Advertisement

Azad Engineering Limited (NSE:AZAD) Looks Just Right With A 26% Price Jump

Azad Engineering Limited (NSE:AZAD) shares have had a really impressive month, gaining 26% after a shaky period beforehand. Looking further back, the 25% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

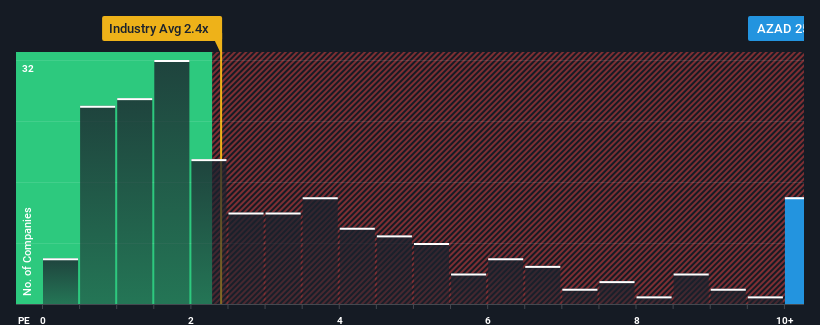

Since its price has surged higher, you could be forgiven for thinking Azad Engineering is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 25x, considering almost half the companies in India's Machinery industry have P/S ratios below 2.4x. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for Azad Engineering

How Azad Engineering Has Been Performing

With revenue growth that's superior to most other companies of late, Azad Engineering has been doing relatively well. The P/S is probably high because investors think this strong revenue performance will continue. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Azad Engineering.Is There Enough Revenue Growth Forecasted For Azad Engineering?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Azad Engineering's to be considered reasonable.

Taking a look back first, we see that the company grew revenue by an impressive 27% last year. The strong recent performance means it was also able to grow revenue by 118% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenue over that time.

Turning to the outlook, the next year should generate growth of 38% as estimated by the three analysts watching the company. With the industry only predicted to deliver 15%, the company is positioned for a stronger revenue result.

With this in mind, it's not hard to understand why Azad Engineering's P/S is high relative to its industry peers. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Key Takeaway

Shares in Azad Engineering have seen a strong upwards swing lately, which has really helped boost its P/S figure. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Azad Engineering's analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. Right now shareholders are comfortable with the P/S as they are quite confident future revenues aren't under threat. It's hard to see the share price falling strongly in the near future under these circumstances.

You always need to take note of risks, for example - Azad Engineering has 2 warning signs we think you should be aware of.

If these risks are making you reconsider your opinion on Azad Engineering, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:AZAD

Azad Engineering

Manufactures and sells precision- engineered components in India and internationally.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|8.7% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|7.2% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor