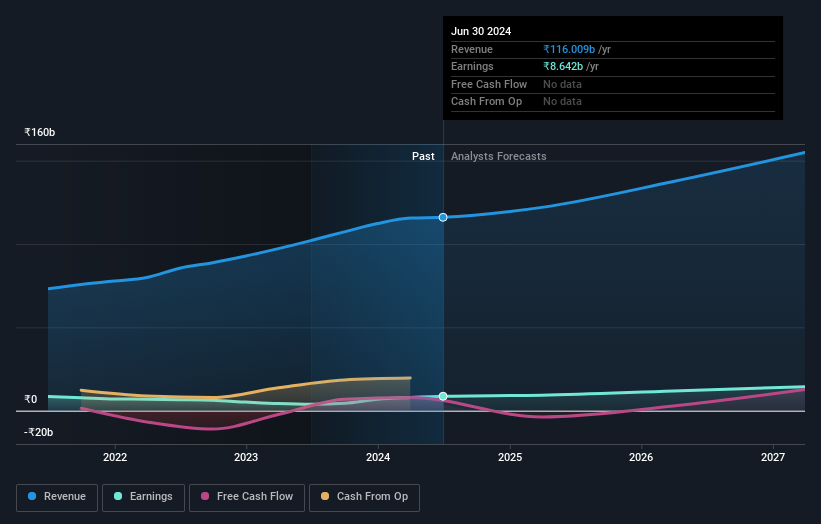

J.K. Cement Limited (NSE:JKCEMENT) defied analyst predictions to release its quarterly results, which were ahead of market expectations. Results were good overall, with revenues beating analyst predictions by 2.5% to hit ₹28b. Statutory earnings per share (EPS) came in at ₹23.98, some 2.6% above whatthe analysts had expected. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

See our latest analysis for J.K. Cement

Taking into account the latest results, the current consensus from J.K. Cement's 21 analysts is for revenues of ₹122.0b in 2025. This would reflect a reasonable 5.1% increase on its revenue over the past 12 months. Per-share earnings are expected to increase 7.3% to ₹120. Yet prior to the latest earnings, the analysts had been anticipated revenues of ₹124.8b and earnings per share (EPS) of ₹127 in 2025. It's pretty clear that pessimism has reared its head after the latest results, leading to a weaker revenue outlook and a small dip in earnings per share estimates.

Despite the cuts to forecast earnings, there was no real change to the ₹4,663 price target, showing that the analysts don't think the changes have a meaningful impact on its intrinsic value. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on J.K. Cement, with the most bullish analyst valuing it at ₹5,704 and the most bearish at ₹2,702 per share. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's pretty clear that there is an expectation that J.K. Cement's revenue growth will slow down substantially, with revenues to the end of 2025 expected to display 6.9% growth on an annualised basis. This is compared to a historical growth rate of 17% over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue shrink 6.4% per year. So it's clear that despite the slowdown in growth, J.K. Cement is still expected to grow meaningfully faster than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for J.K. Cement. Sadly they also cut their revenue estimates, although at least the company is expected to perform a bit better than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have forecasts for J.K. Cement going out to 2027, and you can see them free on our platform here.

We don't want to rain on the parade too much, but we did also find 2 warning signs for J.K. Cement that you need to be mindful of.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:JKCEMENT

J.K. Cement

Manufactures and sells cement and its related products in India and internationally.

Solid track record with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor