Advertisement

- India

- /

- Construction

- /

- NSEI:RAMKY

There Are Some Reasons To Suggest That Ramky Infrastructure's (NSE:RAMKY) Earnings A Poor Reflection Of Profitability

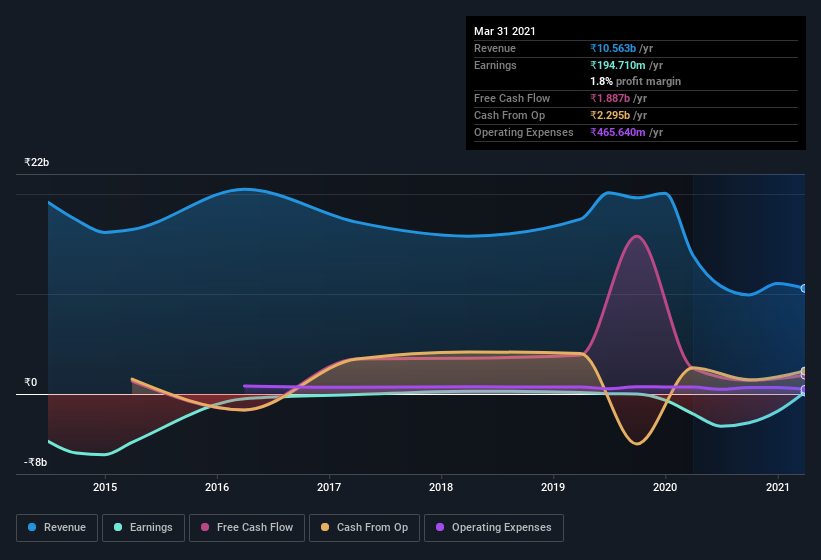

Investors appear disappointed with Ramky Infrastructure Limited's (NSE:RAMKY) recent earnings, despite the decent statutory profit number. Our analysis has found some underlying factors which may be cause for concern.

View our latest analysis for Ramky Infrastructure

The Impact Of Unusual Items On Profit

To properly understand Ramky Infrastructure's profit results, we need to consider the ₹236m gain attributed to unusual items. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. When we crunched the numbers on thousands of publicly listed companies, we found that a boost from unusual items in a given year is often not repeated the next year. And, after all, that's exactly what the accounting terminology implies. Ramky Infrastructure had a rather significant contribution from unusual items relative to its profit to March 2021. As a result, we can surmise that the unusual items are making its statutory profit significantly stronger than it would otherwise be.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Ramky Infrastructure.

An Unusual Tax Situation

Having already discussed the impact of the unusual items, we should also note that Ramky Infrastructure received a tax benefit of ₹891m. It's always a bit noteworthy when a company is paid by the tax man, rather than paying the tax man. Of course, prima facie it's great to receive a tax benefit. And since it previously lost money, it may well simply indicate the realisation of past tax losses. However, the devil in the detail is that these kind of benefits only impact in the year they are booked, and are often one-off in nature. Assuming the tax benefit is not repeated every year, we could see its profitability drop noticeably, all else being equal.

Our Take On Ramky Infrastructure's Profit Performance

In its last report Ramky Infrastructure received a tax benefit which might make its profit look better than it really is on a underlying level. And on top of that, it also saw an unusual item boost its profit, suggesting that next year might see a lower profit number, if these events are not repeated. Considering all this we'd argue Ramky Infrastructure's profits probably give an overly generous impression of its sustainable level of profitability. If you want to do dive deeper into Ramky Infrastructure, you'd also look into what risks it is currently facing. To help with this, we've discovered 3 warning signs (1 is concerning!) that you ought to be aware of before buying any shares in Ramky Infrastructure.

Our examination of Ramky Infrastructure has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you decide to trade Ramky Infrastructure, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:RAMKY

Ramky Infrastructure

Provides integrated construction, infrastructure development, and management services primarily in India.

Excellent balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|35.9% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|15.6% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|23.4% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|2.5% overvalued

TO

Community Contributor