Advertisement

- India

- /

- Construction

- /

- NSEI:BLKASHYAP

The Market Lifts B.L. Kashyap and Sons Limited (NSE:BLKASHYAP) Shares 29% But It Can Do More

The B.L. Kashyap and Sons Limited (NSE:BLKASHYAP) share price has done very well over the last month, posting an excellent gain of 29%. The annual gain comes to 189% following the latest surge, making investors sit up and take notice.

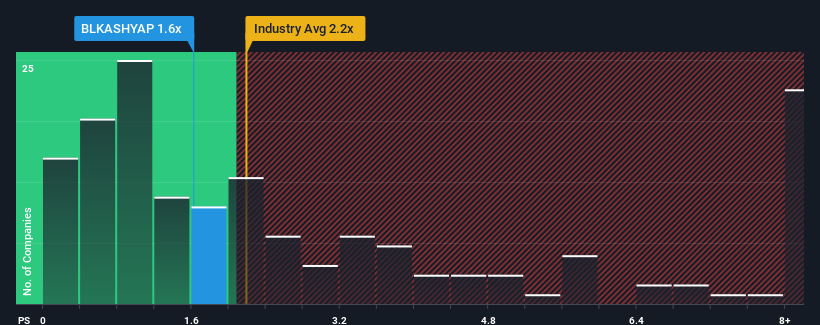

Even after such a large jump in price, B.L. Kashyap and Sons may still be sending buy signals at present with its price-to-sales (or "P/S") ratio of 1.6x, considering almost half of all companies in the Construction industry in India have P/S ratios greater than 2.2x and even P/S higher than 6x aren't out of the ordinary. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

See our latest analysis for B.L. Kashyap and Sons

How Has B.L. Kashyap and Sons Performed Recently?

We'd have to say that with no tangible growth over the last year, B.L. Kashyap and Sons' revenue has been unimpressive. Perhaps the market believes the recent lacklustre revenue performance is a sign of future underperformance relative to industry peers, hurting the P/S. If not, then existing shareholders may be feeling optimistic about the future direction of the share price.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on B.L. Kashyap and Sons' earnings, revenue and cash flow.Is There Any Revenue Growth Forecasted For B.L. Kashyap and Sons?

There's an inherent assumption that a company should underperform the industry for P/S ratios like B.L. Kashyap and Sons' to be considered reasonable.

Retrospectively, the last year delivered virtually the same number to the company's top line as the year before. Still, the latest three year period has seen an excellent 69% overall rise in revenue, in spite of its uninspiring short-term performance. Accordingly, shareholders will be pleased, but also have some questions to ponder about the last 12 months.

Comparing that recent medium-term revenue trajectory with the industry's one-year growth forecast of 12% shows it's noticeably more attractive.

With this information, we find it odd that B.L. Kashyap and Sons is trading at a P/S lower than the industry. Apparently some shareholders believe the recent performance has exceeded its limits and have been accepting significantly lower selling prices.

What We Can Learn From B.L. Kashyap and Sons' P/S?

Despite B.L. Kashyap and Sons' share price climbing recently, its P/S still lags most other companies. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of B.L. Kashyap and Sons revealed its three-year revenue trends aren't boosting its P/S anywhere near as much as we would have predicted, given they look better than current industry expectations. When we see strong revenue with faster-than-industry growth, we assume there are some significant underlying risks to the company's ability to make money which is applying downwards pressure on the P/S ratio. While recent revenue trends over the past medium-term suggest that the risk of a price decline is low, investors appear to perceive a likelihood of revenue fluctuations in the future.

Many other vital risk factors can be found on the company's balance sheet. Take a look at our free balance sheet analysis for B.L. Kashyap and Sons with six simple checks on some of these key factors.

If these risks are making you reconsider your opinion on B.L. Kashyap and Sons, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if B.L. Kashyap and Sons might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:BLKASHYAP

B.L. Kashyap and Sons

Engages in the construction and infrastructure development activities in India.

Adequate balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.8% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|22.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.8% overvalued

LI

Community Contributor