Advertisement

- India

- /

- Auto Components

- /

- NSEI:SJS

3 Growth Companies On Indian Exchange With High Insider Ownership And At Least 21% Earnings Growth

Simply Wall St

Reviewed by Simply Wall St

The Indian stock market has shown robust performance, with a 44% increase over the last 12 months and a steady rise of 1.0% in just the past week. In this context, companies with high insider ownership and strong earnings growth are particularly compelling, as they often signal confidence from those closest to the company's operations.

Top 10 Growth Companies With High Insider Ownership In India

| Name | Insider Ownership | Earnings Growth |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 28.9% |

| Pitti Engineering (BSE:513519) | 33.6% | 28.0% |

| Rajratan Global Wire (BSE:517522) | 19.8% | 33.5% |

| Dixon Technologies (India) (NSEI:DIXON) | 24.9% | 33.5% |

| Happiest Minds Technologies (NSEI:HAPPSTMNDS) | 37.8% | 22.7% |

| Jupiter Wagons (NSEI:JWL) | 11.1% | 27.2% |

| Paisalo Digital (BSE:532900) | 16.3% | 23.8% |

| JNK India (NSEI:JNKINDIA) | 23.8% | 31.8% |

| Chalet Hotels (NSEI:CHALET) | 13.1% | 27.6% |

| Apollo Hospitals Enterprise (NSEI:APOLLOHOSP) | 10.4% | 33.1% |

Let's explore several standout options from the results in the screener.

Kalpataru Projects International (NSEI:KPIL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Kalpataru Projects International Limited specializes in engineering, procurement, and construction (EPC) services for various sectors such as buildings, factories, power infrastructure, and transportation both in India and globally, with a market capitalization of approximately ₹186.61 billion.

Operations: The company's revenue is primarily generated from its Engineering, Procurement, and Construction (EPC) segment, which brought in ₹191.48 billion, and Development Projects contributing ₹2.80 billion.

Insider Ownership: 13.4%

Earnings Growth Forecast: 25.5% p.a.

Kalpataru Projects International Limited (KPIL) is poised for substantial growth with earnings expected to increase by 25.52% annually over the next three years, outpacing the broader Indian market's forecasted growth. This growth is supported by a robust revenue increase of 13.1% per year, also surpassing market averages. However, KPIL faces challenges as its interest payments are not well covered by earnings and its return on equity is projected to remain low at 19.6%. Additionally, despite a significant proposed final dividend of INR 8 per share for FY 2023-24, the company has an unstable dividend track record which might concern investors looking for consistent returns.

- Take a closer look at Kalpataru Projects International's potential here in our earnings growth report.

- Our comprehensive valuation report raises the possibility that Kalpataru Projects International is priced higher than what may be justified by its financials.

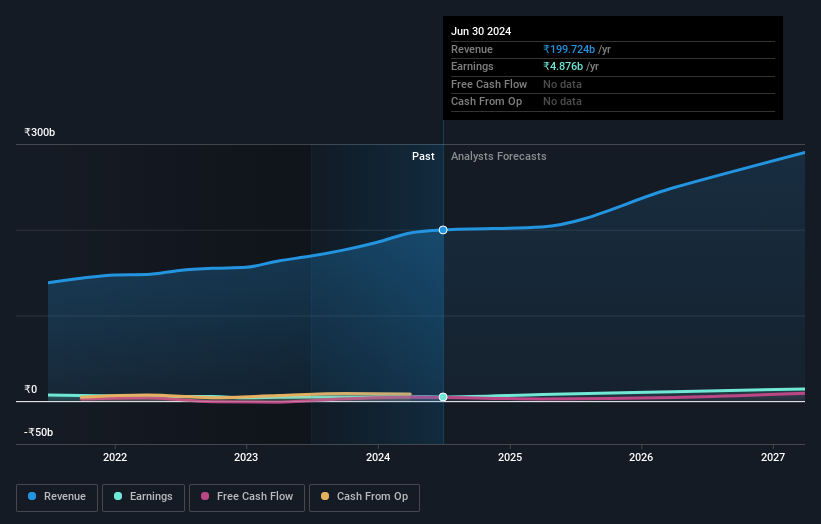

S.J.S. Enterprises (NSEI:SJS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: S.J.S. Enterprises Limited specializes in designing, developing, manufacturing, selling, and exporting decorative aesthetics for the automotive and consumer appliance industries, both domestically and internationally, with a market capitalization of ₹24.17 billion.

Operations: The company generates ₹6.28 billion from the manufacturing and selling of self-adhesive labels.

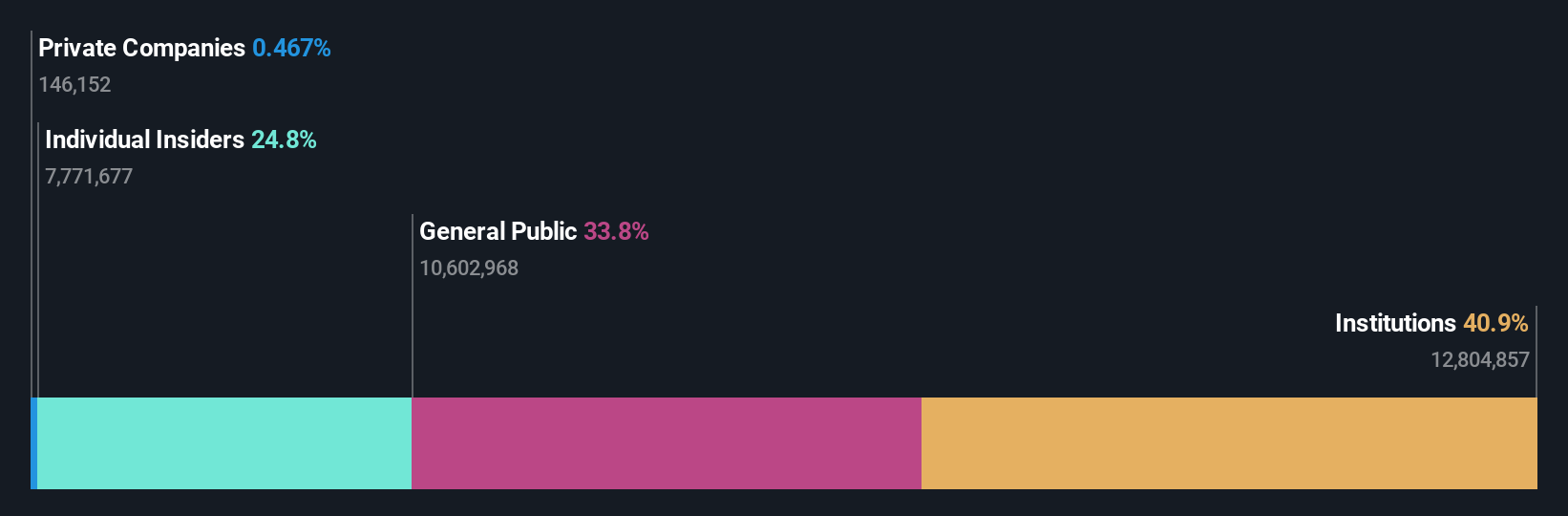

Insider Ownership: 24.8%

Earnings Growth Forecast: 21.7% p.a.

S.J.S. Enterprises exhibits promising growth with earnings forecasted to rise by 21.7% annually, outperforming the broader Indian market's expectation of 16% yearly growth. This is complemented by a revenue increase forecast at 17.3% annually, also above the Indian market average of 9.6%. Insider activities have been positive, with more shares bought than sold recently, indicating confidence from within. However, its projected return on equity remains modest at 18.5%, suggesting some challenges in efficiency or profitability might persist.

- Delve into the full analysis future growth report here for a deeper understanding of S.J.S. Enterprises.

- Our valuation report here indicates S.J.S. Enterprises may be overvalued.

Varun Beverages (NSEI:VBL)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Varun Beverages Limited operates as a franchisee of PepsiCo, producing and distributing carbonated soft drinks and non-carbonated beverages, with a market capitalization of approximately ₹2.11 billion.

Operations: The company generates revenue primarily through the manufacturing and sale of beverages, totaling ₹164.67 billion.

Insider Ownership: 36.4%

Earnings Growth Forecast: 24.7% p.a.

Varun Beverages, a growth-focused company with high insider ownership in India, is set to expand its operations, evidenced by the recent approval to establish a subsidiary in Zimbabwe. The firm's revenue and earnings have shown robust growth, with revenues increasing to INR 44.06 billion this quarter from INR 39.63 billion last year and net income rising to INR 5.37 billion from INR 4.29 billion. Expected annual earnings growth at 24.7% surpasses the Indian market forecast of 16%. Despite these positives, the company carries a high level of debt which could pose financial management challenges.

- Dive into the specifics of Varun Beverages here with our thorough growth forecast report.

- Upon reviewing our latest valuation report, Varun Beverages' share price might be too optimistic.

Where To Now?

- Delve into our full catalog of 82 Fast Growing Indian Companies With High Insider Ownership here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:SJS

S.J.S. Enterprises

Designs, develops, manufactures, sells, and exports decorative aesthetics primarily to automotive and consumer appliance industries in India and internationally.

Solid track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor