Advertisement

- India

- /

- Metals and Mining

- /

- NSEI:DPWIRES

Are D.P. Wires Limited's (NSE:DPWIRES) Fundamentals Good Enough to Warrant Buying Given The Stock's Recent Weakness?

With its stock down 32% over the past three months, it is easy to disregard D.P. Wires (NSE:DPWIRES). However, stock prices are usually driven by a company’s financials over the long term, which in this case look pretty respectable. Particularly, we will be paying attention to D.P. Wires' ROE today.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. Put another way, it reveals the company's success at turning shareholder investments into profits.

View our latest analysis for D.P. Wires

How To Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for D.P. Wires is:

12% = ₹294m ÷ ₹2.4b (Based on the trailing twelve months to September 2024).

The 'return' refers to a company's earnings over the last year. That means that for every ₹1 worth of shareholders' equity, the company generated ₹0.12 in profit.

What Has ROE Got To Do With Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

A Side By Side comparison of D.P. Wires' Earnings Growth And 12% ROE

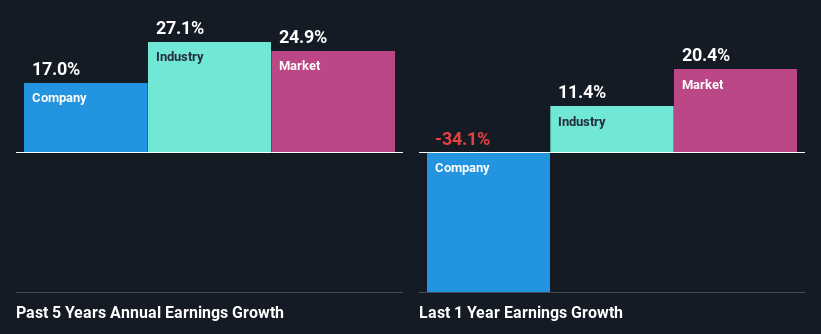

At first glance, D.P. Wires' ROE doesn't look very promising. However, given that the company's ROE is similar to the average industry ROE of 11%, we may spare it some thought. On the other hand, D.P. Wires reported a moderate 17% net income growth over the past five years. Considering the moderately low ROE, it is quite possible that there might be some other aspects that are positively influencing the company's earnings growth. Such as - high earnings retention or an efficient management in place.

As a next step, we compared D.P. Wires' net income growth with the industry and were disappointed to see that the company's growth is lower than the industry average growth of 27% in the same period.

Earnings growth is an important metric to consider when valuing a stock. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if D.P. Wires is trading on a high P/E or a low P/E, relative to its industry.

Is D.P. Wires Using Its Retained Earnings Effectively?

D.P. Wires' three-year median payout ratio to shareholders is 4.3% (implying that it retains 96% of its income), which is on the lower side, so it seems like the management is reinvesting profits heavily to grow its business.

Along with seeing a growth in earnings, D.P. Wires only recently started paying dividends. Its quite possible that the company was looking to impress its shareholders.

Conclusion

Overall, we feel that D.P. Wires certainly does have some positive factors to consider. Namely, its respectable earnings growth, which it achieved due to it retaining most of its profits. However, given the low ROE, investors may not be benefitting from all that reinvestment after all. While we won't completely dismiss the company, what we would do, is try to ascertain how risky the business is to make a more informed decision around the company. You can see the 1 risk we have identified for D.P. Wires by visiting our risks dashboard for free on our platform here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:DPWIRES

D.P. Wires

Manufactures and supplies steel wires, plastic pipes, and plastic films for oil and gas, power, environment, civil, energy, automobile, infrastructure, and other industries in India and internationally.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|6.3% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.8% undervalued

GM

Community Contributor