Advertisement

Investors Met With Slowing Returns on Capital At Swan Energy (NSE:SWANENERGY)

If you're looking for a multi-bagger, there's a few things to keep an eye out for. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. In light of that, when we looked at Swan Energy (NSE:SWANENERGY) and its ROCE trend, we weren't exactly thrilled.

Return On Capital Employed (ROCE): What Is It?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for Swan Energy:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

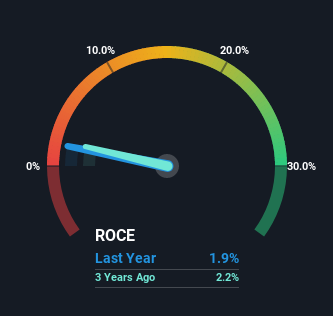

0.019 = ₹1.5b ÷ (₹102b - ₹23b) (Based on the trailing twelve months to March 2023).

Therefore, Swan Energy has an ROCE of 1.9%. In absolute terms, that's a low return and it also under-performs the Luxury industry average of 12%.

View our latest analysis for Swan Energy

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you want to delve into the historical earnings, revenue and cash flow of Swan Energy, check out these free graphs here.

SWOT Analysis for Swan Energy

Strength

- Debt is well covered by .

Weakness

- Interest payments on debt are not well covered.

- Dividend is low compared to the top 25% of dividend payers in the Luxury market.

- Current share price is above our estimate of fair value.

Opportunity

- SWANENERGY's financial characteristics indicate limited near-term opportunities for shareholders.

- Lack of analyst coverage makes it difficult to determine SWANENERGY's earnings prospects.

Threat

- Debt is not well covered by operating cash flow.

- Has less than 3 years of cash runway based on current free cash flow.

The Trend Of ROCE

The returns on capital haven't changed much for Swan Energy in recent years. Over the past five years, ROCE has remained relatively flat at around 1.9% and the business has deployed 511% more capital into its operations. Given the company has increased the amount of capital employed, it appears the investments that have been made simply don't provide a high return on capital.

On a side note, Swan Energy has done well to reduce current liabilities to 22% of total assets over the last five years. This can eliminate some of the risks inherent in the operations because the business has less outstanding obligations to their suppliers and or short-term creditors than they did previously.

The Bottom Line

In conclusion, Swan Energy has been investing more capital into the business, but returns on that capital haven't increased. Since the stock has gained an impressive 48% over the last five years, investors must think there's better things to come. Ultimately, if the underlying trends persist, we wouldn't hold our breath on it being a multi-bagger going forward.

Swan Energy does come with some risks though, we found 3 warning signs in our investment analysis, and 2 of those make us uncomfortable...

While Swan Energy may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SWANCORP

Swan

Manufactures and markets cotton, polyester cotton, linen and viscose fabrics, and non-lycra products in India and internationally.

Solid track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.8% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|22.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.8% overvalued

LI

Community Contributor