Advertisement

- India

- /

- Construction

- /

- NSEI:AHLUCONT

Investors Still Aren't Entirely Convinced By Ahluwalia Contracts (India) Limited's (NSE:AHLUCONT) Earnings Despite 25% Price Jump

Ahluwalia Contracts (India) Limited (NSE:AHLUCONT) shares have continued their recent momentum with a 25% gain in the last month alone. The last month tops off a massive increase of 112% in the last year.

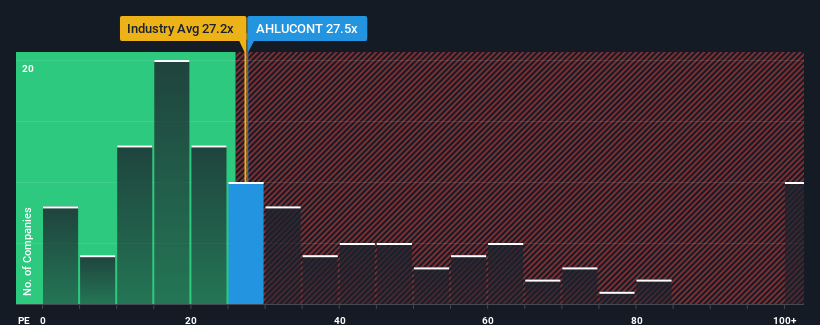

In spite of the firm bounce in price, Ahluwalia Contracts (India)'s price-to-earnings (or "P/E") ratio of 27.5x might still make it look like a buy right now compared to the market in India, where around half of the companies have P/E ratios above 32x and even P/E's above 59x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

Ahluwalia Contracts (India) certainly has been doing a good job lately as it's been growing earnings more than most other companies. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for Ahluwalia Contracts (India)

Is There Any Growth For Ahluwalia Contracts (India)?

Ahluwalia Contracts (India)'s P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

If we review the last year of earnings growth, the company posted a terrific increase of 51%. The strong recent performance means it was also able to grow EPS by 435% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Turning to the outlook, the next year should generate growth of 24% as estimated by the ten analysts watching the company. Meanwhile, the rest of the market is forecast to expand by 24%, which is not materially different.

With this information, we find it odd that Ahluwalia Contracts (India) is trading at a P/E lower than the market. It may be that most investors are not convinced the company can achieve future growth expectations.

The Key Takeaway

Ahluwalia Contracts (India)'s stock might have been given a solid boost, but its P/E certainly hasn't reached any great heights. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Ahluwalia Contracts (India) currently trades on a lower than expected P/E since its forecast growth is in line with the wider market. When we see an average earnings outlook with market-like growth, we assume potential risks are what might be placing pressure on the P/E ratio. It appears some are indeed anticipating earnings instability, because these conditions should normally provide more support to the share price.

A lot of potential risks can sit within a company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Ahluwalia Contracts (India) with six simple checks.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:AHLUCONT

Ahluwalia Contracts (India)

Operates as an engineering, procurement, and construction company in India.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|12.7% undervalued

MA

Community Contributor