Advertisement

- India

- /

- Auto Components

- /

- NSEI:WHEELS

We Think Some Shareholders May Hesitate To Increase Wheels India Limited's (NSE:WHEELS) CEO Compensation

Key Insights

- Wheels India's Annual General Meeting to take place on 17th of July

- Salary of ₹25.3m is part of CEO Srivats Ram's total remuneration

- Total compensation is 87% above industry average

- Wheels India's EPS grew by 224% over the past three years while total shareholder return over the past three years was 30%

Under the guidance of CEO Srivats Ram, Wheels India Limited (NSE:WHEELS) has performed reasonably well recently. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 17th of July. However, some shareholders will still be cautious of paying the CEO excessively.

See our latest analysis for Wheels India

How Does Total Compensation For Srivats Ram Compare With Other Companies In The Industry?

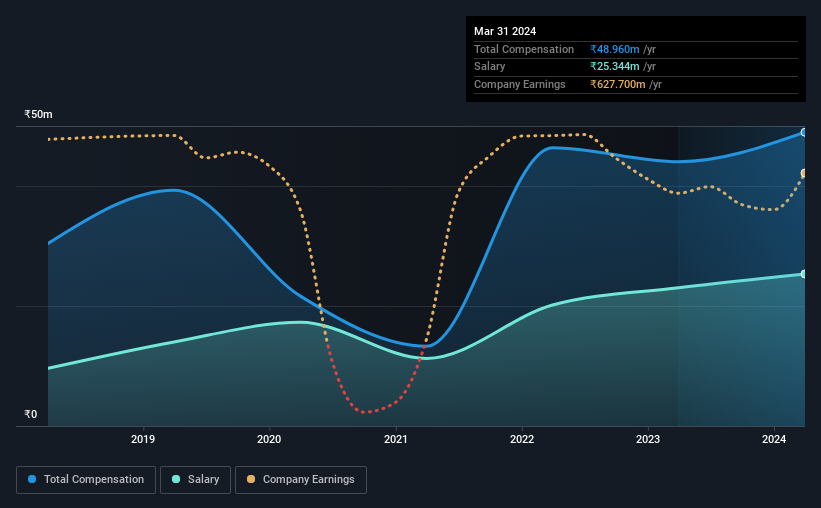

According to our data, Wheels India Limited has a market capitalization of ₹21b, and paid its CEO total annual compensation worth ₹49m over the year to March 2024. That's a notable increase of 11% on last year. In particular, the salary of ₹25.3m, makes up a fairly large portion of the total compensation being paid to the CEO.

On examining similar-sized companies in the Indian Auto Components industry with market capitalizations between ₹8.4b and ₹33b, we discovered that the median CEO total compensation of that group was ₹26m. Hence, we can conclude that Srivats Ram is remunerated higher than the industry median. Moreover, Srivats Ram also holds ₹46m worth of Wheels India stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | ₹25m | ₹23m | 52% |

| Other | ₹24m | ₹21m | 48% |

| Total Compensation | ₹49m | ₹44m | 100% |

Talking in terms of the industry, salary represented approximately 77% of total compensation out of all the companies we analyzed, while other remuneration made up 23% of the pie. It's interesting to note that Wheels India allocates a smaller portion of compensation to salary in comparison to the broader industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Wheels India Limited's Growth Numbers

Wheels India Limited's earnings per share (EPS) grew 224% per year over the last three years. In the last year, its revenue is up 7.3%.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's also good to see modest revenue growth, suggesting the underlying business is healthy. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Wheels India Limited Been A Good Investment?

Wheels India Limited has served shareholders reasonably well, with a total return of 30% over three years. But they would probably prefer not to see CEO compensation far in excess of the median.

To Conclude...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. Still, not all shareholders might be in favor of a pay raise to the CEO, seeing that they are already being paid higher than the industry.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. In our study, we found 3 warning signs for Wheels India you should be aware of, and 1 of them shouldn't be ignored.

Switching gears from Wheels India, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if Wheels India might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:WHEELS

Wheels India

Together with its subsidiary, engages in the manufacture and sale of automotive and industrial components in India and internationally.

Established dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor