Advertisement

- India

- /

- Aerospace & Defense

- /

- NSEI:HAL

Need To Know: The Consensus Just Cut Its Hindustan Aeronautics Limited (NSE:HAL) Estimates For 2026

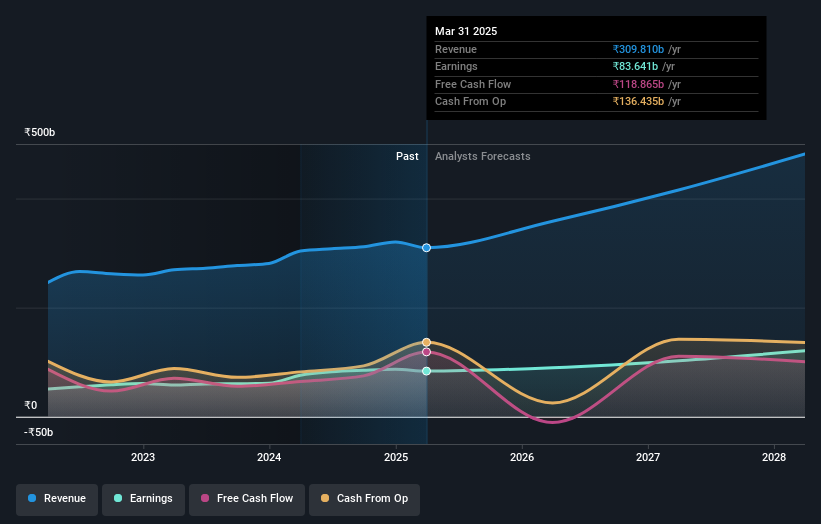

Market forces rained on the parade of Hindustan Aeronautics Limited (NSE:HAL) shareholders today, when the analysts downgraded their forecasts for this year. There was a fairly draconian cut to their revenue estimates, perhaps an implicit admission that previous forecasts were much too optimistic. Surprisingly the share price has been buoyant, rising 13% to ₹5,016 in the past 7 days. It will be interesting to see if the downgrade has an impact on buying demand for the company's shares.

Following the downgrade, the most recent consensus for Hindustan Aeronautics from its 13 analysts is for revenues of ₹355b in 2026 which, if met, would be a solid 15% increase on its sales over the past 12 months. Per-share earnings are expected to increase 3.8% to ₹130. Prior to this update, the analysts had been forecasting revenues of ₹406b and earnings per share (EPS) of ₹132 in 2026. Indeed we can see that the consensus opinion has undergone some fundamental changes following the recent consensus updates, with a measurable cut to revenues and some minor tweaks to earnings numbers.

Check out our latest analysis for Hindustan Aeronautics

The consensus price target rose 15% to ₹5,635, with the analysts apparently satisfied with the business performance despite lower revenue forecasts.

Of course, another way to look at these forecasts is to place them into context against the industry itself. The analysts are definitely expecting Hindustan Aeronautics' growth to accelerate, with the forecast 15% annualised growth to the end of 2026 ranking favourably alongside historical growth of 8.9% per annum over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 17% annually. Factoring in the forecast acceleration in revenue, it's pretty clear that Hindustan Aeronautics is expected to grow at about the same rate as the wider industry.

The Bottom Line

The most obvious conclusion from this consensus update is that there's been no major change in the business' prospects in recent times, with analysts holding earnings per share steady, in line with previous estimates. There was also a drop in their revenue estimates, although as we saw earlier, forecast growth is only expected to be about the same as the wider market. There was also a nice increase in the price target, with analysts apparently feeling that the intrinsic value of the business is improving. Often, one downgrade can set off a daisy-chain of cuts, especially if an industry is in decline. So we wouldn't be surprised if the market became a lot more cautious on Hindustan Aeronautics after today.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. We have estimates - from multiple Hindustan Aeronautics analysts - going out to 2028, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks with high insider ownership.

Valuation is complex, but we're here to simplify it.

Discover if Hindustan Aeronautics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:HAL

Hindustan Aeronautics

Engages in the design, development, manufacture, repair, overhaul, upgrade, and servicing of aircraft, helicopters, aero-engines, avionics, accessories, and aerospace structures in India and internationally.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|6.3% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.8% undervalued

GM

Community Contributor