Advertisement

Are Dividend Investors Making A Mistake With Texmaco Rail & Engineering Limited (NSE:TEXRAIL)?

Could Texmaco Rail & Engineering Limited (NSE:TEXRAIL) be an attractive dividend share to own for the long haul? Investors are often drawn to a company for its dividend. Yet sometimes, investors buy a popular dividend stock because of its yield, and then lose money if the company's dividend doesn't live up to expectations.

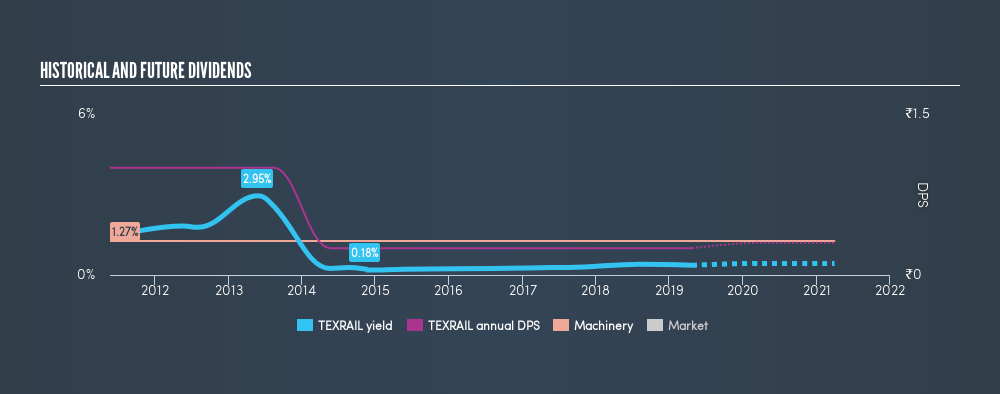

Investors might not know much about Texmaco Rail & Engineering's dividend prospects, even though it has been paying dividends for the last eight years and offers a 0.4% yield. A low yield is generally a turn-off, but if the prospects for earnings growth were strong, investors might be pleasantly surprised by the long-term results. When buying stocks for their dividends, you should always run through the checks below, to see if the dividend looks sustainable.

Explore this interactive chart for our latest analysis on Texmaco Rail & Engineering!

Payout ratios

Dividends are usually paid out of company earnings. If a company is paying more than it earns, then the dividend might become unsustainable - hardly an ideal situation. As a result, we should always investigate whether a company can afford its dividend, measured as a percentage of a company's net income after tax. In the last year, Texmaco Rail & Engineering paid out 77% of its profit as dividends. It's paying out most of its earnings, which limits the amount that can be reinvested in the business. This may indicate limited need for further capital within the business, or highlight a commitment to paying a dividend.

In addition to comparing dividends against profits, we should inspect whether the company generated enough cash to pay its dividend. Last year, Texmaco Rail & Engineering paid a dividend while reporting negative free cash flow. While there may be an explanation, we think this behaviour is generally not sustainable.

Is Texmaco Rail & Engineering's Balance Sheet Risky?

As Texmaco Rail & Engineering has a meaningful amount of debt, we need to check its balance sheet to see if the company might have debt risks.A quick way to check a company's financial situation uses these two ratios: net debt divided by EBITDA (earnings before interest, tax, depreciation and amortisation), and net interest cover. Net debt to EBITDA measures a company's total debt load relative to its earnings (lower = less debt), while net interest cover measures the company's ability to pay the interest on its debt (higher = greater ability to pay interest costs). Texmaco Rail & Engineering has net debt of 5.52 times its earnings before interest, tax, depreciation and amortisation (EBITDA) which implies meaningful risk if interest rates rise of earnings decline.

Net interest cover can be calculated by dividing earnings before interest and tax (EBIT) by the company's net interest expense. With EBIT of less than 1 times its interest expense, Texmaco Rail & Engineering's financial situation is potentially quite concerning. Readers should investigate whether it might be at risk of breaching the minimum requirements on its loans. Low interest cover and high debt can create problems right when the investor least needs them. We're generally reluctant to rely on the dividend of companies with these traits.

Remember, you can always get a snapshot of Texmaco Rail & Engineering's latest financial position, by checking our visualisation of its financial health.

Dividend Volatility

Before buying a stock for its income, we want to see if the dividends have been stable in the past, and if the company has a track record of maintaining its dividend. Looking at the last decade of data, we can see that Texmaco Rail & Engineering paid its first dividend at least eight years ago. It's good to see that Texmaco Rail & Engineering has been paying a dividend for a number of years. However, the dividend has been cut at least once in the past, and we're concerned that what has been cut once, could be cut again. During the past eight-year period, the first annual payment was ₹1.00 in 2011, compared to ₹0.25 last year. The dividend has fallen 75% over that period.

Dividend Growth Potential

With a relatively unstable dividend, and a poor history of shrinking dividends, it's even more important to see if EPS are growing. Texmaco Rail & Engineering's earnings per share have fallen -42% over the past year. This is a pretty serious concern, and it would be worth investigating whether something fundamental in the business has changed - or broken. While one year of growth is good, we'd be remiss not to point out that a majority of companies see their growth rates slow over a longer period.

Conclusion

When we look at a dividend stock, we need to form a judgement on whether the dividend will grow, if the company is able to maintain it in a wide range of economic circumstances, and if the dividend payout is sustainable. Texmaco Rail & Engineering gets a pass on its dividend payout ratio, but it paid out virtually all of its cash flow as dividends. This may just be a one-off, but we'd keep an eye on this. Earnings per share are down, and Texmaco Rail & Engineering's dividend has been cut at least once in the past, which is disappointing. Using these criteria, Texmaco Rail & Engineering looks quite suboptimal from a dividend investment perspective.

Without at least some growth in earnings per share over time, the dividend will eventually come under pressure either from costs or inflation. See if the 3 analysts are forecasting a turnaround in our free collection of analyst estimates here.

If you are a dividend investor, you might also want to look at our curated list of dividend stocks yielding above 3%.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NSEI:TEXRAIL

Texmaco Rail & Engineering

Manufactures, sells, and provides services for rail and rail related products in India and internationally.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|24.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|13.5% overvalued

DA

Community Contributor