Advertisement

- India

- /

- Electrical

- /

- NSEI:TARIL

Market Participants Recognise Transformers and Rectifiers (India) Limited's (NSE:TRIL) Revenues Pushing Shares 26% Higher

Transformers and Rectifiers (India) Limited (NSE:TRIL) shares have continued their recent momentum with a 26% gain in the last month alone. The last 30 days were the cherry on top of the stock's 642% gain in the last year, which is nothing short of spectacular.

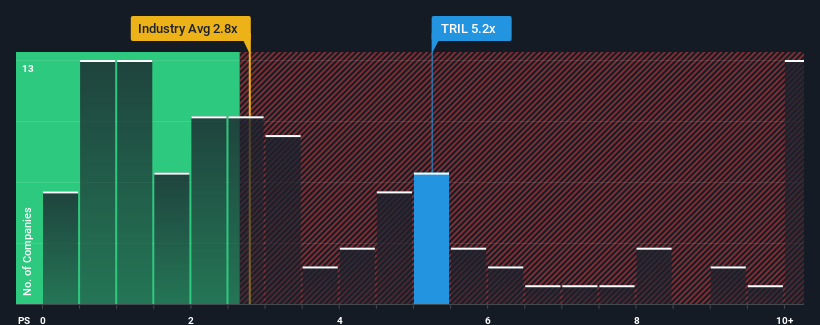

After such a large jump in price, when almost half of the companies in India's Electrical industry have price-to-sales ratios (or "P/S") below 2.8x, you may consider Transformers and Rectifiers (India) as a stock not worth researching with its 5.2x P/S ratio. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Transformers and Rectifiers (India)

What Does Transformers and Rectifiers (India)'s Recent Performance Look Like?

Transformers and Rectifiers (India) could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. One possibility is that the P/S ratio is high because investors think this poor revenue performance will turn the corner. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Transformers and Rectifiers (India).How Is Transformers and Rectifiers (India)'s Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as steep as Transformers and Rectifiers (India)'s is when the company's growth is on track to outshine the industry decidedly.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 6.2%. However, a few very strong years before that means that it was still able to grow revenue by an impressive 94% in total over the last three years. So we can start by confirming that the company has generally done a very good job of growing revenue over that time, even though it had some hiccups along the way.

Turning to the outlook, the next three years should generate growth of 38% each year as estimated by the only analyst watching the company. With the industry only predicted to deliver 17% per annum, the company is positioned for a stronger revenue result.

In light of this, it's understandable that Transformers and Rectifiers (India)'s P/S sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

Transformers and Rectifiers (India)'s P/S has grown nicely over the last month thanks to a handy boost in the share price. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our look into Transformers and Rectifiers (India) shows that its P/S ratio remains high on the merit of its strong future revenues. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

Plus, you should also learn about these 4 warning signs we've spotted with Transformers and Rectifiers (India) (including 1 which doesn't sit too well with us).

If you're unsure about the strength of Transformers and Rectifiers (India)'s business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Transformers and Rectifiers (India) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:TARIL

Transformers and Rectifiers (India)

Manufactures and sells transformers in India.

Exceptional growth potential with outstanding track record.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|21.8% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.6% undervalued

TR

Community Contributor