Advertisement

- India

- /

- Commercial Services

- /

- NSEI:IRCTC

Indian Railway Catering & Tourism (NSE:IRCTC) Is Paying Out A Larger Dividend Than Last Year

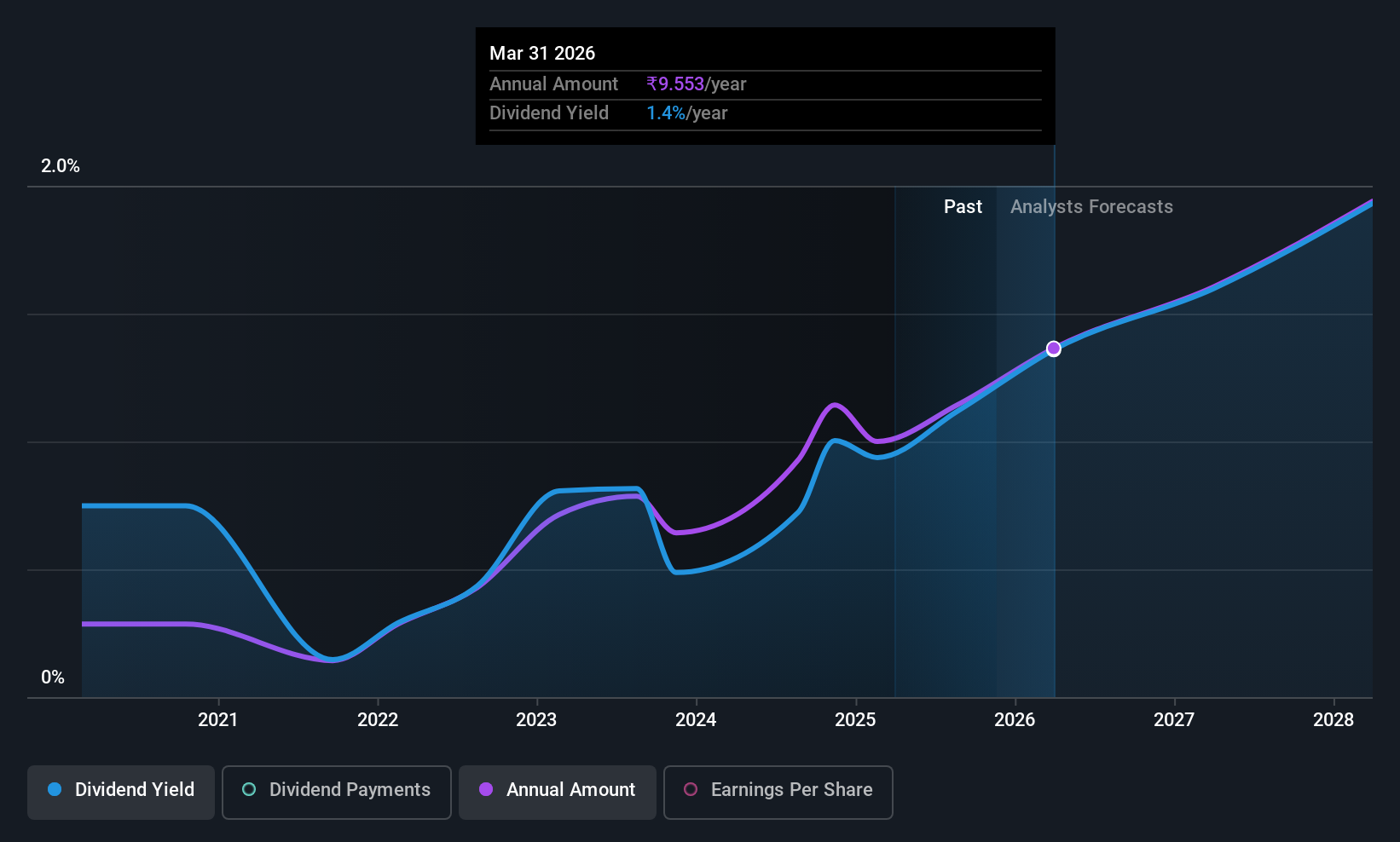

Indian Railway Catering & Tourism Corporation Limited's (NSE:IRCTC) periodic dividend will be increasing on the 12th of December to ₹5.00, with investors receiving 25% more than last year's ₹4.00. This will take the dividend yield to an attractive 1.1%, providing a nice boost to shareholder returns.

Indian Railway Catering & Tourism's Payment Could Potentially Have Solid Earnings Coverage

A big dividend yield for a few years doesn't mean much if it can't be sustained. Prior to this announcement, Indian Railway Catering & Tourism's dividend was comfortably covered by both cash flow and earnings. This means that a large portion of its earnings are being retained to grow the business.

Looking forward, earnings per share is forecast to rise by 19.4% over the next year. If the dividend continues along recent trends, we estimate the payout ratio will be 54%, which is in the range that makes us comfortable with the sustainability of the dividend.

Check out our latest analysis for Indian Railway Catering & Tourism

Indian Railway Catering & Tourism's Dividend Has Lacked Consistency

Indian Railway Catering & Tourism has been paying dividends for a while, but the track record isn't stellar. Due to this, we are a little bit cautious about the dividend consistency over a full economic cycle. Since 2019, the annual payment back then was ₹2.00, compared to the most recent full-year payment of ₹8.00. This means that it has been growing its distributions at 26% per annum over that time. Dividends have grown rapidly over this time, but with cuts in the past we are not certain that this stock will be a reliable source of income in the future.

The Dividend Looks Likely To Grow

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. It's encouraging to see that Indian Railway Catering & Tourism has been growing its earnings per share at 30% a year over the past five years. The company doesn't have any problems growing, despite returning a lot of capital to shareholders, which is a very nice combination for a dividend stock to have.

Indian Railway Catering & Tourism Looks Like A Great Dividend Stock

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. Earnings are easily covering distributions, and the company is generating plenty of cash. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. For example, we've picked out 1 warning sign for Indian Railway Catering & Tourism that investors should know about before committing capital to this stock. Is Indian Railway Catering & Tourism not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:IRCTC

Indian Railway Catering & Tourism

Engages in the provision of catering and hospitality, Internet ticketing, travel and tourism, and packaged drinking water services in India.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor