Advertisement

Kajaria Ceramics (NSE:KAJARIACER) Has A Rock Solid Balance Sheet

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Kajaria Ceramics Limited (NSE:KAJARIACER) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Kajaria Ceramics

How Much Debt Does Kajaria Ceramics Carry?

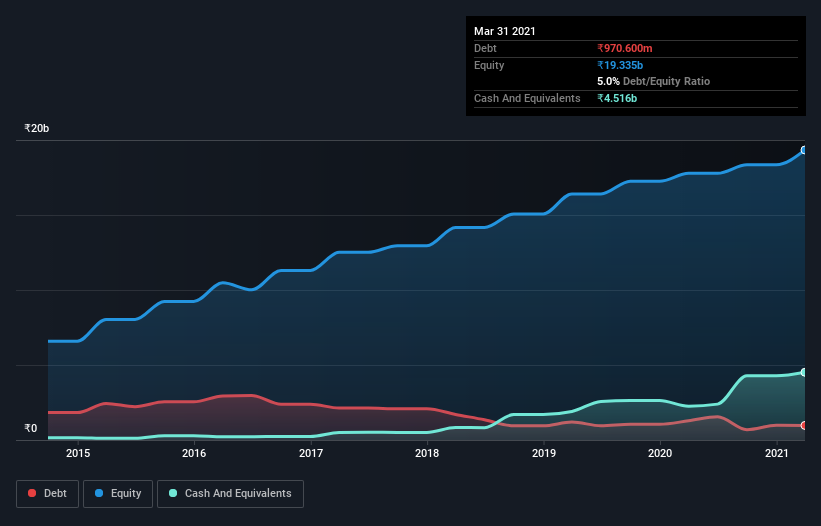

As you can see below, Kajaria Ceramics had ₹970.6m of debt at March 2021, down from ₹1.28b a year prior. But on the other hand it also has ₹4.52b in cash, leading to a ₹3.55b net cash position.

How Strong Is Kajaria Ceramics' Balance Sheet?

According to the last reported balance sheet, Kajaria Ceramics had liabilities of ₹4.60b due within 12 months, and liabilities of ₹1.34b due beyond 12 months. Offsetting this, it had ₹4.52b in cash and ₹4.45b in receivables that were due within 12 months. So it actually has ₹3.03b more liquid assets than total liabilities.

Having regard to Kajaria Ceramics' size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the ₹154.9b company is struggling for cash, we still think it's worth monitoring its balance sheet. Simply put, the fact that Kajaria Ceramics has more cash than debt is arguably a good indication that it can manage its debt safely.

On top of that, Kajaria Ceramics grew its EBIT by 30% over the last twelve months, and that growth will make it easier to handle its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Kajaria Ceramics's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Kajaria Ceramics may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the most recent three years, Kajaria Ceramics recorded free cash flow worth 64% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

While it is always sensible to investigate a company's debt, in this case Kajaria Ceramics has ₹3.55b in net cash and a decent-looking balance sheet. And we liked the look of last year's 30% year-on-year EBIT growth. So is Kajaria Ceramics's debt a risk? It doesn't seem so to us. We'd be very excited to see if Kajaria Ceramics insiders have been snapping up shares. If you are too, then click on this link right now to take a (free) peek at our list of reported insider transactions.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you decide to trade Kajaria Ceramics, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Kajaria Ceramics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:KAJARIACER

Kajaria Ceramics

Manufactures, sells, and distributes ceramic and vitrified wall and floor tiles under the Kajaria, GresBond, and Eternity brands in India and internationally.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|49.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|7.0% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|22.5% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|52.5% overvalued

RO

Community Contributor