- India

- /

- Construction

- /

- NSEI:NCC

It's Unlikely That NCC Limited's (NSE:NCC) CEO Will See A Huge Pay Rise This Year

Key Insights

- NCC to hold its Annual General Meeting on 29th of August

- CEO Alluri Ananta Venkata Raju's total compensation includes salary of ₹16.3m

- The total compensation is 41% higher than the average for the industry

- Over the past three years, NCC's EPS grew by 11% and over the past three years, the total shareholder return was 223%

CEO Alluri Ananta Venkata Raju has done a decent job of delivering relatively good performance at NCC Limited (NSE:NCC) recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 29th of August. However, some shareholders may still be hesitant of being overly generous with CEO compensation.

View our latest analysis for NCC

Comparing NCC Limited's CEO Compensation With The Industry

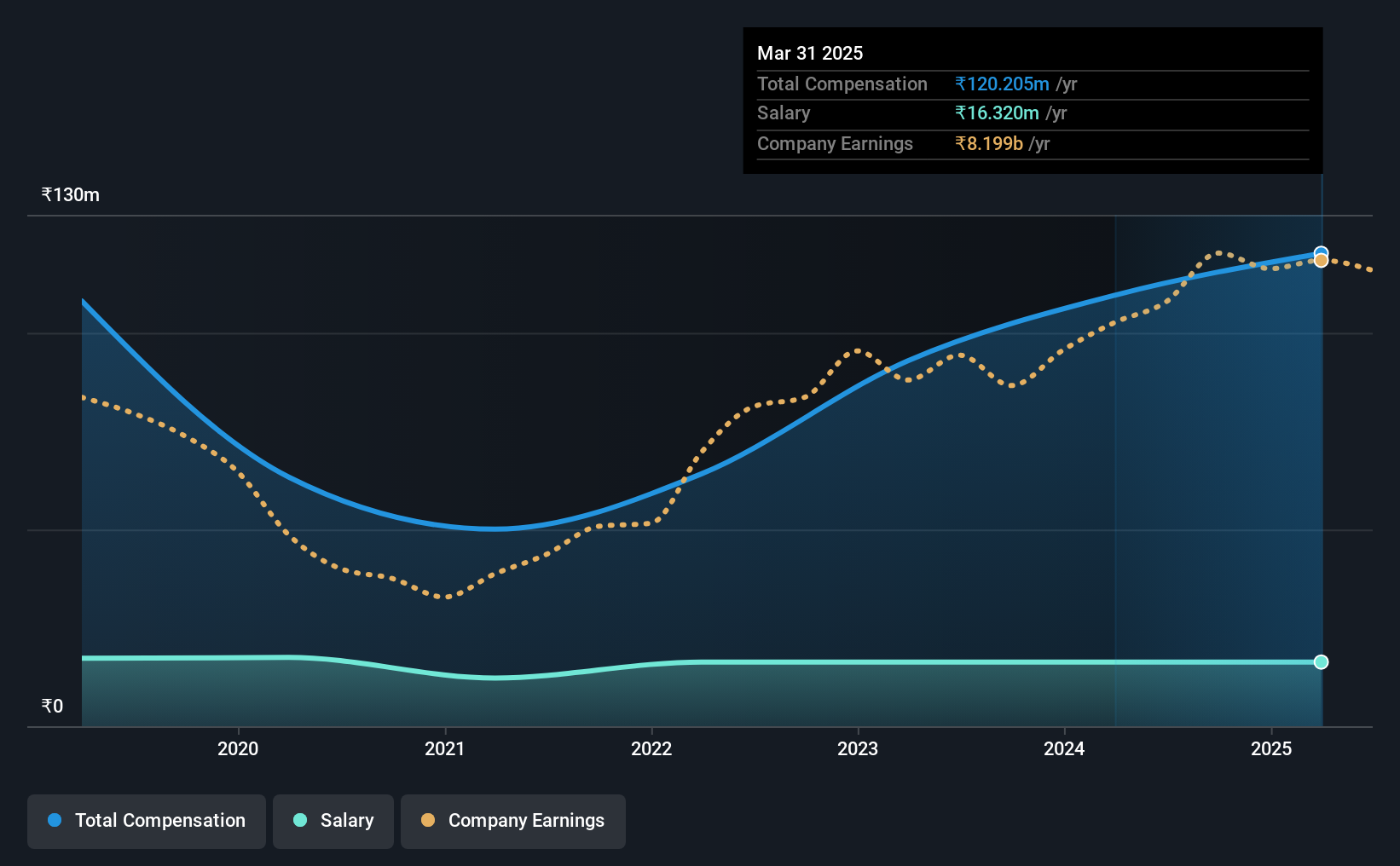

At the time of writing, our data shows that NCC Limited has a market capitalization of ₹136b, and reported total annual CEO compensation of ₹120m for the year to March 2025. Notably, that's an increase of 9.7% over the year before. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at ₹16m.

In comparison with other companies in the Indian Construction industry with market capitalizations ranging from ₹88b to ₹280b, the reported median CEO total compensation was ₹85m. This suggests that Alluri Ananta Venkata Raju is paid more than the median for the industry. What's more, Alluri Ananta Venkata Raju holds ₹430m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2025 | 2024 | Proportion (2025) |

| Salary | ₹16m | ₹16m | 14% |

| Other | ₹104m | ₹93m | 86% |

| Total Compensation | ₹120m | ₹110m | 100% |

Talking in terms of the industry, salary represents all of total compensation among the companies we analyzed, while other remuneration is, interestingly, completely ignored. NCC sets aside a smaller share of compensation for salary, in comparison to the overall industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

A Look at NCC Limited's Growth Numbers

NCC Limited has seen its earnings per share (EPS) increase by 11% a year over the past three years. Revenue was pretty flat on last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's always a tough situation when revenues are not growing, but ultimately profits are more important. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has NCC Limited Been A Good Investment?

Boasting a total shareholder return of 223% over three years, NCC Limited has done well by shareholders. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

To Conclude...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. However, if the board proposes to increase the compensation, some shareholders might have questions given that the CEO is already being paid higher than the industry.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We've identified 1 warning sign for NCC that investors should be aware of in a dynamic business environment.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if NCC might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:NCC

Undervalued with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Meta’s Bold Bet on AI Pays Off

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Visa Stock: The Toll Booth at the Center of Global Commerce

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion