Advertisement

Balaji Amines Limited Just Missed Earnings And Its Revenue Numbers Were Weaker Than Expected

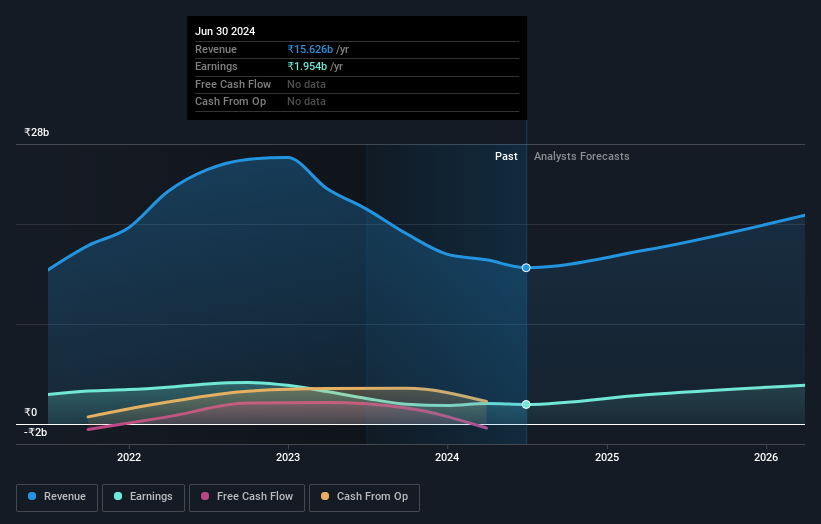

Shareholders might have noticed that Balaji Amines Limited (NSE:BALAMINES) filed its quarterly result this time last week. The early response was not positive, with shares down 8.9% to ₹2,222 in the past week. Balaji Amines reported a serious miss, with revenue of ₹3.8b falling a huge 33% short of analyst estimates. The bright side is that statutory earnings per share of ₹63.22 were in line with forecasts. Following the result, the analyst has updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We've gathered the most recent statutory forecasts to see whether the analyst has changed their earnings models, following these results.

View our latest analysis for Balaji Amines

Taking into account the latest results, the most recent consensus for Balaji Amines from single analyst is for revenues of ₹17.4b in 2025. If met, it would imply a solid 11% increase on its revenue over the past 12 months. Statutory earnings per share are predicted to jump 50% to ₹90.30. In the lead-up to this report, the analyst had been modelling revenues of ₹20.4b and earnings per share (EPS) of ₹95.40 in 2025. It looks like sentiment has fallen somewhat in the aftermath of these results, with a substantial drop in revenue estimates and a small dip in earnings per share numbers as well.

The analyst made no major changes to their price target of ₹2,611, suggesting the downgrades are not expected to have a long-term impact on Balaji Amines' valuation.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. We can infer from the latest estimates that forecasts expect a continuation of Balaji Amines'historical trends, as the 15% annualised revenue growth to the end of 2025 is roughly in line with the 16% annual growth over the past five years. Compare this with the broader industry, which analyst estimates (in aggregate) suggest will see revenues grow 12% annually. So although Balaji Amines is expected to maintain its revenue growth rate, it's definitely expected to grow faster than the wider industry.

The Bottom Line

The biggest concern is that the analyst reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Balaji Amines. They also downgraded Balaji Amines' revenue estimates, but industry data suggests that it is expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that in mind, we wouldn't be too quick to come to a conclusion on Balaji Amines. Long-term earnings power is much more important than next year's profits. We have analyst estimates for Balaji Amines going out as far as 2026, and you can see them free on our platform here.

Before you take the next step you should know about the 1 warning sign for Balaji Amines that we have uncovered.

Valuation is complex, but we're here to simplify it.

Discover if Balaji Amines might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:BALAMINES

Balaji Amines

Engages in the manufacture and sale of methylamines, ethylamines, and derivatives of specialty chemicals and pharma excipients in India.

Flawless balance sheet with high growth potential and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor