- India

- /

- Professional Services

- /

- NSEI:QUESS

Indian Exchange Growth Companies With High Insider Ownership And 16% Revenue Growth

Reviewed by Simply Wall St

In recent times, the Indian market has shown robust performance, with a 1.5% increase over the last week and an impressive 46% rise over the past year. Coupled with an expected annual earnings growth of 16%, stocks like those of growth companies with high insider ownership become particularly attractive as they often signal strong confidence from those who know the company best.

Top 10 Growth Companies With High Insider Ownership In India

| Name | Insider Ownership | Earnings Growth |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 28.9% |

| Kirloskar Pneumatic (BSE:505283) | 30.6% | 29.8% |

| Pitti Engineering (BSE:513519) | 33.6% | 28.0% |

| Shivalik Bimetal Controls (BSE:513097) | 19.5% | 28.7% |

| Jupiter Wagons (NSEI:JWL) | 11.1% | 27.2% |

| Rajratan Global Wire (BSE:517522) | 19.8% | 33.5% |

| Dixon Technologies (India) (NSEI:DIXON) | 24.9% | 34.1% |

| Paisalo Digital (BSE:532900) | 16.3% | 23.8% |

| JNK India (NSEI:JNKINDIA) | 23.8% | 31.8% |

| Apollo Hospitals Enterprise (NSEI:APOLLOHOSP) | 10.4% | 33.2% |

Let's dive into some prime choices out of from the screener.

Honasa Consumer (NSEI:HONASA)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Honasa Consumer Limited is a digital-first beauty and personal care company based in India, with a market capitalization of approximately ₹147.76 billion.

Operations: The company generates ₹19.20 billion in revenue from trading a variety of beauty and personal care products and related services.

Insider Ownership: 36.6%

Revenue Growth Forecast: 16.3% p.a.

Honasa Consumer, recently profitable, is experiencing robust growth with earnings expected to increase significantly at 34.4% per year, outpacing the Indian market's average. Revenue forecasts also look promising, growing at 16.3% annually against a market rate of 9.7%. However, its Return on Equity is projected to be modest at 19.7%. The company expanded its retail footprint through a significant partnership with Reliance Retail Ventures Ltd., enhancing offline presence for its Mamaearth brand across over 1000 stores nationwide.

- Click here and access our complete growth analysis report to understand the dynamics of Honasa Consumer.

- Insights from our recent valuation report point to the potential overvaluation of Honasa Consumer shares in the market.

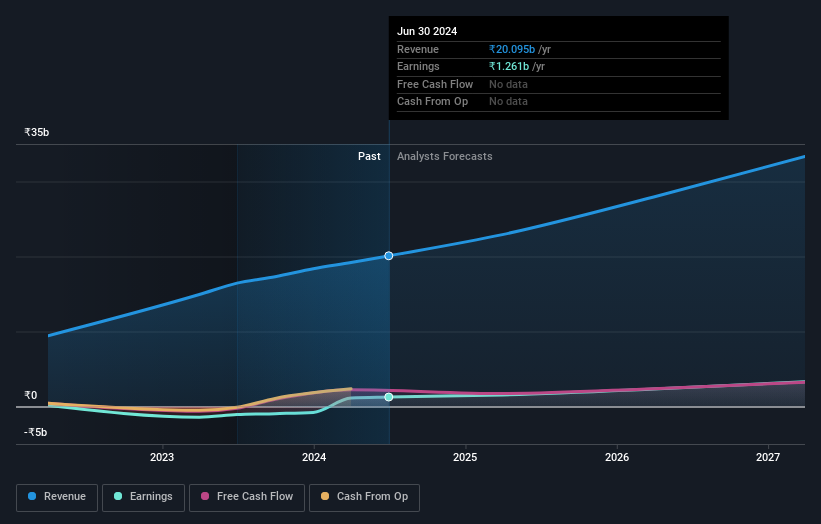

Quess (NSEI:QUESS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Quess Corp Limited is a business services provider operating in India, South East Asia, the Middle East, and North America, with a market capitalization of approximately ₹92.91 billion.

Operations: The company generates revenue through several segments: Workforce Management (₹134.42 billion), Operating Asset Management (₹28.01 billion), Global Technology Solutions excluding Product Led Business (₹23.40 billion), and Product Led Business (₹5.17 billion).

Insider Ownership: 15.9%

Revenue Growth Forecast: 13.4% p.a.

Quess Corp. Limited, demonstrating substantial growth potential, is forecasted to increase revenue by 13.4% annually, outperforming the broader Indian market's 9.7%. Despite a low projected Return on Equity of 18.2% in three years and unstable dividends, earnings are expected to surge by 27.6% annually. Recent strategic moves include appointing Mr. Gurmeet Chahal as CEO of Quess Global Technology Solutions, aiming to boost its capabilities in Data Technology and AI amid a corporate demerger process.

- Delve into the full analysis future growth report here for a deeper understanding of Quess.

- Our comprehensive valuation report raises the possibility that Quess is priced lower than what may be justified by its financials.

Varun Beverages (NSEI:VBL)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Varun Beverages Limited operates as a franchisee of PepsiCo, producing and distributing carbonated soft drinks and non-carbonated beverages, with a market capitalization of approximately ₹2.09 trillion.

Operations: The company generates its revenue primarily from the manufacturing and sale of beverages, amounting to ₹164.67 billion.

Insider Ownership: 36.4%

Revenue Growth Forecast: 16.5% p.a.

Varun Beverages, with high insider ownership, is poised for notable growth. Recent strategic expansions include launching a subsidiary in Zimbabwe and starting production at a new facility in Uttar Pradesh. Financially, the company reported a substantial increase in Q1 2024 earnings, with net income rising to INR 5.37 billion from INR 4.29 billion year-over-year. Despite its high debt levels, earnings are expected to grow by 24.36% annually, outpacing the Indian market's forecasted growth. Recent leadership changes aim to strengthen its strategic focus and operational efficiency.

- Take a closer look at Varun Beverages' potential here in our earnings growth report.

- Our valuation report here indicates Varun Beverages may be overvalued.

Where To Now?

- Investigate our full lineup of 83 Fast Growing Indian Companies With High Insider Ownership right here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Quess might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:QUESS

Quess

Operates as a business services provider in India, South East Asia, the Middle East, and North America.

Flawless balance sheet, undervalued and pays a dividend.